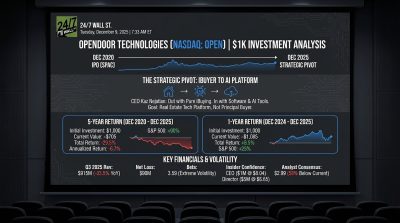

Opendoor Technologies (NASDAQ: OPEN) reported earnings after the market closed yesterday and beat on revenue but missed on profit, cut near-term expectations, and told investors the real turnaround is a 2026 story. The market is repricing that path today.

Quick stats investors care about

- Revenue: $915M, up vs. the $882.3M consensus, but down 33.5% YoY

- Adjusted EPS: –$0.12 vs. –$0.07 expected

- Gross margin: 7.2%, down from 11.5% a year ago

- Net loss: $90M, wider than last year’s $78M

- Cash: $962M, up 16% YoY

- Q4 outlook: revenue expected down ~35% sequentially on low inventory

The 7 reasons the stock is sinking

1) EPS miss and losses widening

Adjusted EPS of –$0.12 missed by five cents and the net loss expanded to $90M. That is a clear step the wrong way for profitability even with the revenue beat.

2) Shrinking top line

Revenue fell 33.5% year over year. Management framed the quarter as clearing legacy inventory rather than growth. Shrink now, maybe grow later is rarely rewarded in the short term.

3) Margin pressure

Gross margin compressed to 7.2% from 11.5% last year and contribution margin slid as older, lower-quality inventory moved out. Management said Q4 contribution margin will be below Q3 before improving as the mix resets.

4) Tough near-term guide

Q4 revenue is expected to fall about 35% quarter over quarter due to thin inventory after a slow buying period. Investors heard “lighter volumes and pressure now” before any rebound.

5) “2026” profitability timeline

New CEO Kaz Nejatian is “refounding Opendoor as a software and AI company” and targeting adjusted net income breakeven by year-end 2026 on a forward 12-month basis. That pushes the payoff out multiple quarters, which compresses near-term multiples.

6) Dilution and capital moves

To fix a balance-sheet “ticking clock,” Opendoor raised nearly $200M via its ATM in September and refinanced a large chunk of its 2030 converts with equity. The board also declared a warrant dividend (Series K/A/Z). Cleaning up risk is good, but added share overhangs and complexity often hit the stock first.

7) Strategy pivot means execution risk

Opendoor is tightening spreads, accelerating turns, and leaning into AI, inspections, and a D2C funnel. That is a different operating model than the old “buy big at wide spreads.” Pivots can work, but they usually bring choppy results while processes, pricing, and resale velocity get re-tooled.