A 62-year-old retiree with $1.8 million faces a reality few anticipate: when they stop working matters as much as how much they’ve saved. This is about sequence-of-returns risk, where early retirement losses can permanently damage portfolio sustainability, even if markets eventually recover.

One Reddit user planning to retire in 2026 at 55 captured this tension: “I do think at times about retiring at what could be near the top of the market. But I’m not all that worried about what’s commonly referred to around here as SORR.” Their solution? Building spending flexibility into their budget rather than timing the market.

| Scenario Element | Details |

|---|---|

| Portfolio Value | $1.8 million |

| Retirement Age | 62 years old |

| Key Risk | Sequence-of-returns impact on withdrawal sustainability |

| Current Market | SPY at $677.58 (down 2% yesterday, up 14.5% over one year) |

The Math That Reveals the Danger

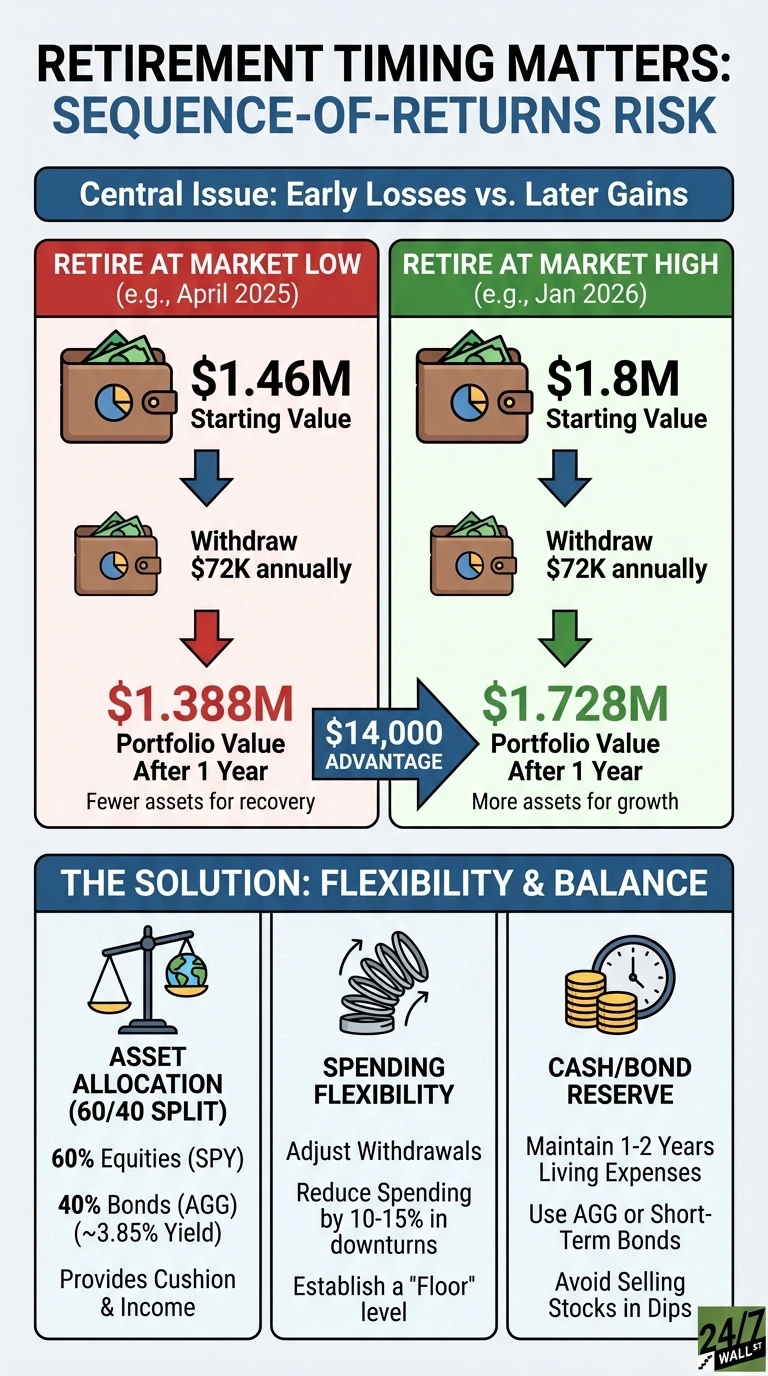

In April 2025, SPY dropped to $548.62 during sharp declines. By January 20, 2026, it recovered to $677.58, a 23.5% gain from that low.

For our $1.8 million retiree, this timing difference translates to roughly $342,000 in portfolio value. Someone who retired during April turbulence would have started with an effective portfolio of about $1.46 million. Someone retiring today starts with the full $1.8 million.

The damage compounds when withdrawals begin. Following the 4% rule means withdrawing $72,000 annually. When markets drop early in retirement, you’re forced to sell more shares to generate that $72,000, permanently reducing the asset base that can recover when markets rebound. As Schwab notes, “Not only does that drain your savings more quickly, but it also leaves you with fewer assets that can generate growth and returns during potential future recoveries.”

To illustrate this impact with concrete numbers: A retiree who started with $1.46 million in April 2025 and withdrew $72,000 would have $1.388 million remaining. If that portfolio then experienced the 23.5% market recovery, it would grow to approximately $1.714 million. Meanwhile, a retiree starting with $1.8 million today and withdrawing $72,000 would have $1.728 million remaining, a $14,000 advantage. This gap widens over time as the smaller portfolio has fewer assets generating returns.

Strategic Paths That Actually Work

The solution isn’t avoiding retirement during volatility. It’s building withdrawal flexibility and proper asset allocation. A balanced 60/40 portfolio split between equities (SPY) and bonds (AGG) provides cushioning. Over the past year, AGG gained 6.95% while maintaining monthly dividend distributions around $0.32 per share, providing predictable income without forcing equity sales during downturns.

Consider implementing a variable withdrawal strategy rather than rigidly adhering to 4%. The Variable Percentage Withdrawal method adjusts spending based on portfolio performance, requiring retirees to identify a “floor” spending level they can cut to if markets drop 50%. If you can reduce spending by 10-15% during market stress, you dramatically reduce sequence risk.

Another approach: maintain 1-2 years of living expenses in stable assets like AGG or short-term bonds. This reserve lets you avoid selling equities during temporary downturns. With AGG currently yielding approximately 3.85% and trading near $99.67, it provides both income and principal stability.

What to Evaluate Now

Financial advisors typically evaluate three key factors when assessing sequence-of-returns risk: spending flexibility (whether retirees can reduce expenses by 15-20% during market stress), asset allocation (balanced portfolios with 30-40% bonds versus 100% equity exposure), and retirement timing relative to market conditions. Advisors note that delaying retirement 6-12 months during extreme volatility can build additional cushion and reduce the percentage withdrawn, though this is about risk management rather than market timing.

The biggest mistake is assuming your $1.8 million will behave the same regardless of when you retire. It won’t.

This article is for informational purposes only and does not constitute personalized financial advice. Consult with a qualified financial advisor before making retirement decisions.