In the world of Dave Ramsey and honest talk, you can always expect to hear some very difficult advice. This often means that Dave, who is well-known for being outspoken on other people’s financial situations, will give you the advice you need to hear, even if it’s not the easiest advice to receive.

On the other hand, sometimes Dave gives some really great advice on what people need to hear that they might not have thought of themselves. One such case is that Dave correctly says that to retire, you need to hit a certain financial number, and not just focus on the age at which you retire.

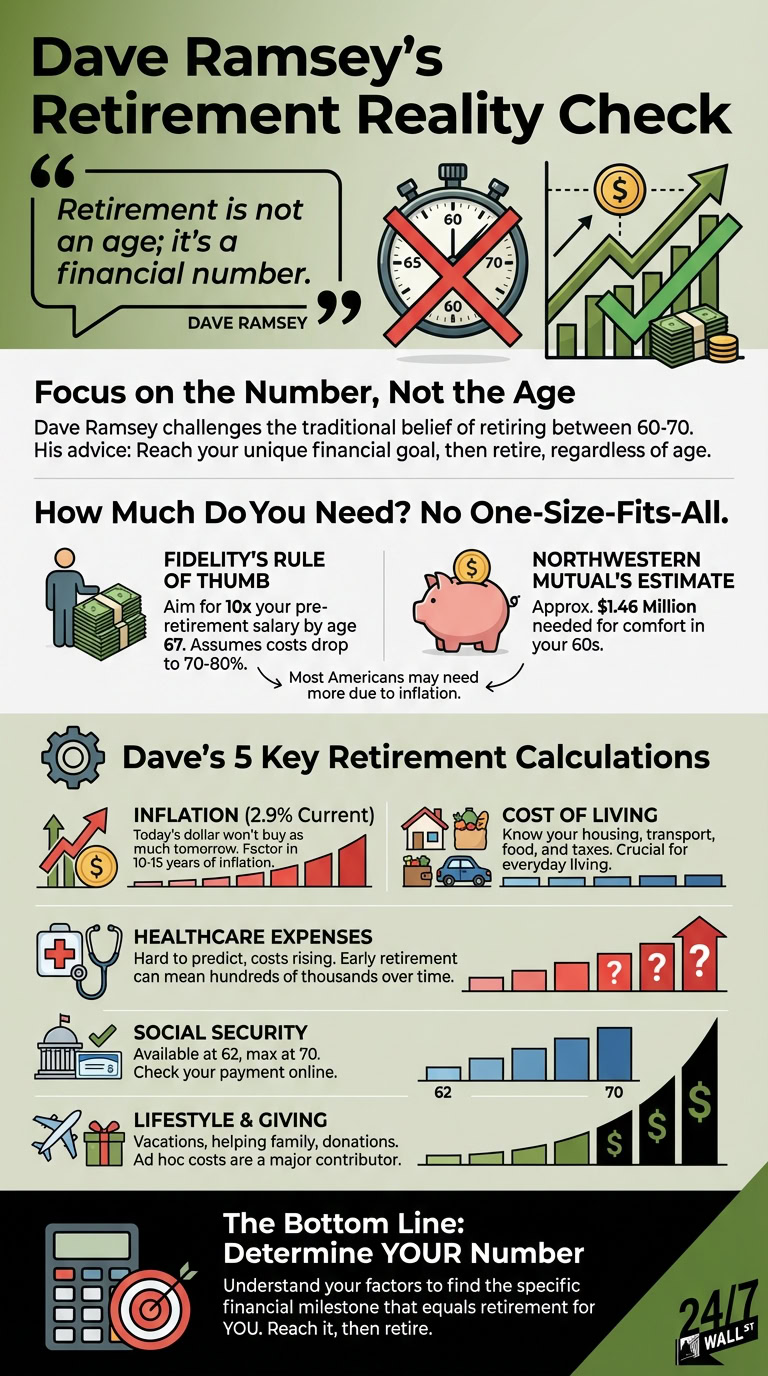

What Dave Means

When Dave wrote, “Retirement is not an age; it’s a financial number,” this unsurprisingly caught many people off guard. For far too many years, there has been a belief in the US that you retire sometime between 60 and 70 and no sooner.

While those in the FIRE (financial independence, retire early) world would love to disagree, many people are now starting to gravitate toward Dave’s advice as gospel. There are factors that can affect whatever number you think you need, but Dave’s bottom line is that you should absolutely be focused on the number, and whenever you hit that number, that’s when you retire.

How Much Do You Need?

The challenging part of this entire conversation is that there is no one-size-fits-all number for everyone. It doesn’t matter if you are middle-class, upper-middle-class, or rich as everyone’s nest egg size is going to look different from their neighbors’.

In many instances, the prevailing theory is that you need a certain multiple of your pre-retirement income. According to Fidelity, you want to have at least 10 times your salary put away by the time you are 67, with the understanding that your costs will drop to between 70-80% of pre-retirement spending.

On the other hand, Northwestern Mutual indicates that it believes you need around $1.46 million to comfortably retire beginning in your 60s. Inflation concerns are still abundant, so it’s very likely most Americans would want a little more than this to be truly comfortable, but you could consider this number to be fairly close to where you want to be.

The bottom line is that there are any number of ways to determine how much you’ll need. Still, the 10x number of your pre-retirement income seems to be a pretty good theory if you’re retiring around Full Retirement Age of 67 and then withdrawing Social Security for a little extra income boost.

Dave’s Calculations

Dave Ramsey believes you should factor in a few things as part of your retirement plan to reach your number. First is inflation, which at a current 2.7% means that what $1 million means today will not buy as much in the next 10 or 15 years.

The second is your cost of living, arguably the most crucial money determination. Knowing this number will help you determine a good approximation of what you need for housing, transportation, food, taxes, and everyday living.

The same goes for healthcare, though it’s pretty hard to predict exactly how much you will need in this case. The average cost of healthcare is only going in one direction, and if you retire early, say in your 40s, you can expect hundreds of thousands in healthcare expenses over time.

Social Security will also play a role, and the good news is that you can see your payment at any time through the Social Security Administration. You can start withdrawing money at 62, but the maximum payment starts at 70.

Finally, your lifestyle will be the other major contributor to knowing what kind of number you need. Whereas your cost-of-living is more fixed, lifestyle costs are more ad hoc, as in you might decide to spontaneously take a vacation or help out with college for children or grandchildren. Do you want to make charitable donations? According to Dave, knowing what kind of number you can expect for your lifestyle here will go a long way toward understanding your actual retirement number.