Dave Ramsey is full of financial advice. And much of it tends to follow a similar pattern: Save money. Avoid debt. Repeat.

Ramsey also thinks Americans need to be very careful when it comes to claiming Social Security. But his advice might surprise you. And it might also be pretty tough for the typical retiree to follow.

How Ramsey suggests Americans manage their Social Security benefits

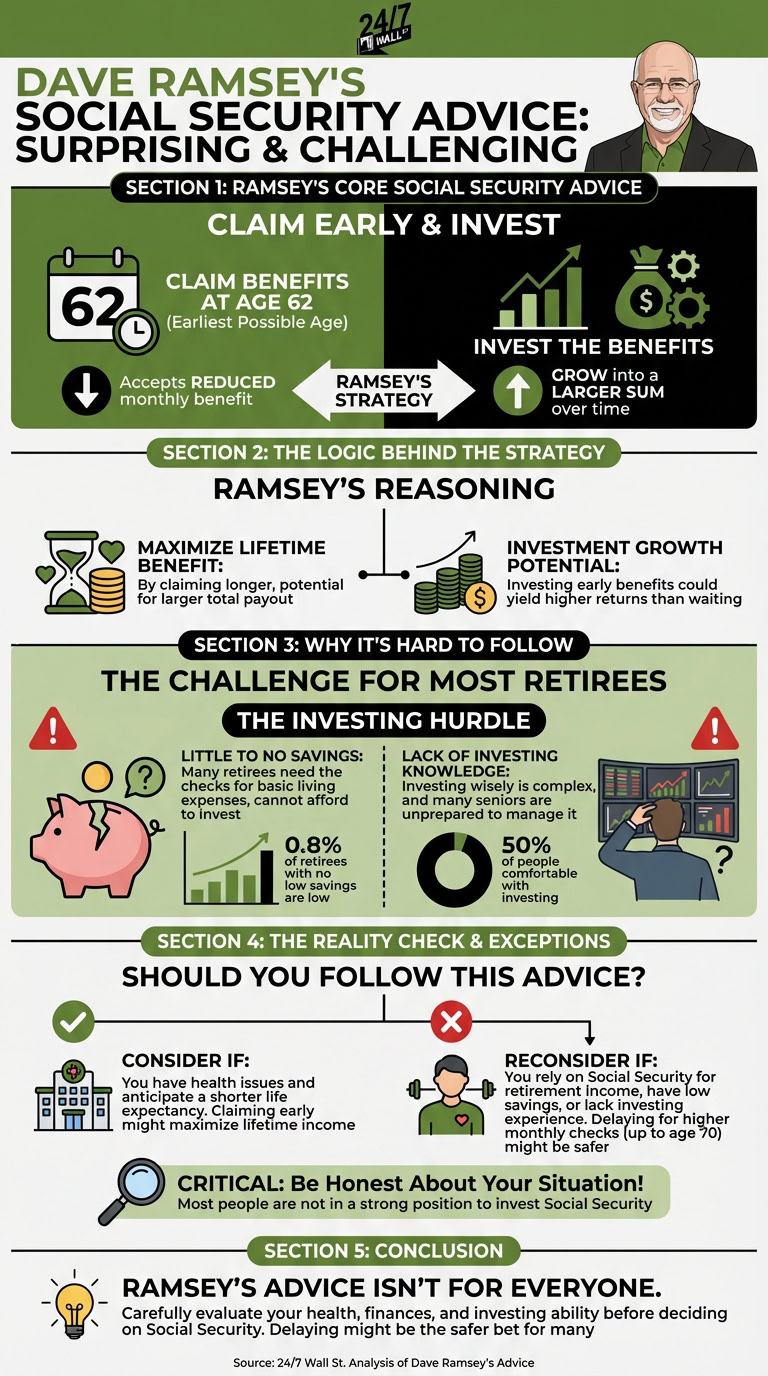

When it comes to Social Security, recipients have choices as to when to file. The earliest age to claim benefits is 62. But anyone wanting their monthly benefits without a reduction will need to wait until full retirement age (FRA), which is 67 for people born in 1960 or later.

It could also pay to delay Social Security past FRA. Each year that happens boosts benefits by 8%, up until age 70.

Now based on the type of advice Ramsey tends to give out, one might assume that his advice on Social Security is to delay benefits as long as possible for the largest possible monthly checks. Surprisingly, though, Ramsey actually thinks it’s wise to claim benefits at the earliest possible age of 62, despite the reduction that leads to.

Ramsey’s logic is twofold. First, he figures that since people only get to collect Social Security for as long as they’re alive, filing early could, for a lot of people, mean locking in a larger number of monthly checks and therefore a larger lifetime benefit.

Ramsey also suggests that Social Security claimants take benefits at 62 and invest the money. That way, they can grow it into a larger sum.

Why Ramsey’s advice is so hard to follow

Ramsey’s advice to claim Social Security at 62 isn’t particularly tough. In fact, 62 has long been the most popular age to file for Social Security. Rather, it’s the investing part that will likely trip most seniors up.

First, many people enter retirement with little to no money saved. So the typical retiree can’t afford to invest their Social Security checks because they need the money to live on.

Secondly, many Americans don’t know how to invest. Even if the money isn’t needed to cover near-term expenses, handing the typical retiree a Social Security check each month and trusting them to invest it wisely is pushing it.

Therefore, Ramsey’s advice is pretty surprising. Ramsey probably knows full well that the typical American needs their Social Security for income once they claim benefits and isn’t in a strong position to invest it. Based on that, it would make more sense for Ramsey to suggest that filers delay their claims for larger monthly payments.

The thing that may be getting in the way of that guidance is longevity risk. Although life expectancies are increasing, many Americans have chronic health problems. So Ramsey may be thinking that claiming Social Security at 62 is the safest bet from a lifetime income perspective.

Should you follow Ramsey’s Social Security advice?

Although Ramsey’s Social Security advice may be appropriate for some people, you need to be honest with yourself. If you need your Social Security checks to cover your retirement expenses and don’t have a lot of savings, you may not be able to afford to reduce those benefits by claiming them early.

Also, if you’re old enough to claim Social Security but have never so much as invested a dollar of your money, you’re probably not going to start now. So rather than pretend you will, you may want to sit tight on Social Security and claim benefits at FRA or later.

The one scenario where it makes sense to listen to Ramsey is if you have health problems and don’t think you’re destined to live a long life. Otherwise, think carefully about when you take benefits, and don’t necessarily rush to claim them right away.