Nvidia (NASDAQ:NVDA | NVDA Price Prediction) has been the obvious winner over the past three years if we look at the sheer amount of money pouring into it. But if you involve percentages, Palantir (NASDAQ:PLTR) wins. Both companies have spearheaded the AI rally, and you likely have exposure to both in some way.

Which is better for the long run? NVDA and PLTR are at nosebleed valuations and have rallied by quadruple digits over the past three years. Investors are at a crossroads and are balking at the premium they must pay. The companies undeniably have stellar fundamentals, but it’s the tech industry after all. The last time something pivotal like AI dominated Wall Street was during the internet boom in the early 2000s. If you looked at some of the biggest names on exchanges back then, you wouldn’t recognize half of them.

However, Nvidia could become the Apple of AI, providing hardware and maintaining its dominance. In contrast, Palantir may dominate AI software just as Google managed to maintain its search engine dominance for decades. Let’s take a look at the likelihood of each of those scenarios and find out whether or not PLTR stock or NVDA stock is better today.

Nvidia (NVDA)

Starting with the biggest of the two, Nvidia looks expensive on paper, but is quite cheap compared to Palantir. You’re paying less than 40 times forward earnings for FY 2026 when you buy NVDA stock and 28 times forward FY 2027 earnings.

Nvidia is mostly an AI hardware company and has become the backbone of AI training farms and data centers. Its AI chips are the best in class, and competitors are still behind. Some have managed to narrow the gap, and companies like Broadcom (NASDAQ:AVGO) are managing to land some customers by making custom AI chips for them. However, Nvidia’s overall dominance remains undisputed.

Companies are continuously pouring money into AI and building out more data center capacity. There has been no indication that this rapid build-out will stop anytime soon, and Nvidia will arguably be the biggest beneficiary as it can provide the best hardware.

And as long as it can do that, it will remain in the lead. AI companies are willing to pay more for better performance.

