FedEx (NYSE: FDX | FDX Price Prediction) and UPS (NYSE: UPS) just wrapped up earnings that tell strikingly different stories. FedEx is expanding revenue and chasing operational fixes. UPS is shrinking its workforce and losing its largest customer while protecting margins.

Revenue Growth Versus Margin Defense

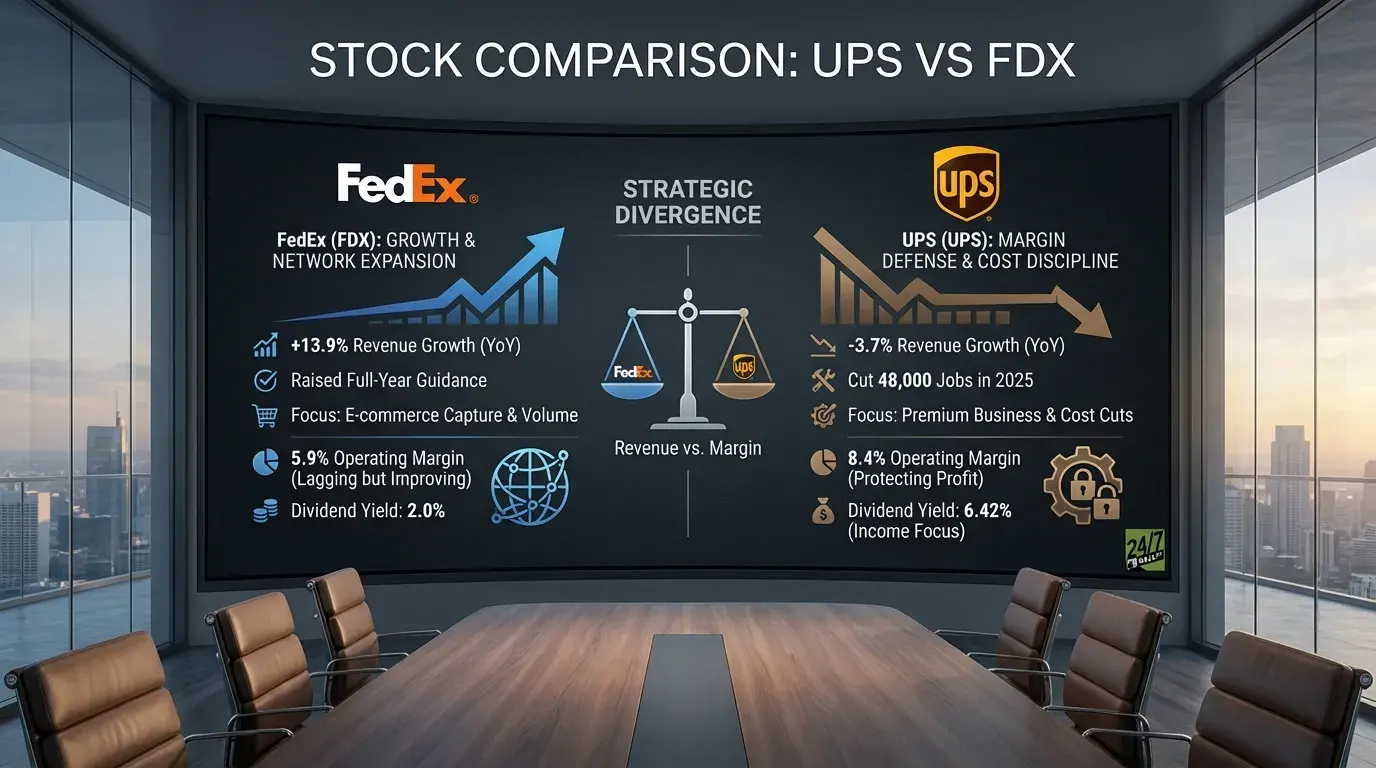

FedEx delivered a 17.27% earnings beat in fiscal Q2 ended November 30, reporting $4.82 per share against estimates of $4.11. Revenue climbed 13.9% year over year to $23.47 billion, driven by stronger Express segment performance. The company raised full-year revenue guidance to 5% to 6% growth, up from 4% to 6%. Operating margin sits at 5.9%, reflecting ongoing integration and network streamlining costs.

UPS beat expectations more dramatically in Q3, posting $1.74 per share versus $1.30 consensus, a 33.85% surprise. Revenue fell 3.7% to $21.4 billion as Amazon shipments dropped 21.2%, accelerating from a 13% decline in the first half. UPS cut 48,000 jobs this year, including 34,000 operational roles and 14,000 management positions. The workforce reduction pushed operating margin to 8.4%, well above FedEx’s 5.9%. CEO Carol Tomé expects $3.5 billion in cost savings for 2025.

| Metric | FedEx | UPS |

| Revenue Growth (YoY) | +13.9% | -3.7% |

| Operating Margin | 5.9% | 8.4% |

| Recent Earnings Beat | 17.27% | 33.85% |

| Workforce Change | Undisclosed | -48,000 jobs |

One Expands the Network, One Contracts It

FedEx is betting on volume growth and network optimization, investing in Express and Ground segments to capture e-commerce market share. The strategy accepts lower near-term margins for revenue scale and customer retention. FedEx has not disclosed seasonal hiring numbers for 2025, suggesting a more cautious staffing approach.

UPS is moving in the opposite direction. The company closed 93 leased and owned buildings through September and completed a sale-leaseback on five properties, generating a $330 million pretax gain. Rather than chase low-margin volume, UPS is focusing on higher-value shipments and business customers. The 6.42% dividend yield, more than triple FedEx’s 2.0%, signals management is prioritizing shareholder returns over growth.

| Strategic Focus | FedEx | UPS |

| Core Bet | Volume growth, network expansion | Margin protection, cost discipline |

| Customer Strategy | Broad e-commerce capture | Premium business accounts |

| Dividend Yield | 2.0% | 6.42% |

What Happens After the Holiday Rush

FedEx needs to convert revenue growth into margin expansion. The 5.9% operating margin lags industry standards and suggests the company is still absorbing integration costs. If Express and Ground segments continue improving and management executes on network consolidation, profitability should follow.

UPS must stabilize revenue while proving cost cuts do not damage service quality or customer relationships. Amazon’s accelerating exit creates a structural headwind that cost savings alone cannot offset indefinitely. The $3.5 billion in savings buys time, but UPS needs to replace lost volume with higher-margin business. Fourth-quarter guidance calls for 11% to 11.5% operating margin, which would validate the turnaround thesis.

Growth Versus Income Profiles

FedEx presents a growth-oriented profile with 13.9% revenue growth and raised guidance suggesting the company is winning market share. Margins will likely improve as integration costs fade, and the stock trades at 16x earnings.

UPS offers an income-focused profile with a 6.42% dividend yield. Management has demonstrated commitment to protecting profitability even at revenue’s expense. The stock is down 13.61% year to date, but the turnaround could unlock value if cost cuts translate to sustainable margin gains. Both companies face execution challenges over the next two quarters.