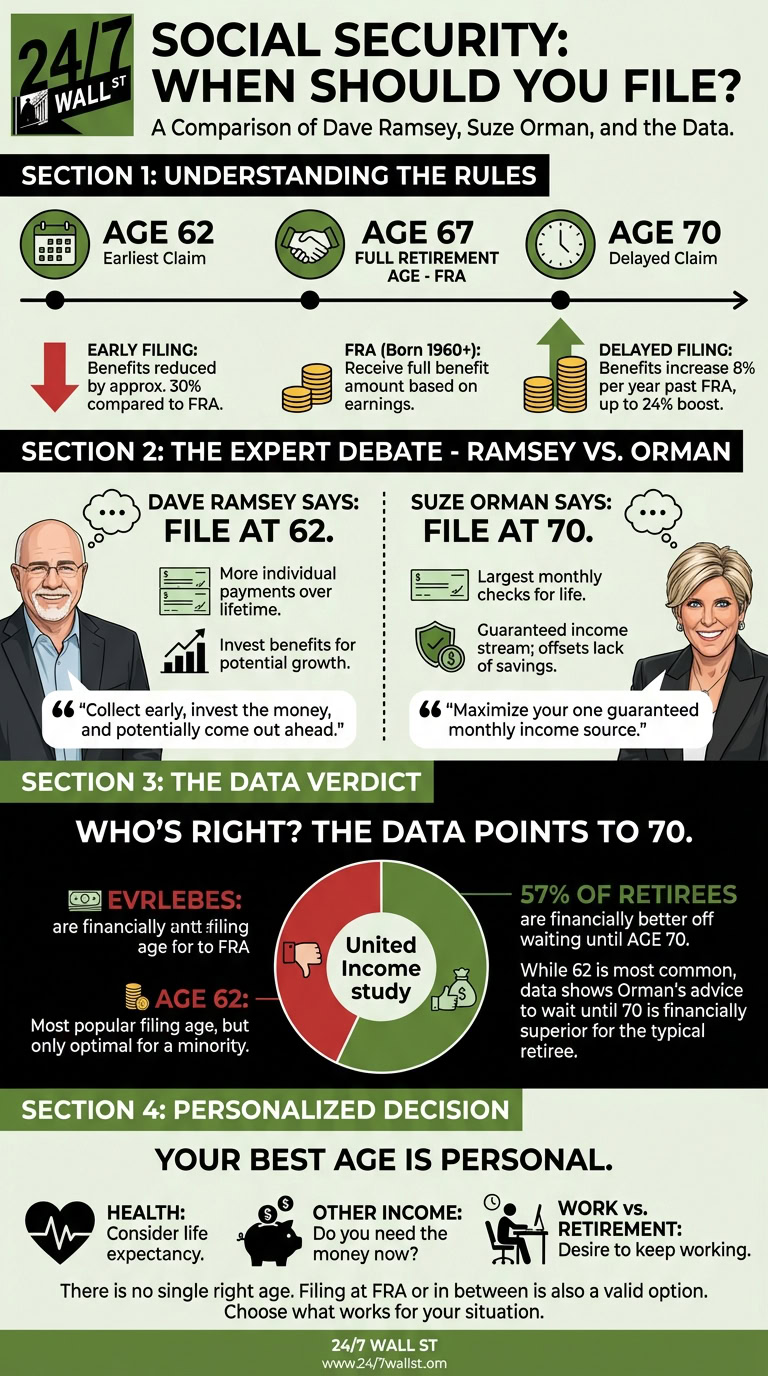

There’s a reason it’s important to put a lot of thought into your Social Security filing decision. The age you sign up for benefits will help determine how much monthly income you get from the program.

If you file for Social Security at your full retirement age (FRA), which is 67 for anyone born in 1960 or later, you’ll get your precise monthly benefit based on your earnings history without a boost or reduction. However, you have many other choices.

The earliest age to claim Social Security is 62. Filing at that point will reduce your monthly benefits by about 30% compared to an FRA of 67.

You can also score an 8% boost to your monthly Social Security benefits for each year you delay your claim past FRA. That incentive runs out once you turn 70. But with an FRA of 67, you could give your benefits up to a 24% raise.

Financial experts Dave Ramsey and Suze Orman have opposite views when it comes to the optimal age for claiming Social Security. But data shows that one of them may have better guidance than the other, broadly speaking.

Dave Ramsey’s advice on Social Security

Dave Ramsey thinks 62 is the best age to sign up for Social Security. The reason is that the earlier in life you start collecting that money, the more individual payments you’re apt to get.

Plus, Ramsey’s logic is that if you invest your Social Security benefits rather than spend them, you can more than make up for the reduction that comes with filing early.

Suze Orman’s advice on Social Security

Suze Orman thinks 70 is the best age to sign up for Social Security. The reason is that claiming benefits at 70 results in the largest monthly checks.

Having more generous benefits is a great way to make up for a lack of retirement savings — something many older Americans struggle with. Plus, Social Security may be your one guaranteed income stream in retirement, so it’s a good thing for your checks to be larger each month.

Ramsey vs. Orman: Who’s right on Social Security?

Let’s be clear. There’s no such thing as a right or wrong age to file for Social Security. That choice depends on the person. And the right age for one retiree may not be the right age for another.

That said, on a broad level, there’s data supporting Orman’s advice to claim Social Security at 70 rather than sign up at the earliest possible age of 62.

A few years ago, investment firm United Income examined the long-term financial effects of various Social Security filing decisions. And it found that 57% of retirees would come out ahead financially if they waited until age 70 to take benefits.

Of course, the data also found that only 4% of retirees typically sign up for Social Security at age 70. By contrast, age 62 has long been the most popular age to claim Social Security, since it’s the earliest point in time to get benefits.

But from the perspective of building retirement wealth, the data seems to say that Orman is correct, and that 70 is the ideal Social Security filing age for the typical retiree.

That doesn’t mean that filing for Social Security at 70 is right for you, though. You’ll need to take different factors into account, including your health, other income streams, and desire to keep working versus retire, when making that choice.

Remember, too, that you don’t have to follow Ramsey or Orman’s advice. Rather than file at the earliest possible age of 62 or the latest age of 70, you could meet in the middle by claiming Social Security at FRA, or a little bit before or after. You may find that that works better for you, and there’s absolutely nothing wrong with that.