As a retiree, you are probably going to rely on Social Security for support, and you need to decide when you want your retirement benefit checks to start.

Suze Orman has some strong opinions on that, and listening to her advice could be well worth it. In fact, she has a stern warning that you need to read before you even consider claiming your monthly benefit from the Social Security Administration.

Here’s what Orman’s warning is, and why it is so important to pay attention to.

Listen to Suze Orman’s stern warning on Social Security

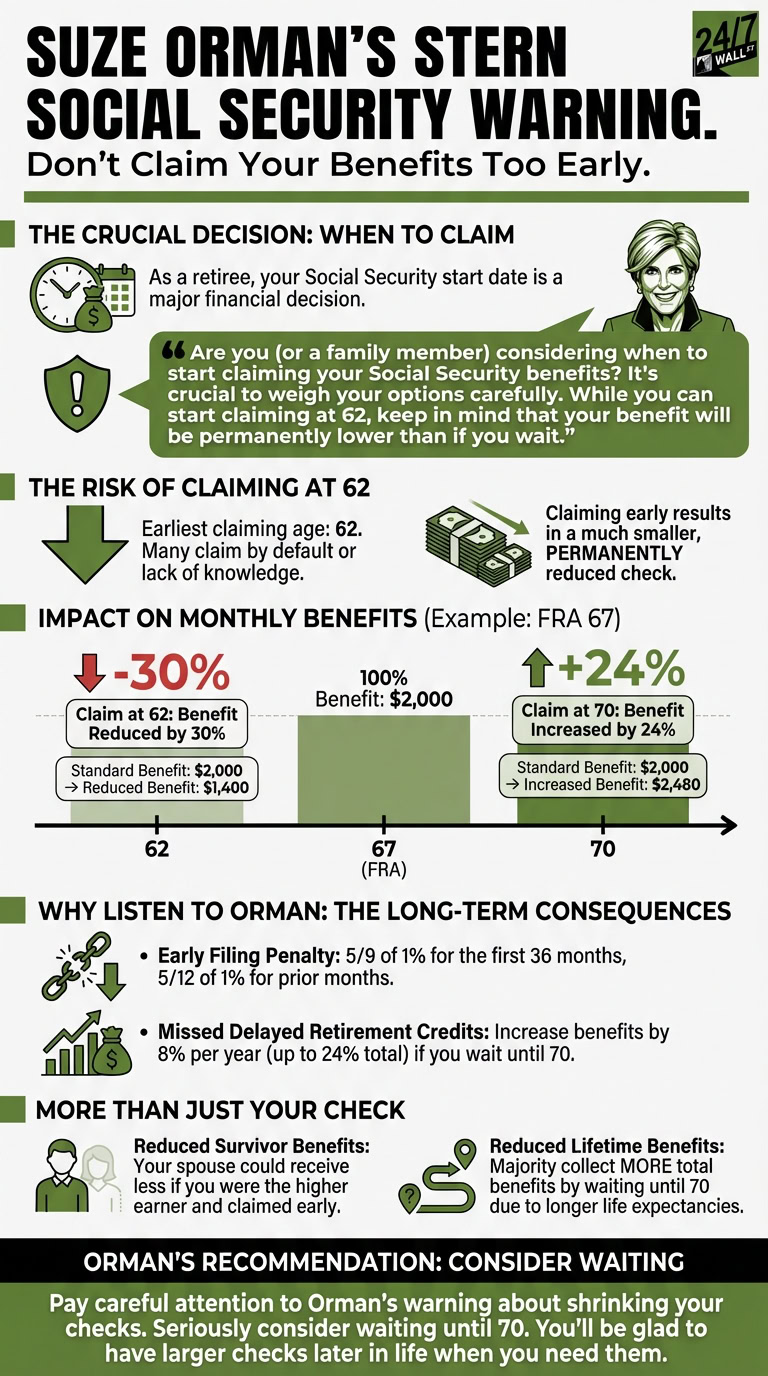

Orman issued her Social Security warning on LinkedIn, stating, “Are you (or a family member) considering when to start claiming your Social Security benefits? It’s crucial to weigh your options carefully. While you can start claiming at 62, keep in mind that your benefit will be permanently lower than if you wait.”

Orman has issued this warning because 62 is the earliest age when you can claim your Social Security retirement benefits. Many people start their checks then by default because they have been waiting to retire and think they need Social Security benefits to do it, or because they don’t really realize the implications of making this claiming decision. Since the government is ready to start sending you checks, it may also seem silly to wait to get that money.

However, as Orman points out, a claim at 62 would leave you with a much smaller Social Security check. You have a designated full retirement age, which is 67 years old for anyone born in 1960 or later. A claim before FRA reduces monthly benefits, leaving you with less guaranteed Social Security income. A claim after FRA increases monthly checks, giving you more money to live on later in life.

Many people don’t realize just how much they will reduce their Social Security with this early claim, or don’t know that the reduction is permanent and you can never catch back up to the monthly income you’d have had if you waited.

Why you should listen to Orman about when to claim Social Security

Listening to Orman about when to claim Social Security is a smart decision because an early claim can have serious long-term consequences for your finances.

Every month that you claim Social Security before full retirement age means getting hit with an early filing penalty equal to 5/9 of 1% for the first 36 months and 5/12 of 1% for any prior month. These penalties add up to reduce your monthly benefit by 30% if your FRA is 67 and you claim at 62. So, a standard benefit of $2,000 would fall to just $1,400 if you started it at 62. You’d also permanently forfeit the chance to earn delayed retirement credits that increase monthly benefits by 2/3 of 1% per month — which adds up to 8% per year and 24% total if you wait until 70 with an FRA of 67.

Not only will you reduce your check by hundreds of dollars with an early claim, but you will also reduce survivor benefits that your spouse could collect if you were the higher earner. And, you reduce your odds of maximizing lifetime benefits, as research has shown that the majority of people collect more total Social Security benefits by waiting until 70.

The reality is, many people now outlive the life expectancies that were the norm when Social Security was designed. While early filing penalties and delayed retirement credits were supposed to equalize out lifetime benefits for early and late filers, since so many people live longer now, it’s very common for people to do much more than break even for missed benefits when they wait until 70.

You should pay careful attention to Orman’s warning about shrinking your checks and seriously consider waiting until 70 for all of these reasons. When you have large Social Security checks coming late in life when you need them, you’ll be glad you did.