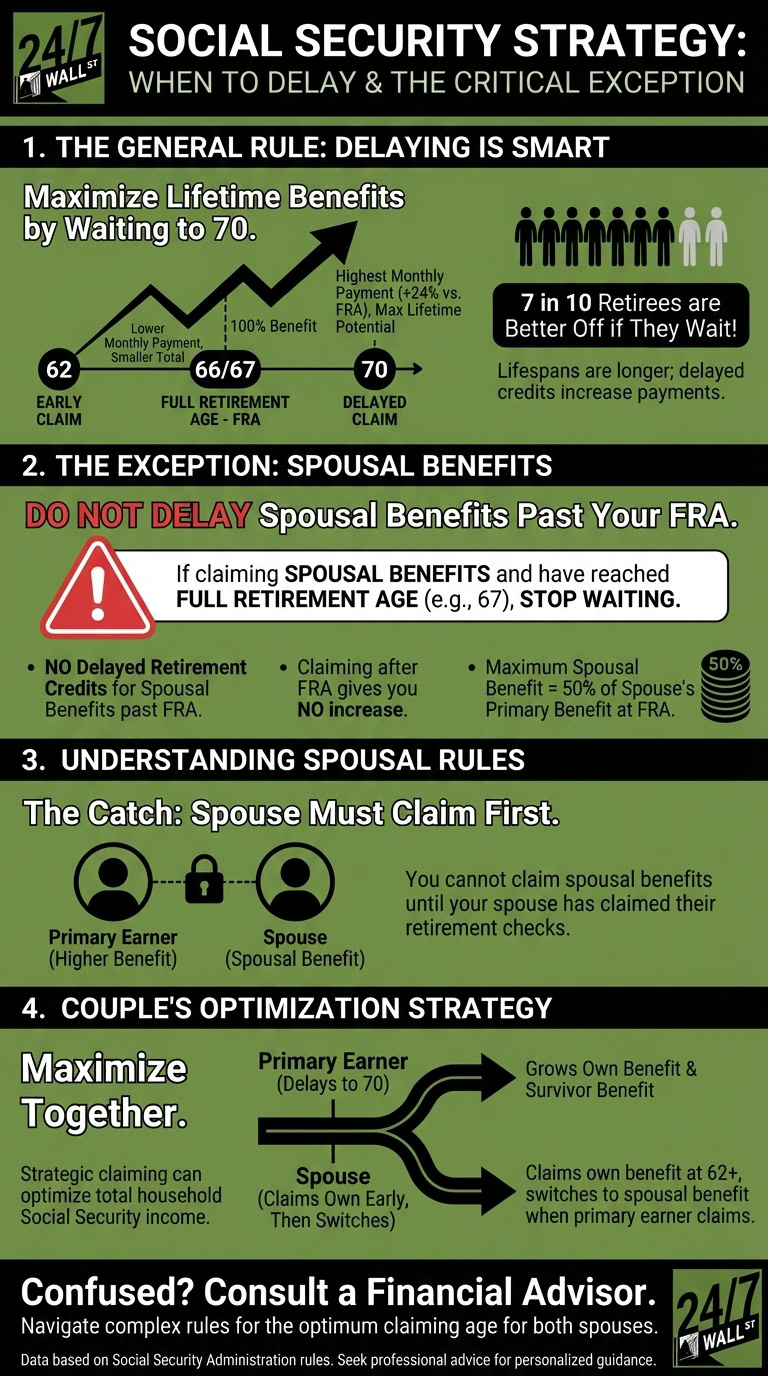

In most cases, delaying Social Security benefits is a smart choice for retirees. While benefits can be claimed starting at 62, putting off a claim as long as possible until 70 will result in the amount of your monthly payment increasing. Since the Social Security benefits formula was created to equalize out the amount early and late claimers received, and since lifespans have gotten longer since the formula was created, delaying until 70 also gives you the best chance of getting more lifetime benefits. In fact, 7 in 10 retirees are better off if they wait.

There is, however, one situation where retirees should definitely not put off their Social Security claim. Here’s what it is.

Do not delay your Social Security benefits claim if this applies to you

You should not wait to claim Social Security if you are planning to claim spousal benefits and you have reached your full retirement age.

Full retirement age is based on birth year and it’s 67 for anyone born in 1960 or later. If you wait until your full retirement age to claim spousal benefits you will receive 50% of your spouse’s primary benefit. If you claim before full retirement age, then you will receive a reduced amount. If you claim after, though, you do not see any increase in your monthly payments.

This is different from people who claim spousal benefits on their own work record. Those who get benefits based on their own earnings are also hit with early filing penalties for a claim before FRA, just as those who get spousal benefits are. However, people claiming their own retirement benefits also have the option to earn delayed retirement credits. Those credits increase payments by 2/3 of 1% per month until age 70. For someone with an FRA of 67, that adds up to a 24% benefits increase, which is a pretty substantial sum.

People getting spousal benefits can’t earn those delayed retirement credits, though. So delaying beyond their full retirement age doesn’t earn them any extra money. They’re giving up payments they could receive for no benefit at all.

Understand the rules for when you can claim spousal benefits

Now, there’s one big caveat to be aware of with spousal benefits. You can’t claim them until your spouse has claimed their retirement checks.

Say, for example, your husband was the higher earner and you want to claim spousal benefits on his work history. If your husband hasn’t yet filed for retirement benefits, you aren’t going to be allowed to claim your spousal benefits until he does.

It often makes sense for the spouse who earned more money to put off a Social Security claim for as long as they can. Doing so does increase their benefit and, as mentioned above, it gives them the best shot at earning the most lifetime income. They also max out survivor benefits when they wait, which is very important to protecting their partner if they die first. However, depending on whether there is an age gap, this can sometimes mean that a person in line for spousal benefits does have to wait.

If you and your husband are both 70 in our above example, for instance, it would make sense for you to claim your spousal benefits at your FRA if you could. But if your husband was waiting until 70 to get his retirement checks, you would not be able to.

The good news is, if you are eligible for your own retirement benefits — even if they aren’t worth much because you didn’t earn a lot — you could claim them at a younger age. You’d have some Social Security income coming into the house, and then when your spouse retirees, could claim spousal benefits then. This is the strategy many married couples use to optimize the lifetime Social Security income coming from both spouses and, in many cases, it’s a very good strategy worth considering.

Since Social Security is confusing for married couples because of all these different rules, working with a financial advisor could be your best bet. Your advisor can help you pick the optimum claiming age for both spouses so you can make the most of the Social Security benefits you’ve earned throughout your working life.