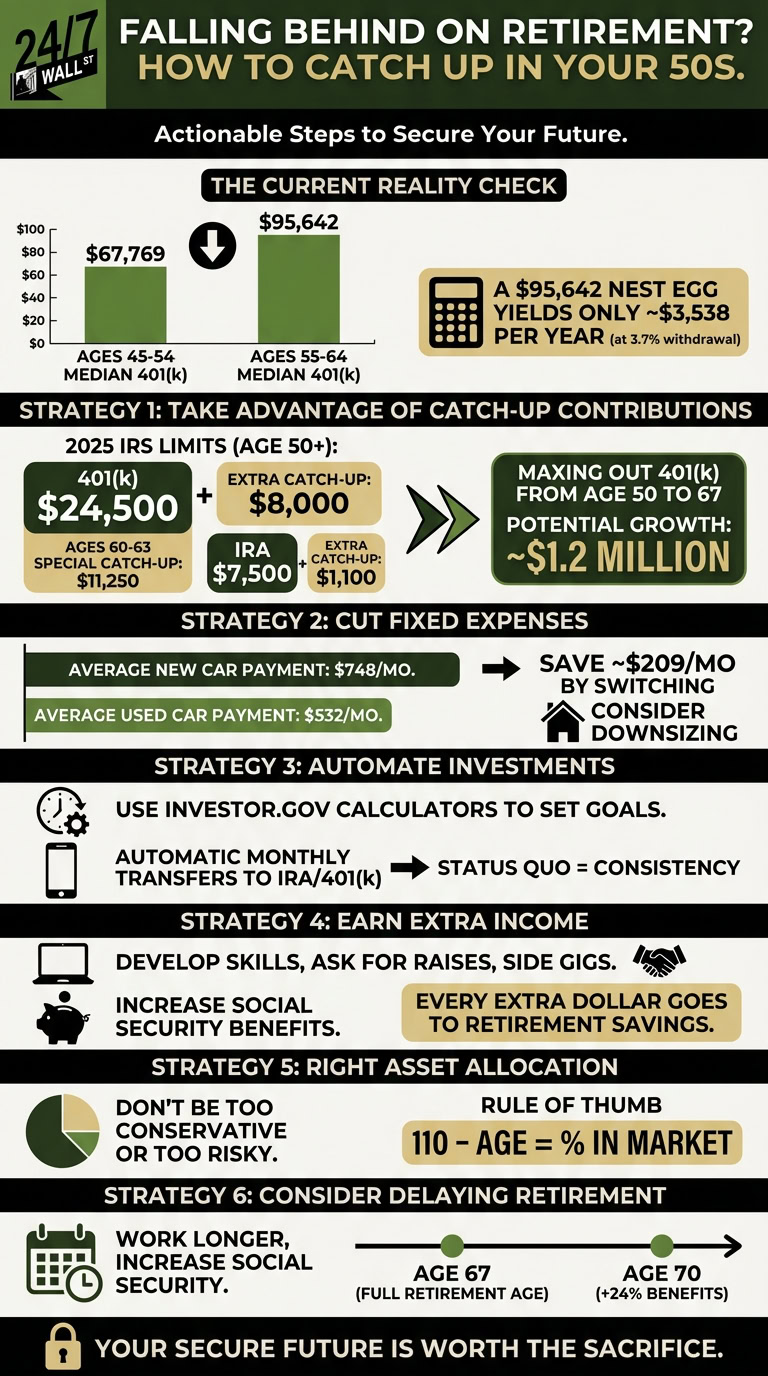

For Americans ages 45 to 54, the median 401(k) balance is just $67,769 according to Vanguard’s How America Saves Report. This is far less than most people need to be ready to retire. Things don’t get much better for those ages 55 to 64, either, with the median balance going up to just $95,642. A nest egg of only $95,642 would produce only $3,538 at a safe 3.7% withdrawal rate.

If you find yourself among the many people in their 50s who are falling short of where you need to be, there are techniques that can help you invest for your future. Here’s what you should do to get back on track.

Take advantage of catch-up contributions

One of the single best ways to get caught up is to take advantage of accounts that provide tax breaks for retirement. Accounts like a 401(k) and IRA allow you to reduce your taxable income based on the amount of contributions that you make during the year. For example, for each $1,000 you invest, you can save up to $220 on your taxes if you are in the 22% tax bracket (your savings will be more if you’re in a higher bracket or less if you’re in a lower one).

