Software stocks have split into two camps in 2026. The winners are printing money with expanding margins and accelerating growth. The losers are treading water despite solid execution. What separates them? Profitability at scale, not just revenue growth. The market is done rewarding unprofitable expansion. It has started paying premiums for companies that convert dominance into actual earnings power.

We ranked the top five software stocks by weighing profitability metrics, revenue growth, and competitive positioning. A $3.5 trillion giant grinding out 35% profit margins deserves respect. So does a $415 billion company growing revenue 63% while delivering 28% profit margins. The common thread: these companies make real money while growing faster than their peers.

5. Fortinet

Fortinet (NASDAQ:FTNT | FTNT Price Prediction) delivers the highest return on equity in software at 228%. The cybersecurity specialist converts every dollar of shareholder capital into $2.28 of profit. With a 32x P/E ratio, 14.4% revenue growth, and 28.6% profit margins, Fortinet represents the old guard of cybersecurity executing at peak efficiency.

The stock is down 17% over the past year, trading at $78.80, but business fundamentals remain rock solid. Operating margins of 31.7% show pricing power in a competitive market. While newer players like CrowdStrike (NASDAQ:CRWD) and Zscaler (NASDAQ:ZS) grab headlines, Fortinet quietly compounds shareholder value through disciplined capital allocation and consistent profitability.

4. Intuit

Intuit (NASDAQ:INTU) posted 41% revenue growth year over year, the highest among profitable software companies in this analysis. The financial software leader expanded earnings per share from $2.64 in fiscal 2015 to $16.97 in fiscal 2024, representing 543% growth over nine years. The most recent quarter delivered $3.34 EPS, beating estimates by 8.1%.

The company trades at a 43x P/E ratio with a $176 billion market cap. Intuit has beaten analyst estimates for eight consecutive quarters, including a 66.7% surprise in Q4 fiscal 2025. The combination of 21.2% profit margins, 22% ROE, and accelerating revenue growth makes Intuit a compounding machine in financial software.

3. Oracle

Oracle (NYSE:ORCL) delivered a 38.7% earnings beat in its most recent quarter, reporting $2.26 EPS versus $1.63 estimates. That’s the kind of surprise that validates a multi-year cloud transformation. The database giant now sports a $553 billion market cap with 14.2% revenue growth and 69% ROE.

The stock gained 18% over the past year, reaching $194.03, as the market recognized Oracle’s cloud infrastructure momentum. With 25.3% profit margins and a 37x P/E ratio, Oracle trades at a premium to its historical range. The valuation reflects confidence that the company can maintain double-digit growth while expanding margins. The cloud migration strategy is working, and the recent earnings beat shows acceleration.

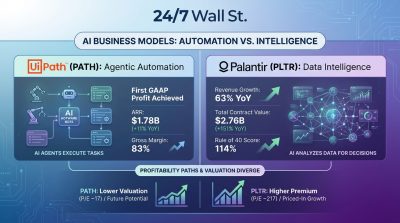

2. Palantir

Palantir (NYSE:PLTR) exploded 139% over the past year to $179.53, making it the best-performing software stock in this analysis. The data analytics company grew revenue 62.8% year over year while posting 28.1% profit margins and 33.3% operating margins. That combination of hypergrowth and profitability is rare.

The 396x P/E ratio reflects extreme optimism about Palantir’s AI platform and government contracts. The company delivered $0.21 EPS in Q3 2025, beating estimates by 23.5%, with annual EPS growing from $0.37 in 2024 to $0.50 in 2025. Reddit sentiment swings wildly on Palantir, with 10 times more discussion than Microsoft, showing retail enthusiasm. The valuation requires perfect execution, but the company is delivering on both growth and profitability.

1. Microsoft

Microsoft (NASDAQ:MSFT) sits at the top with a $3.51 trillion market cap, 35.7% profit margins, and 48.9% operating margins. The software giant grew revenue 18.4% year over year while maintaining a 34x P/E ratio and 32.2% ROE. This is what dominance looks like: massive scale combined with margin expansion and steady growth.

The most recent quarter delivered $3.72 EPS versus $3.66 estimates, marking the fourth beat in five quarters. Annual EPS grew from $11.81 in fiscal 2024 to $13.64 in fiscal 2025, representing 15.5% growth. The stock gained 14.7% over the past year to $476.60, though it’s down 1.45% year to date as investors take profits after a strong 2025.

Microsoft’s Azure cloud platform, Office 365 subscription base, and AI infrastructure investments create multiple growth vectors. The company prints $35.7 of profit for every $100 of revenue while growing faster than most companies one-tenth its size. That’s the ultimate software business model: scale, margins, and growth all moving in the right direction simultaneously.

These five stocks share a common trait that separates them from struggling peers like Snowflake (NYSE:SNOW) and CrowdStrike. They convert revenue into profit at scale. The market rewarded that discipline with premium valuations and strong stock performance. Software is eating the world, but only the companies that can digest their growth into earnings are worth owning at these prices.