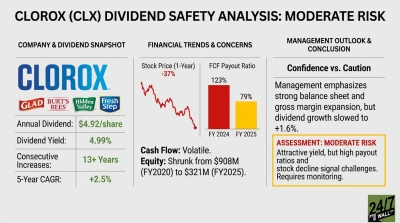

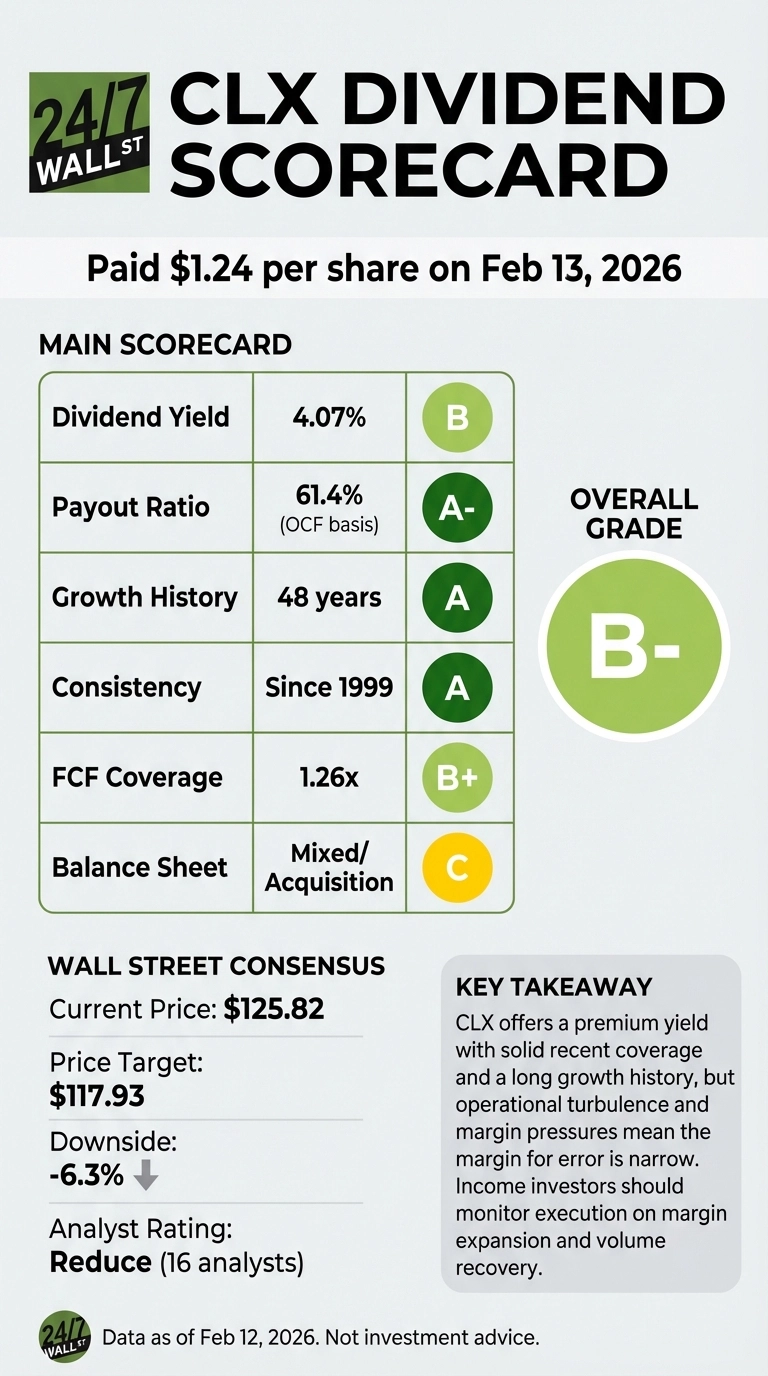

The Clorox Company just paid investors $1.24 per share on February 13, 2026, marking the latest payment in a 48-year streak of consecutive dividend increases. But the Dividend King’s crown sits uneasily on a company navigating operational turbulence and margin pressure that raises questions about whether this 4.07% yield compensates investors for the risks ahead.

