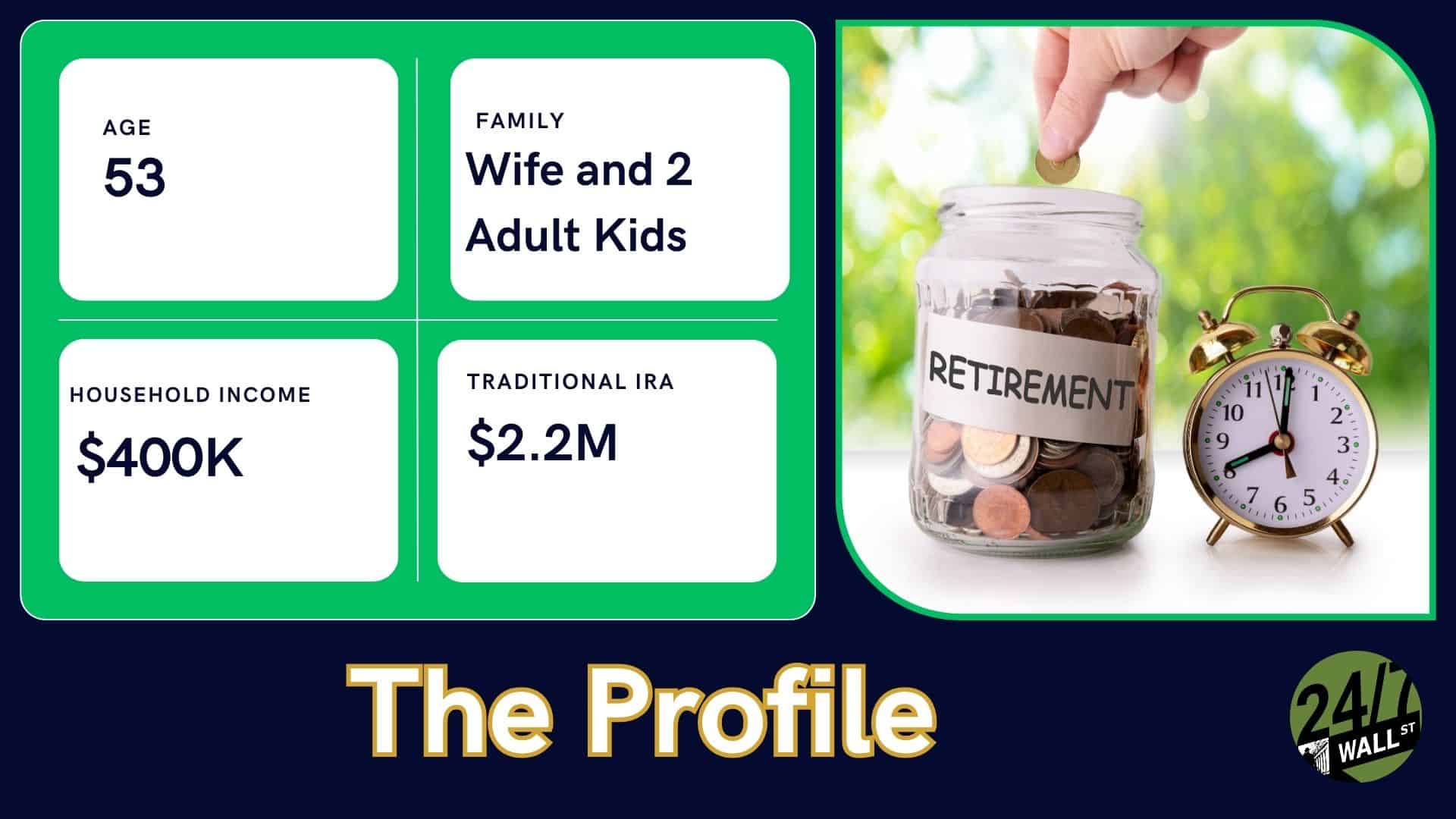

At 54 with $1.8 million saved, you are in a strong position. The gap between “strong” and “finished” is exactly what makes this disagreement worth taking seriously.

