Hitting the $500,000 portfolio milestone is a big deal that deserves a nice pat on the back. That said, if you’re gearing up for an earlier retirement (let’s say in your 50s), things could get a bit more challenging if you’re not expecting social security benefits to be coming your way any time soon. In any case, there are a number of ways that can help make your half-a-million-dollar portfolio live up to your expectations. Ultimately, it depends on the type of retirement lifestyle you seek and which state or province you reside in.

Undoubtedly, a $500,000 portfolio could play a huge role in funding a partial retirement in places where housing costs are below the average. That said, if you’re in a pricy city like New York, you may need to stick it out in the workforce longer, as it’s going to be incredibly difficult to stretch a $500,000 portfolio without causing you to chase yield. As always, consult a financial adviser because everybody’s push to the retirement finish line will differ vastly.

In any case, here are five quick tips that you may wish to bring up with your adviser at your next meeting!

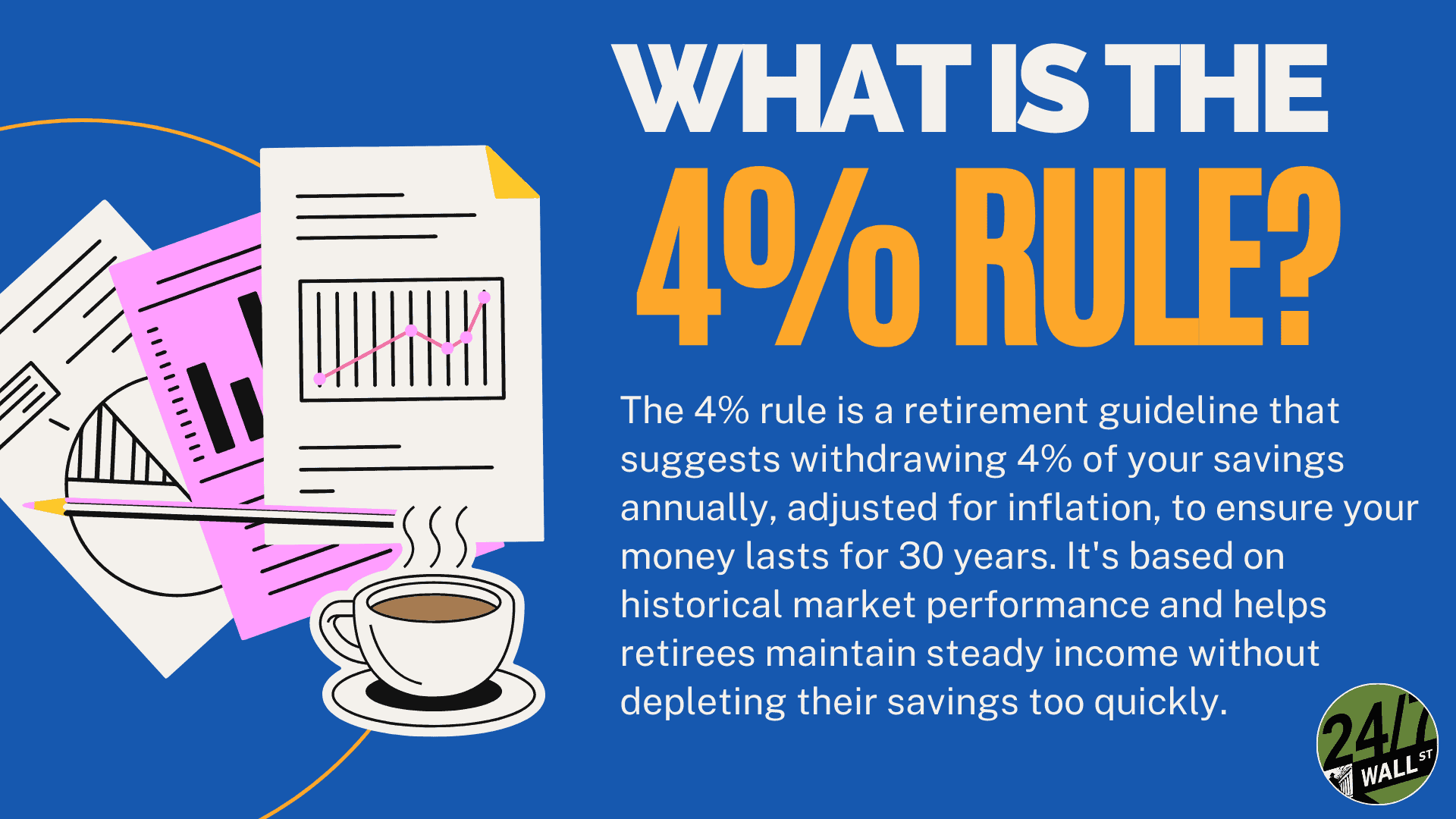

Consider Leveraging the 4% Rule.

No surprises here. The 4% rule is well-known for a reason. And though you can easily average a portfolio yield well north of 5% without taking on significantly more risk in this high-rate environment, it’s not only more conservative to go back to the timeless 4% rule, but you may get more growth and appreciation from a 4%-yielding dividend stock in this environment.

Indeed, capital gains still matter, even as you shift gears toward passive income to be ready for retirement. But if you’ve got the flexibility to time your retirement date, perhaps it makes sense to find the optimal balance of income and growth. It’s all right not to know exactly when you’ll retire, but the good news is you have options as your portfolio hits the $500,000 mark.

Yields North of 5% May Make Sense. But Don’t Chase Yield.

The 4% rule suggests $20,000 in annual passive income from a $500,000 portfolio. This is hardly enough to fund a comfy retirement, but it’s still a nice supplement if you’re looking to enter a semi-retirement of sorts before a full-blown one. At these levels, a 5%-yielder like Crown Castle (NYSE:CCI | CCI Price Prediction) makes a lot of sense to pick up, especially while it’s still hurting from higher rates. As rates come down, CCI stock can continue its run, offering a perfect mix of dividends (5.20% at writing) and steady multi-year appreciation.