Dividend Scorecard: Solid Coverage, But Stress Marks Visible

Clorox’s dividend earns a B- grade on sustainability metrics, reflecting adequate but not exceptional coverage ratios. The company generated $981 million in operating cash flow for fiscal 2025, covering the $602 million dividend payout at a 61.4% payout ratio. Free cash flow of $761 million provided 1.26x coverage after capital expenditures.

These figures represent a meaningful recovery from fiscal 2024’s concerning 85.6% payout ratio, when operating cash flow collapsed to $695 million – the lowest level in five years. Free cash flow that year fell to $483 million, providing just 0.81x coverage of the dividend. That was the only year in the past five where free cash flow failed to cover the payout.

The dividend itself has grown steadily, increasing 33.8% from $450 million annually in fiscal 2018 to $602 million in fiscal 2025, representing a compound annual growth rate of approximately 5.2%. Recent quarterly payments have stabilized at $1.24, up from $1.22 in the first half of 2025.

Yield Context: Premium to Sector, But At What Cost?

Clorox’s 4.07% dividend yield stands well above household products peers Procter & Gamble’s 2.63% and significantly above Kimberly-Clark’s 4.76%. This yield premium reflects investor skepticism about Clorox’s near-term prospects rather than superior dividend growth potential.

The stock has delivered a 26.21% year-to-date gain through February 12, 2026, rebounding from a challenging 2025. But zoom out and the picture darkens: shares are down 11.86% over the past year and 20.32% over five years. The elevated yield reflects a depressed stock price of $125.82, well below the $152.78 52-week high.

The ERP Hangover and Margin Squeeze

Clorox’s recent operational performance reveals why investors demand a yield premium. The company’s five-year, $580 million SAP enterprise resource planning implementation, completed in February 2026, caused significant disruption. Second-quarter fiscal 2026 results showed revenue of $1.67 billion but adjusted earnings per share of just $1.39, missing analyst expectations of $1.43.

More concerning than the ERP transition costs is the underlying business pressure. Gross margin has compressed to 43.2% as consumers trade down to cheaper alternatives, particularly impacting the household products segment. Sales volumes continue declining despite price increases, and management projects only flat to 1% organic growth for the back half of fiscal 2026.

The company’s 11.2% profit margin and 14.1% operating margin trail P&G’s 19.3% and 26.3% respectively, highlighting Clorox’s efficiency disadvantage against larger peers. The 20x forward price-to-earnings ratio appears reasonable only if operational improvements materialize.

Strategic Moves Add Complexity

Management’s $2.25 billion acquisition of GOJO Industries, maker of Purell hand sanitizer, announced in early 2026, strengthens the health and hygiene portfolio but adds integration risk during an already challenging operational period. The company also faces a $14.15 million Consumer Product Safety Commission fine for delayed warnings about bacterial contamination in Pine-Sol products, involving 37 million bottles recalled.

Clorox repurchased $332 million worth of shares in fiscal 2025, suggesting management confidence in the valuation. Yet institutional investors show mixed conviction: while Wealthfront Advisers increased its stake 93.8% and ProShare Advisors added 11.7%, Nuance Investments reduced holdings 18.1% despite Clorox remaining its largest position.

What Income Investors Should Watch

The dividend appears safe in the near term based on cash flow coverage, but the margin for error has narrowed. Management reaffirmed full-year fiscal 2026 adjusted earnings guidance of $5.95 to $6.30 per share despite the second-quarter miss, projecting gross margin expansion in the back half. Whether that materializes depends on consumers stabilizing their purchasing patterns and the company realizing cost savings from the completed ERP system.

Clorox CEO Linda Rendle and CFO Luc Bellet present at the CAGNY Conference on February 19, 2026, where investors will scrutinize guidance for fiscal 2027 and the timeline for margin recovery. Management has warned of a temporary inventory reset in 2026 that could further pressure profits.

The 48-year dividend growth streak provides historical comfort, but recent cash flow volatility, particularly fiscal 2024’s coverage shortfall, demonstrates that even Dividend Kings face business cycle pressures. The current 4.07% yield compensates investors for operational uncertainty, but only if the company executes on margin expansion and returns to volume growth. For now, the dividend checks clear, but the premium yield exists for a reason.