These accounts have annual contribution limits, but you are allowed to invest more in them once you reach age 50. In 2025, the IRS reports that the maximum 401(k) contribution is $24,500 while the maximum contribution for IRA accounts is $7,500. However, once you are 50 or over, you become eligible for extra catch-up contributions.

- You can make an additional $8,00 catch-up contribution to your 401(k) after age 50 or if you are 60, 61, 62, or 63, you can make an extra contribution of $11,250 instead of an extra $8,000.

- You can make an extra $1,100 catch-up contribution to your IRA after age 50

If you can max out these accounts, including catch-up contributions, you will get back on track very quickly to building a secure future. Investing $31,000 in a 401(k) from age 50 to age 67 would net you over $1.2 million — and since these contribution limits go up each year and you’d be eligible for the larger catch-up limits from ages 60 to 63, you’d end up even richer. Plus, if you are eligible for an employer match, this too would help your account grow.

Cut fixed expenses

Now, it may seem impossible to invest $32,500 or anything close to that amount. But you can work to increase your contributions and get as close as possible. One of the best ways to do that is to reduce fixed expenses. It is much harder to sustain many small cuts to discretionary spending over long periods than it is to just make one or two big lifestyle changes that can free up a lot of money to consistently invest.

Say, for example, that you can reduce your car payment. Experian reports that in the third quarter of 2025, the average car payment for a new car was $748 and the average car payment for a used car was $532. Opting for a cheaper used car instead of a new one would give you an extra $209 per month to invest. Better yet, buy a cheap used car, pay off the loan ASAP, and drive it until the wheels fall off so you have no car loan and an extra $532 to $748 per month to save for retirement.

You can also consider downsizing to a cheaper place to live or making other big one-time changes that will make a huge difference in how much you can invest.

Automate your investments

The best way to make sure you hit your goals is to see how much you need to save using the calculators at Investor.gov, which take into account your current savings balance, your projected returns, and your retirement timeline. Once you know your goals, try to work your budget to hit your monthly savings target — and then automate your investments.

Setting up automatic contributions to an IRA or 401(k) will ensure you don’t miss any months of investing for your future. You are much more likely to stick with your investing plan if it’s the status quo. If you have to force yourself to move money over to savings each month, on the other hand, then chances are good you’ll end up spending the money elsewhere and falling off course.

Earn some extra income

Increasing income can be one of the best ways to get on track for retirement savings when you have fallen behind. As a bonus, if you can earn more money, this will also result in your Social Security benefits being higher in the future since they are based on average wages during the 35 years when you earned the most.

You can increase your income by developing new job skills, asking for overtime, looking for a better-paying job, negotiating your raises, negotiating your salary when you start a new position, or working a side gig for a few hours per month. The more you can boost your income, the better.

As you increase what you earn, put every extra dollar towards your retirement investments. Since you aren’t counting on this money for bills or essential expenses, you should be able to use all of the money towards building a secure future.

Make sure you have the right asset allocation

When you are behind, you need your money to work hard for you. This means you need the right mix of investments. You don’t want to invest too conservatively and risk not earning the returns you need for compound growth to work its magic. At the same time, since you are getting closer to retirement age, you can’t take on too much risk.

Working with a financial advisor is a good idea to develop a personalized approach to asset allocation. However, there’s also a simple rule of thumb that says to subtract your age from 110 and put that percentage of your portfolio into the market. You can start there to get a good idea of whether your portfolio is invested in the right way.

Consider delaying retirement age

Finally, you may need to consider retiring at a later age. This would benefit you in many ways including allowing you to increase your Social Security benefit by delaying your claim; giving you more years to save; and leaving you with fewer years for your savings to support you.

Aiming to work until age least 67, which is the full retirement age for Social Security, can be a good idea but you may need to work a little longer depending on just how behind you are and how much you can devote to catching up. If you put off Social Security until 70 you can max out the benefits, increasing them by as much as 24% compared to your full retirement age.

By taking these steps, hopefully you can ensure you have the secure retirement you deserve even with your later start. It will require sacrifice but it will be worth it in the end.