Live: Will Opendoor Beat Earnings Tonight?

Quick Read

-

Opendoor (OPEN) reports Q4 earnings today. Consensus expects -$0.11 EPS and roughly $594M revenue (down 45% YoY). We’ll be updating this live blog with news and analysis. Simply stay on this page and new updates will appear automatically once Opendoor earnings cross newswires.

-

Polymarket traders price in 69.5% probability that Opendoor misses estimates.

-

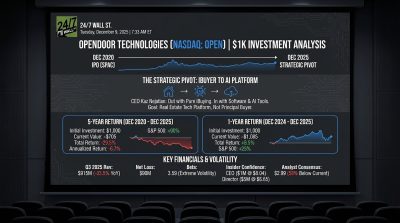

Opendoor purchased only 1,169 homes in Q3 (lowest since 2017 excluding COVID) and must reach 1,577 in Q4.

Live Updates

Opendoor's Call is Starting Now

Opendoor’s conference call is starting now.

Shares are still up 14%. We’ve outlined the reasons for the move in earlier updates, but the 46% growth in purchases and margin improvements loom large.

Up 12% After-Hours Despite Massive EPS Miss

Prediction markets collapsed from 37.5% beat probability on February 15 to just 0.6% today as traders anticipated another earnings miss. The actual Q4 results delivered exactly that: EPS of -$1.26 versus -$0.11 consensus, marking a massive 1,045% miss.

Yet shares surged 10%+ after hours. Markets priced in the loss but weren’t prepared for the operational pivot. Management’s 46% sequential growth in home purchases signals the new pricing algorithms are working, while October 2025 cohorts tracking to record contribution margins validates unit economics.

The real surprise: revenue of $746 million crushed the $594 million estimate by 26%, far exceeding management’s own guidance for a 35% sequential decline. Traders betting on a miss focused on the wrong metric entirely.

The Opendoor Metric Wall Street is Cheering: Margin Improvement

Opendoor issued Q1 2026 guidance signaling improving fundamentals despite near-term revenue pressure. Management expects revenue to decline approximately 10% quarter-over-quarter from Q4’s $746 million, but the margin trajectory tells a more compelling story.

The company projects an adjusted EBITDA loss in the low to mid $30 million range for Q1, a meaningful improvement from Q4’s loss. Management stated that contribution margin bottomed in September and has improved every month since, with Q1 exit rates expected to reach the highest level since Q2 2024.

The 46% sequential growth in home purchases demonstrates new pricing algorithms are driving volume without sacrificing unit economics. CEO Kaz Nejatian’s October 2025 cohort is tracking to deliver the strongest contribution margins of any October cohort in company history, validating the operational overhaul.

Shares climbed on the margin improvement narrative rather than revenue guidance.

Opendoor Executives Trumped 46% growth in Home Purchasing

Here are some of the quotes from OpenDoor’s release:

“Last quarter, we outlined a four-step plan to transform Opendoor: reach breakeven Adjusted Net Income by the end of 2026 on a 12-month go-forward basis, drive positive unit economics while increasing transaction velocity, transition to direct-to-consumer relationships, and expand our product suite. This quarter demonstrates we are executing on that plan,” said Kaz Nejatian, CEO of Opendoor. “These results reflect structural improvements in how we operate with more accurate pricing, faster inventory turns, and disciplined selection.

“The evidence of progress is clear. We increased our homes purchased by 46% quarter-over-quarter, significantly reduced our capital intensity by expanding Cash Plus such that it is now 35% of our weekly volume, and we reduced average days in possession of our inventory by 23%.

“Most significantly, our October 2025 acquisition cohort—both the first full month under the Opendoor 2.0 model and the first with mature sell-through data—is tracking to deliver the strongest contribution margins of any October cohort in Company history. And these homes are selling at more than twice the velocity of the October 2024 cohort, with over 50% already sold or under resale contract. While our newer cohorts are still early in their sell-through, we like what we see, and our Q1 2026 contribution margin guide post reflects our confidence in the trajectory for the portfolio.”

That 46% number will be carefully studied and is likely one of the biggest drivers of Opendoor’s surge after hours. Shares are now up 10.3%.

Opendoor's Guidance

Here’s the guidance Opendoor issued:

- Q1 2026 Financial Outlook:

- Acquisitions: You can track our acquisition contracts on accountable.opendoor.com1.

- Revenue: We expect a decrease of approximately 10% quarter-over-quarter.

- Contribution Margin2: Our contribution margin bottomed out in September and has been improving every month since. We expect to exit Q1 2026 with the highest contribution margin we’ve posted since Q2 2024.

- Adjusted EBITDA2: We expect Q1 2026 adjusted EBITDA loss in the low to mid $30 millions.

