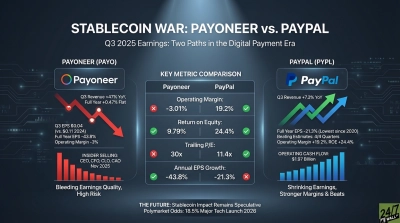

Fortive (NYSE: FTV | FTV Price Prediction) and Dayforce (NYSE: DAY) both reported Q3 2025 earnings that exposed fundamental cracks beneath their software-driven growth narratives. Fortive’s industrial automation platform saw earnings collapse 75% year-over-year despite modest revenue growth. Dayforce’s HCM software business swung from consistent profitability to a catastrophic loss that missed estimates by 686%.

One Bleeds Margin, The Other Burns Cash

Fortive’s Q3 revenue of $1.03 billion grew just 2.3% while net income plummeted from $222 million to $55 million. Operating margin compressed 390 basis points to 15.5%. Management blamed operational challenges, but the numbers tell a story of lost pricing power in automation and sensing businesses. Full-year 2025 EPS of $1.86 represents a 38% decline from 2024’s $2.99.

Dayforce posted Q3 revenue of $481.6 million, up 9.5%, but reported a net loss of $196.8 million against analyst expectations of a $0.21 profit. That’s not a miss. That’s a detonation. Operating margin sat at negative 25.8%. The company went from beating estimates in seven consecutive quarters to posting the worst quarterly result in its history. Full-year 2025 turned negative at -$0.04 per share after reaching $1.98 in 2024.

| Metric | Fortive | Dayforce |

| Q3 Revenue Growth | +2.3% YoY | +9.5% YoY |

| Operating Margin | 15.5% | -25.8% |

| Net Income | $55M | -$196.8M |

| Full-Year 2025 EPS | $1.86 (-38% YoY) | -$0.04 (from $1.98) |

Different Sectors, Same Execution Problem

Fortive operates in industrial automation, sensing, and software for manufacturing and healthcare. Its Intelligent Operating Solutions segment should benefit from factory digitization trends, but margin compression suggests competitive pressure or weak demand. The company generates positive cash flow and maintains a 0.55% dividend, but its elevated 20.75x P/E ratio leaves no room for continued earnings deterioration.

Dayforce sells cloud-based HCM software for payroll, workforce management, and talent acquisition. The 9.5% revenue growth shows customers are still buying, but the company is burning cash to acquire them. A negative 25.8% operating margin means Dayforce spends $1.26 in operating costs for every dollar of gross profit. That’s unsustainable without a clear path to profitability. The company trades at 5.83x sales despite losing money, pricing in a turnaround that hasn’t materialized.

Analysts See Limited Upside in Both

Fortive has 14 of 18 analysts at Hold with a $58.12 target price, implying just 3.4% upside. Dayforce shows similar caution with 15 of 16 analysts at Hold and a $69.92 target barely above current levels. Neither stock has momentum or conviction. Fortive’s 50-day moving average sits at $53.77, and the stock has dropped 10.65% over the past year. Dayforce is down 32% over five years.

I’d Wait on Both Until the Stories Improve

I’m not buying either stock today. Fortive’s margin compression and balance sheet stress (total assets down 30% quarter-over-quarter) suggest operational issues beyond cyclical softness. Dayforce’s profitability collapse raises questions about unit economics and management’s ability to scale efficiently. For industrial software exposure, wait for Fortive to stabilize margins above 18%. If you believe in the HCM market, Dayforce needs to show it can grow revenue without incinerating cash. Right now, both are execution stories without credible execution.