When it comes to claiming Social Security, there are a lot of different opinions out there. Suze Orman, a noted financial expert, shared hers on LinkedIn not too long ago.

The financial expert warned in her post that making a specific decision about claiming Social Security could lead to a “costly cut.”

Here’s what Orman had to say about the Social Security claiming choice that could end up coming at a big cost.

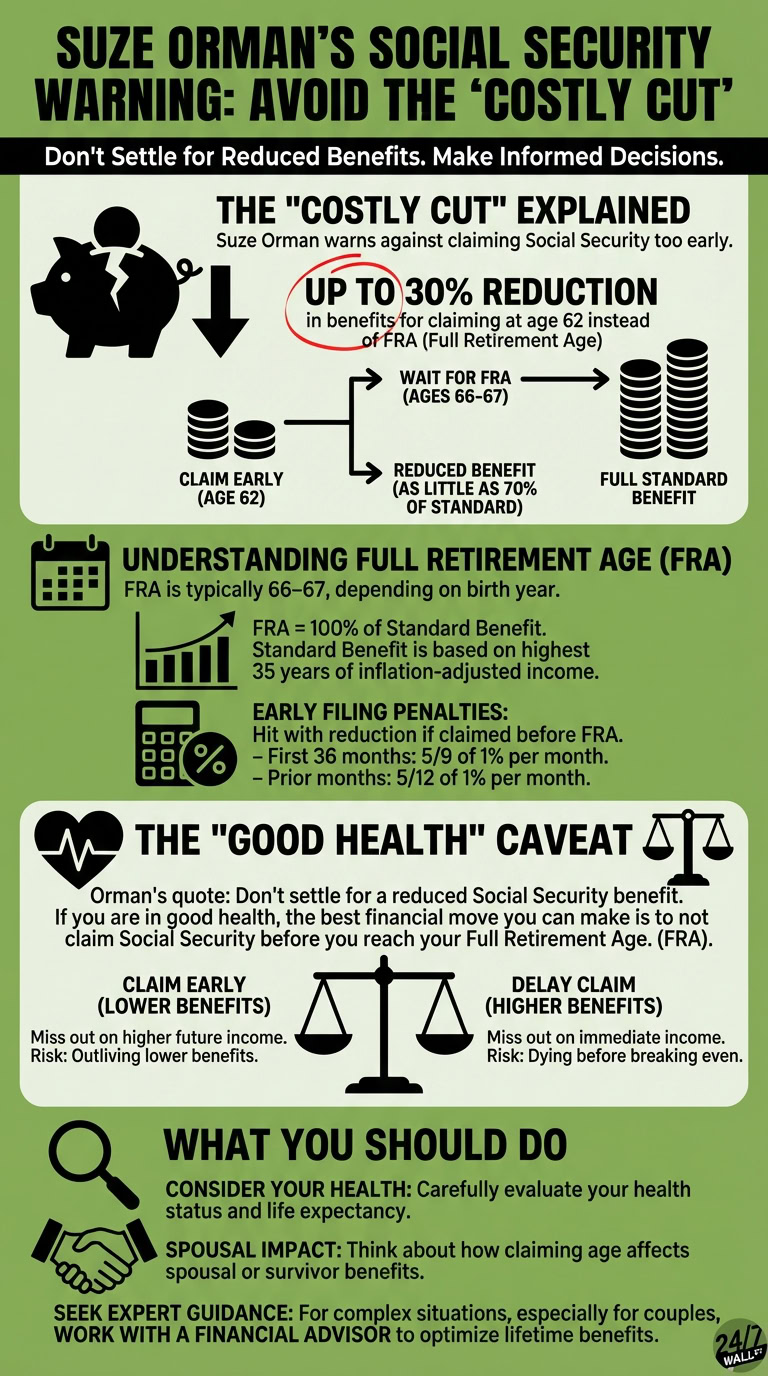

Orman warned against making this Social Security move

Orman’s warning was about claiming Social Security at too young of an age. You are allowed to start your benefits as early as 62, but Orman does not think you should do that.

As she explained, full retirement age (FRA) for most people is between the ages of 66 and 67, with the specifics depending on the year when you were born. You can collect the full standard benefit you are entitled to receive from this entitlement program if you wait to start benefits until your FRA. That standard benefit is based on average wages over the 35 years of your career when your inflation-adjusted income was the highest.

However, many people start their checks as soon as they can, even though that’s well before FRA. Orman said that doing this would lead to a “costly cut,” and she’s right. You are hit with early filing penalties if you claim benefits ahead of your FRA. Those are equal to 5/9 of 1% per month for each of the first 36 months, and to 5/12 of 1% for any prior month you claim benefits.

This adds up, and Orman explained your benefits could be worth as little as 70% of your standard benefit. If you claimed at 62 instead of at an FRA of 67, that’s exactly what would happen, as you’d be facing a 30% reduction in your benefits.

Does this mean you should never claim early?

While Orman warned about the costly cut that comes with an early claim, she did have a caveat to her advice. On her LinkedIn post, she said, “Don’t settle for a reduced Social Security benefit. If you are in good health, the best financial move you can make is to not claim Social Security before you reach your Full Retirement Age. (FRA).”

The “in good health” part of her statement is important. That’s because when you delay Social Security, you miss out on income you could have collected. It is not necessarily bad to miss out on those checks since you get higher ones later. However, you obviously want to get enough higher checks to make up for the missed income. If you don’t, say, because you die before breaking even, then you gave up some of your lifetime benefits for no reason.

You should carefully consider your health when making a decision on your claim, and should also think about things like how your claiming age could affect your spouse’s access to survivor or spousal benefits if they plan to claim either. This will help guide you in choosing the best claiming age.

The reality, though, is that it can be very confusing to make a decision, especially for married couples who have many different ways of optimizing lifetime benefits. The best option for most people is to work with a financial advisor to get some advice on the Social Security claiming age that truly makes the most sense, given your individual financial situation.