Your wife wants to open a 529 for a grandchild. You want to keep every dollar pointed at retirement. You are both right about something, and you are both missing something.

Why $1.8 Million at 54 Is a Starting Point, Not a Finish Line

The 4% rule applied to $1.8 million produces roughly $72,000 per year in inflation-adjusted income. Whether that is enough depends entirely on what you spend.

If your annual expenses run $90,000 or more, $1.8 million is not a comfortable finish line at 54. Add Social Security (full retirement age is 67 for anyone born in 1960 or later), and the picture improves, but that benefit is 13 years away. Healthcare is the wildcard. National healthcare spending has climbed steadily, rising from $3,432.2 billion in January 2025 to $3,718.3 billion by February 2026, and pre-Medicare retirees absorb those costs directly. A couple retiring at 62 faces five years of private insurance before Medicare eligibility at 65.

The next decade of contributions matters enormously. At 54, both spouses can make catch-up contributions to their 401(k)s. The 2026 limit is $24,500, plus an $8,000 catch-up for those 50 and older, for a total of $32,500 per person per year. Two spouses maxing out 401(k)s could add $65,000 annually to the portfolio before any employer match. That compounding window is irreplaceable.

Core PCE inflation has risen steadily, with the index climbing from 125.502 in April 2025 to 128.859 by February 2026. A 30-year retirement means purchasing power erosion is not theoretical. A portfolio that feels comfortable today will need to cover costs that look meaningfully different in 2046.

How a Modest 529 Can Work Without Derailing Retirement

The husband’s instinct to protect retirement is correct as a priority. The two goals can coexist with the right sequencing.

A 529 plan funded modestly by grandparents carries real advantages. The 2026 annual gift tax exclusion is $19,000 per recipient per donor. A married couple can jointly contribute $38,000 per year to a grandchild’s 529 without triggering gift tax reporting. There is also a superfunding option: a one-time lump sum of up to $95,000 per grandparent (five years of exclusions front-loaded at once) that removes assets from the taxable estate while letting the money grow tax-free for qualified education expenses.

Grandparent-owned 529 plans also no longer hurt financial aid under updated FAFSA rules. A one-time contribution of $20,000 to $30,000 into a 529 today, invested in an age-based equity allocation, has 14 to 18 years to compound before a grandchild reaches college age. Private nonprofit four-year college tuition reached $45,000 in the 2025-26 academic year, a 4% year-over-year increase. Starting early matters.

Max Out Retirement Accounts Before Opening a 529

Before any dollar goes to a grandchild’s education, answer this question: are both spouses maxing out their 401(k) catch-up contributions and fully funding Roth IRAs or backdoor Roth conversions? The 2026 IRA limit for those 50 and older is $8,600. If the answer is no, the husband is right and the wife’s instinct should wait.

If the answer is yes, consider three paths:

- Modest ongoing 529 contributions: Contribute $5,000 to $10,000 per year from after-tax income. This preserves retirement momentum while honoring the wife’s goal.

- One-time superfunding contribution: Make a single lump-sum contribution now using the five-year gift tax election, then stop. This front-loads the grandchild’s educational benefit without creating an ongoing obligation that competes with retirement savings in future years.

- Wait and revisit at 60: Defer the 529 decision entirely until closer to retirement and can assess actual spending needs, Social Security projections, and portfolio performance with more precision. This is the most conservative path.

Retirement First, Then Generosity

Max out every tax-advantaged retirement account first, every year, without exception. If cash flow allows after that, open the 529 with a modest contribution. Do not let generosity toward a grandchild become a liability for your own retirement. You cannot borrow for retirement the way a grandchild can borrow for college.

The Fed funds rate is near 4% and the 10-year Treasury yields around 4.3%, meaning conservative savings vehicles are producing real returns. Money parked in a 529 is not dead money.

If you are not yet maxing out retirement contributions, that gap deserves immediate attention before any 529 discussion happens. The final working decade is when compounding does its heaviest lifting.