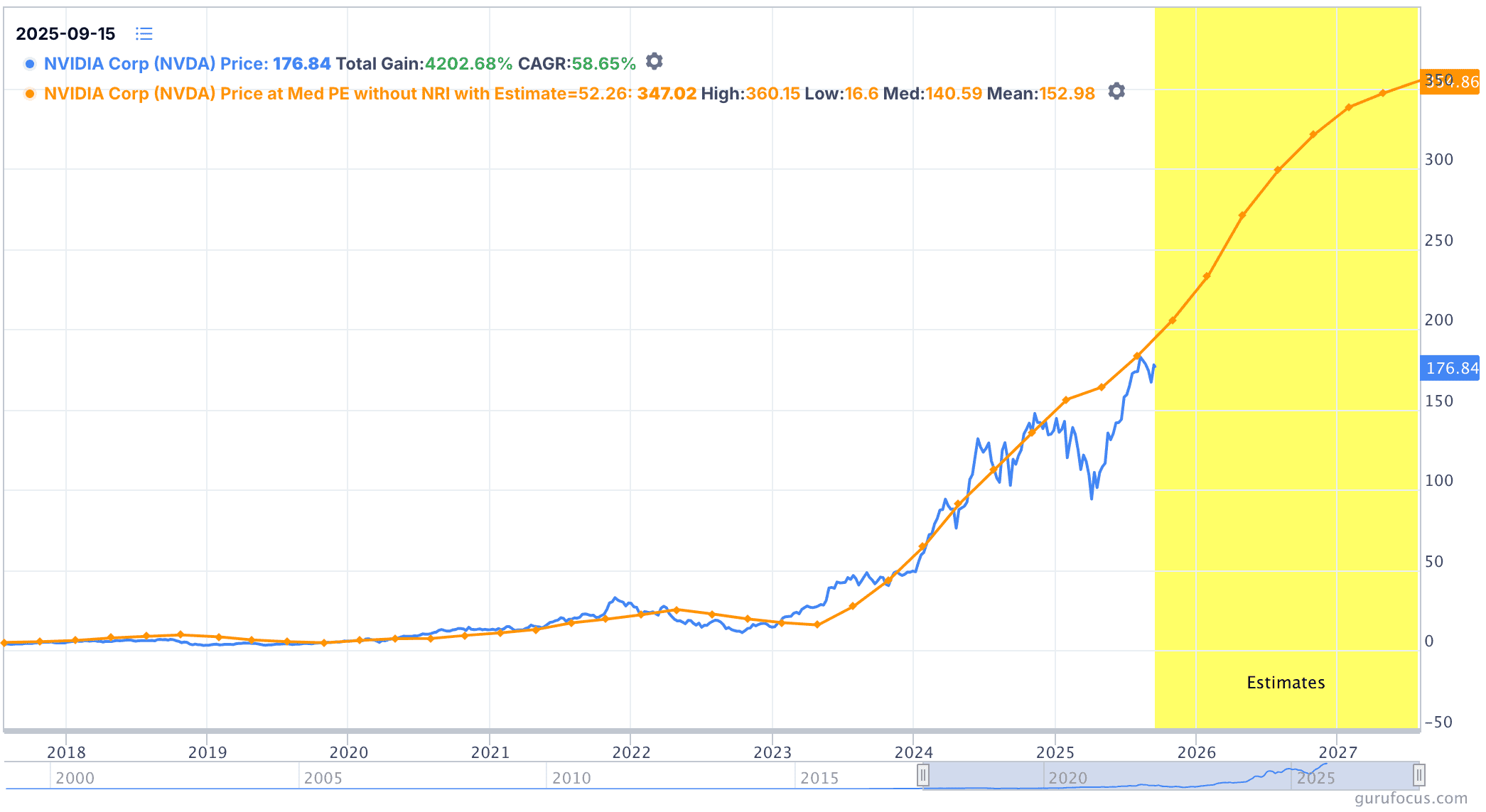

Now, if we extrapolate the existing median PE ratio out to mid-2027 with current earnings estimates, we get NVDA stock at over $350.

This may look outlandish today, but the AI rally has shown that it can outrun even the most bullish expectations. Even $300 means ~70% upside and will comfortably outperform the benchmark. I believe this is possible, especially as almost every other Nvidia competitor trades at a higher multiple despite having lower growth and inferior AI products.

The biggest caveat is that some hyperscalers are increasingly designing and adopting their own AI chips. So far, these chips have failed to fully substitute what Nvidia offers.

Palantir (PLTR)

Palantir has been unlike anything else the market has seen since the Dot Com bubble. The valuation is truly astounding. The bulls would answer by saying PLTR stock should be valued through free cash flow (which I agree with) instead of earnings. But even when you do that, it’s a very expensive stock. However, are you really paying for enduring quality?

Let’s first take a look at the momentum here.

Palantir has grown its revenue from $1.54 billion in 2022 to $2.9 billion in 2024. Analysts see revenue at $4.16 billion in 2025. Free cash flow in 2024 was $1.1 billion. In 2025, the higher end of free cash flow estimates put it at ~$2 billion. This means you’re paying over 200 times forward FCF for this year.

Revenue is estimated to be $5.7 billion in 2026. Analysts expect it to reach a 60% adjusted FCF margin in 2026, so that’s $3.42 billion, or over 117 times 2026 FCF. 2027 revenue is estimated to be $7.5 billion, and if Palantir maintains a 60% FCF margin, you’re still paying over 89 times FCF some three years out. That’s if Palantir can consistently meet the most bullish estimates for the next 12 quarters.

Dan Ives, the most bullish analyst on Palantir, believes it will be a $1 trillion company “within 3 years.” This is highly speculative. But if true, it implies ~150% upside over the next 3 years, something Nvidia is not too far behind.

PLTR or NVDA, which one should you buy?

PLTR stock can still be a very profitable investment many years out and will likely outperform the broader market. However, NVDA stock comes with a better risk-reward profile. The bullish argument for Nvidia is laid out clearly, with hyperscalers planning to spend trillions in total over the coming years.

Palantir’s accelerating growth is dependent on an increasing number of AI and government customers scaling its partnerships with the company. This story is more treacherous as AI lowers the bar for data + software competitors.