That guidance is significantly below Wall Street’s expectations, but investors don’t seem to mind. Shares are now up 11%.

Opendoor's Earnings Are Out - Here are The Key Numbers

Opendoor’s earnings just hit newswires, here are the most important numbers:

- Revenue: $746 million

- EPS: -$1.26

As a reminder, here’s what Wall Street was expecting:

- Revenue: $594.02 million

- EPS:-$0.11

Share are initially up 7% as investors are focusing on the revenue beat initially.

The Bull and Bear Case Before Opendoor Reports Q4 Earnings

Prediction markets show beat probability fell to 28% as of this afternoon, down from 37.5% on February 15. The steady erosion reflects mounting skepticism about Q4 results after management guided to a 35% sequential revenue decline due to low inventory.

Bull Case

- Q3 revenue beat estimates and $962 million cash provides runway for the AI pivot

- Management targets 35%+ acquisition growth from new pricing tools

- Breakeven adjusted net income by end of 2026 creates profitability visibility

Bear Case

- Net losses widened to $90 million in Q3 from $78 million prior year

- Revenue down 33.55% year-over-year with another steep drop expected

- Housing starts declined 5.8% year-over-year, pressuring transaction volume

Earnings Expected at About 4:05 p.m. ET

We expect Opendoor earnings to hit newswires at about 4:05 p.m. ET. If you see movement before then, it could just be noise. As a reminder, we’ll begin posting news and analysis once earnings are released.

Simply stay on this page and new updates will post automatically.

Opendoor Beating Quarterly Earnings Moving on Polymarket

The odds of Opendoor beating earnings tonight slipped as low as 14% at 11 a.m. this morning, but have rebounded to 32% currently.

Opendoor shares are up 4% today and have been steadily rising throughout the trading day.

Opendoor Technologies reports Q4 2025 earnings today after market close. Wall Street expects earnings of -$0.11 per share on revenue of $594.02 million, representing a ~45% year-over-year decline. Shares have fallen 25.68% over the past month, significantly underperforming the broader market. Here’s what investors should watch.

What Wall Street Expects

Analysts are focused on three critical metrics: unit economics, inventory turns, and the path to profitability under new CEO Kaz Nejatian. The consensus revenue estimate implies roughly $594 million, down approximately 35% quarter-over-quarter from Q3’s $915 million.

The earnings estimate of -$0.11 represents a slight improvement from Q3’s -$0.12 loss, but prediction markets tell a different story. Polymarket traders are pricing in a 69.5% probability that Opendoor will miss estimates, suggesting significant skepticism about the company’s ability to clear even this low bar.

What Happened Last Quarter

Q3 delivered a mixed bag. Revenue of $915 million beat the $849.6 million consensus, but earnings missed at -$0.12 versus the expected -$0.07. The company purchased just 1,169 homes in Q3, the lowest quarterly acquisition count since 2017 excluding COVID.

Management’s promise for this quarter was clear: increase acquisitions by at least 35% from Q3 levels while improving contribution margins after they bottomed in October. CEO Nejatian laid out an aggressive transformation, stating the company is “refounding Opendoor as a software and AI company” with a path to breakeven adjusted net income by end of 2026.

The stock initially dropped 16.1% following the Q3 report but recovered to close up 24.5% one week later, before giving back those gains in subsequent months.

The Metrics That Matter Most

First, watch acquisition volume. Management guided to at least 1,577 homes purchased in Q4 (35% above Q3’s 1,169). Hitting or exceeding this target would validate the new AI-powered pricing engine and direct-to-consumer initiatives Nejatian launched in his first 90 days.

Second, gross margins are critical. Q3’s 7.2% gross margin was down from 7.6% a year earlier. Management expects Q4 margins to dip below Q3 as legacy inventory clears, but any margin above 7% would signal the turnaround is gaining traction. The company needs to demonstrate it can achieve the 5% to 7% contribution margin target for 2026 profitability.

The wild card is strategic validation. Lennar’s 18.8 million share stake filed February 18 sent shares up 7%, but investors need to see this partnership translate into builder-channel volume growth. Watch for any commentary on the Opendoor Trade-in widget adoption or revenue contribution from new products launched in Q3.

Eric Bleeker has been investing for more than 20 years. He began his career working at Microsoft before joining Motley Fool, one of the largest publishers of financial research. In his 15 years at Motley Fool Eric served as the General Manager for Fool.com and led coverage in the Technology & Telecom sector. In addition, he was a featured columnist and has hosted dozens of investing seminars attended by more than a million total investors. Eric has more than 1,000 financial bylines to his name and has been featured in The Wall Street Journal, CNBC, Fox Business, and many other leading publications. He is currently focused on artificial intelligence investing and is a CFA Charterholoder.

© 24/7 Wall St