Dave Ramsey has made a name for himself by giving out financial advice. And a lot of it is pretty spot-on.

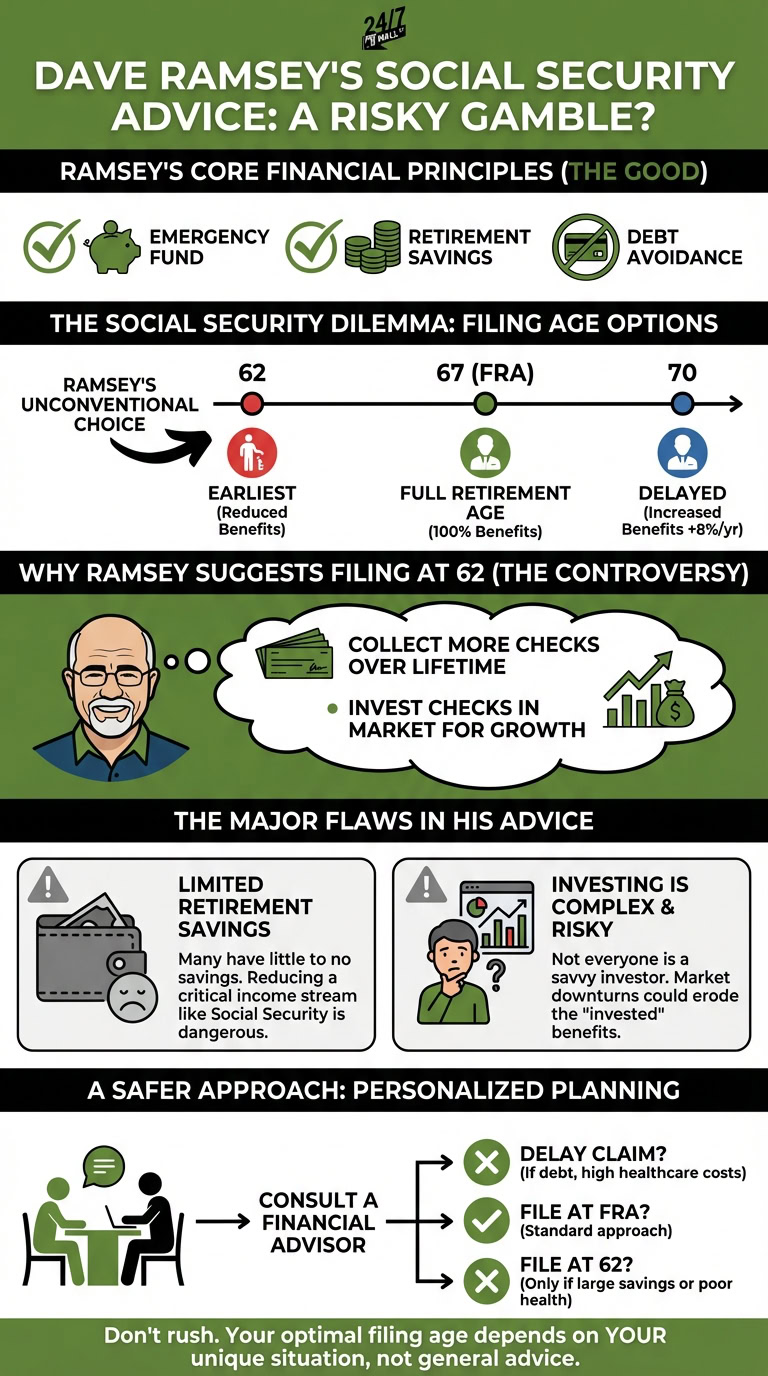

Ramsey is a firm believer in attaining financial security. To that end, he advocates maintaining an emergency fund at all times and saving money for retirement. He also strongly urges consumers to do what they can to avoid debt, and to prioritize paying off whatever debt they’ve already racked up.

Because of this, you’d think Ramsey would be pretty cautious with regard to claiming Social Security. But actually, his advice is somewhat reckless when it comes to taking benefits. And following it could seriously put your retirement at risk.

Ramsey’s ideal Social Security filing age

When it comes to claiming Social Security, you have choices. The earliest age you can take benefits is 62. But you won’t get your benefits without a reduction until you reach full retirement age (FRA), which is 67 if you were born in 1960 or later.

You can also delay your Social Security claim beyond FRA. For each year you do, until you reach the age of 70, your benefits get a permanent 8% boost.

You’d think Ramsey would suggest filing for Social Security at FRA, or even at age 70, since that guarantees larger monthly checks. Surprisingly, though, he’s a fan of claiming Social Security at 62.

The reason for this is twofold. First, because you only get to collect a Social Security check each month for as long as you’re alive, Ramsey feels that by filing as early as possible, you can collect a greater number of individual checks in your lifetime — even if they’re smaller each month.

Furthermore, Ramsey thinks that if you invest your Social Security checks, you can more than make up for the reduction that comes with filing for benefits early — especially if you’re willing to put that money into the stock market.

Why Ramsey’s advice is flawed

Ramsey’s Social Security advice may be well intentioned, but it’s flawed for a couple of reasons.

First, many Americans do not have any savings for retirement whatsoever. And even among people with savings for their senior years, there’s not necessarily a lot of money to go around. Reducing a critical income stream like Social Security could put a lot of people’s financial stability at risk.

Also, many people aren’t comfortable investing money, nor do they know how to do so in a savvy manner. So unless you’re a seasoned investor, you may not come out ahead financially if you reduce your monthly Social Security benefits by filing early.

You may not want to file as early as possible

While Ramsey’s Social Security advice may work for some people, if you’re someone without much retirement savings and you don’t know a thing about investing, then you shouldn’t rush to follow it.

What should you do? Sit down with a financial advisor and figure out an optimal Social Security filing age based on your personal situation.

An advisor may suggest that you claim Social Security at FRA to avoid a reduction in those monthly checks. Or, they might suggest delaying your claim, especially if you’re entering retirement with debt or are anticipating large healthcare bills.

Granted, an advisor might also suggest that you file for Social Security at 62. But they’ll probably only tell you to do so if you have a large amount of money saved for retirement, or if you have health issues that make it likely you won’t live a long life. Otherwise, taking benefits at 62 could end up being pretty dangerous thing for your senior finances.