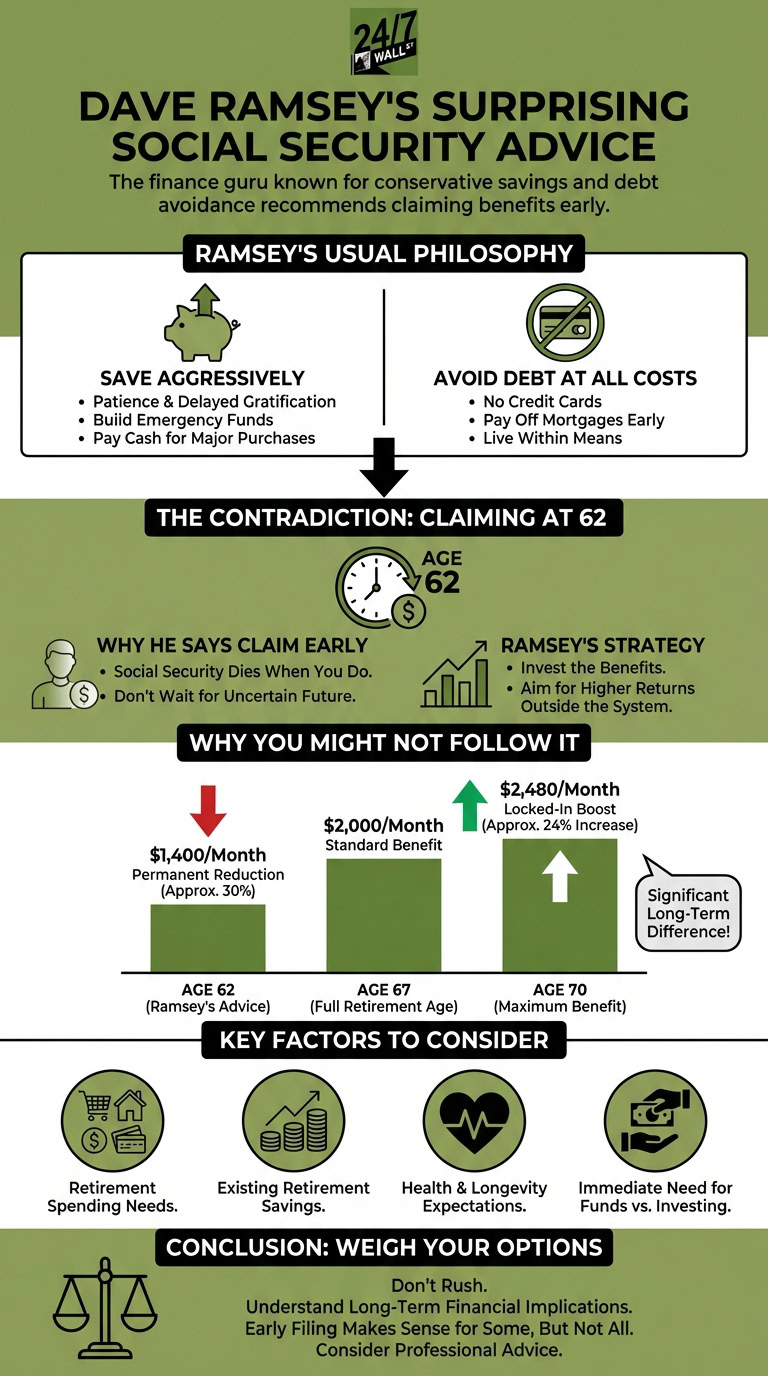

Dave Ramsey has created a name for himself in the world of personal finance as being extremely conservative when it comes to savings and debt. Ramsey feels that consumers should, on a whole, protect themselves with savings and avoid debt at all costs. He’s even gone so far as to suggest that Americans buy a house with cash when possible rather than take on mortgage debt.

It’s for this reason that Ramsey’s advice on Social Security is strange coming from him. But there’s a logic behind his guidance.

Why Ramsey’s Social Security advice defies his usual logic

At its core, Ramsey’s financial guidance centers on patience and delayed gratification. Ramsey thinks people should save money so they can afford the things they want — not rack up debt to get those things right away. This holds true in the context of everything from automobiles to clothing to vacations.

For this reason, it’s a little surprising that Ramsey suggests that Americans claim Social Security at the earliest age of 62. Waiting until full retirement age, which is 67 for people born in 1960 or later, means avoiding a reduction in those monthly checks. And delaying Social Security past full retirement age means locking in boosted monthly benefits for life.

Yet Ramsey thinks filing for Social Security makes the most sense, despite the reduction in monthly checks it results in. He insists that because Social Security dies when you do, you should start collecting that money as early as possible. He also thinks the typical person should ideally claim Social Security early and invest the money to grow those benefits into more.

You may not want to follow Ramsey’s advice

Part of Ramsey’s advice may be rooted in the fact that Social Security is facing financial challenges, and that the program’s rules could eventually change. But even so, at the end of the day, claiming Social Security early means locking in smaller monthly checks for life. That’s surprising advice coming from a person like Ramsey.

For this reason, you may want to follow Ramsey’s advice on building savings and avoiding debt. But when it comes to Social Security, you may want to take a different path.

Imagine you’re eligible for a $2,000 monthly Social Security check at age 67. If you file for benefits at 62 like Ramsey suggests, you’ll knock those monthly payments down to $1,400 permanently. But if you wait until age 70 to file for Social Security, you’ll set yourself up to collect $2,480 a month instead.

Of course, your Social Security claiming decision should be based on different factors, including:

- What your retirement spending needs look like

- How much money you have saved for your senior years

- How healthy or unhealthy you are, and how you expect that to impact your longevity

You should also consider what you need the money for. If you need your Social Security to cover living costs, investing the money like Ramsey suggests may not be feasible.

Also, you have to do pretty well as an investor to make an early filing make sense. That’s because you have to make up for the reduction in payments that comes with taking benefits at 62.

But all told, you shouldn’t rush to follow Ramsey’s advice on Social Security. That doesn’t mean filing for benefits at 62 doesn’t make sense for you. It just means you need to weigh other options and make sure you understand the long-term financial implications of taking benefits as early as possible.