United Parcel Service (NYSE:UPS | UPS Price Prediction) stock traded at $100.49 as of midday Wednesday, down nearly 11% over the past week. The drop has handed a symbolic crown to its longtime rival.

In a historic moment, FedEx (NYSE:FDX) has quietly surpassed United Parcel Service in market value for the first time ever. It’s a milestone that would have seemed unthinkable just a few years ago, and there are major implications for UPS and FDX stock investors in 2026.

The Crown Changes Hands

The market-cap gap tells the story clearly. FedEx’s market capitalization now stands at approximately $84.6 billion, exceeding UPS’s $74.75 billion by roughly $9.9 billion. That gap is the result of two companies executing very different playbooks over the past year, with very different outcomes.

FedEx stock is up nearly 25% year to date and up 49% over the past year. UPS, by contrast, is down more than 10% over the past year and down more than 25% over the past five years. For a deeper look at how dramatically the two rivals have diverged over time, a decade-long look at how the two rivals have performed puts the gap in stark relief.

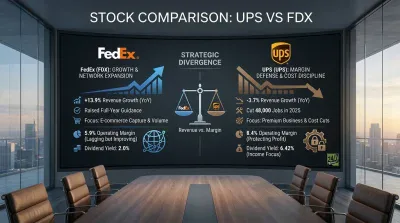

UPS reported full-year 2025 revenue of $88.66 billion, down 2.46% year over year, while operating income in the most recent quarter fell 13.76% year over year to $2.575 billion. The company beat earnings estimates, but the underlying volume story is hard to spin positively.

Moreover, UPS’s U.S. domestic package volume dropped 10.8% year over year in Q4 2025. This reflects both the ongoing Amazon (NASDAQ:AMZN) volume reduction and broader demand softness.

Amazon Hangover and the Cost of Transformation

Speaking of Amazon, UPS has faced persistent challenges from rising labor costs, declining volume, and investor skepticism around its relationship with Amazon. The company made a deliberate decision to reduce its dependence on Amazon, which was a low-margin customer.

However, the volume hole that strategy created has been painful to fill. UPS cut approximately 48,000 positions and closed 93 facilities in 2025 as part of its Network of the Future overhaul.

Now, UPS aims to close up to 200 manual package sorting facilities by 2030 and shift to automated hubs, a transformation that promises long-term margin improvement but creates near-term disruption. CEO Carol Tome has been direct about the timeline. “Upon completion of the Amazon glide-down, 2026 will be an inflection point in the execution of our strategy to deliver growth and sustained margin expansion,” she said when reporting UPS’s Q4 results.

UPS carries a dividend yield of approximately 6.3%, which looks attractive on paper. However, the dividend is not well covered by earnings or free cash flow, raising sustainability questions that are weighing on the stock. Full-year 2025 free cash flow came in at $5.47 billion, while the company guided for approximately $5.4 billion in dividend payments in 2026. That’s a thin margin of safety, to put it mildly.

FedEx Builds Momentum With DRIVE

In contrast, FedEx’s success is attributed to cost-cutting, margin improvement, and its plans to spin off its freight business. The company’s DRIVE cost savings program has been delivering real results.

To crunch the numbers quickly, FedEx reported Q2 fiscal 2026 revenue of $23.47 billion, up 6.84% year over year. The company also disclosed adjusted EPS of $4.82 beating the $4.11 consensus estimate by more than 17%.

Additionally, FedEx raised its fiscal 2026 revenue growth outlook to 5% to 6% and adjusted EPS guidance to a range of $17.80 to $19.00. FedEx’s Network 2.0 plan involves closing over 475 stations in North America by 2027, a more aggressive consolidation strategy than what UPS is executing. The cost savings are showing up in the margin line, with adjusted operating margin improving to 6.9% from 6.3% in the prior year period.

The planned spin-off of FedEx Freight into a separately traded entity under the ticker FDXF is scheduled for June 1, 2026. Investors appear to be pricing in the value unlock that separation could create, which helps explain why FedEx stock has outperformed so dramatically year to date despite a 5.65% pullback over the past week.

What to Watch

Both companies are navigating a freight environment complicated by higher oil prices hitting logistics operators across the sector, with WTI crude sitting near $87 per barrel after climbing from lows near $57 at the start of the year. Fuel costs are a real headwind for both carriers, but FedEx’s stronger revenue growth gives it more cushion to absorb that pressure.

The $100 level is a key technical reference point for UPS shares;d whether management provides any updated commentary on the Amazon transition timeline that might give investors more confidence in that “inflection point” promise. As for FDX stock, it’s settling comfortably at the $360 level for the time being.

Overall, the logistics industry is in the middle of a genuine restructuring, and the market-cap reversal between these two rivals isn’t just a footnote. It reflects a fundamental reassessment of which company is better positioned for the next phase of the delivery economy.

FedEx is executing, margins are improving, and a major catalyst in the freight spin-off is just months away. United Parcel Service has the right strategy on paper, but the execution timeline is long and the dividend math is tight. UPS faces continued headwinds until volume recovers and the Amazon transition is complete, so any share purchases should be considered with due caution.