There are a slew of high-yielders out there, but it’s important to analyze each firm’s balance sheet to ensure its payout isn’t stretching things too far. The last thing you want is to experience a dividend cut amid retirement.

Ensure You’re Properly Diversified

Every once in a while, it pays to check in with your portfolio to ensure it’s still diversified across industries and geographies.

Undoubtedly, if you’ve held onto shares of Nvidia (NASDAQ:NVDA) these past handful of years, it may have grown to comprise too large a portion of your portfolio. With the higher valuation, volatility levels, and downside risks, perhaps it makes sense to trim the big winner in favor of some cheaper, higher-yielding dividend stocks that can gain from lower rates.

Don’t Forget About Fixed Income

Best-in-breed dividend stocks may offer greater potential for gains, especially if you buy them at a hefty discount. However, that doesn’t mean you should neglect fixed-income securities, which hold a place in any diversified portfolio.

Whether we’re talking CDs, bonds, bond funds, or annuities, fixed-income products can make sense, especially since nasty market crashes can completely derail retirement plans. I’d check in with your adviser on this one as asset allocation is highly personal to each individual.

Don’t Forget About Growth

Finally, don’t neglect the growth prospects of a dividend stock. Far too many retirees concentrate on yield, with little to no emphasis on growth. As inflation hits every year, you’re going to want a dividend payer that can consistently raise its payout. To do so, a firm needs to grow its cash flows. And if you’re looking at a high-yielder that’s actually experiencing falling revenue growth, the firm’s dividend growth prospects should come into question.

For instance, Crown Castle shares have a robust record of growing dividends. In the past five years, the cell tower REIT has averaged more than 8% in annual dividend growth. Though the payout ratio has climbed, fading headwinds and hopes for lower rates paint a prettier picture of the firm’s dividend health and growth potential.