Social Security isn’t going bankrupt, but it’s heading toward a funding crisis that could reduce monthly checks by nearly a quarter within the next decade. Understanding what this means for your retirement income matters more than ever, especially if you’re within 10 years of claiming benefits.

What’s Actually Happening

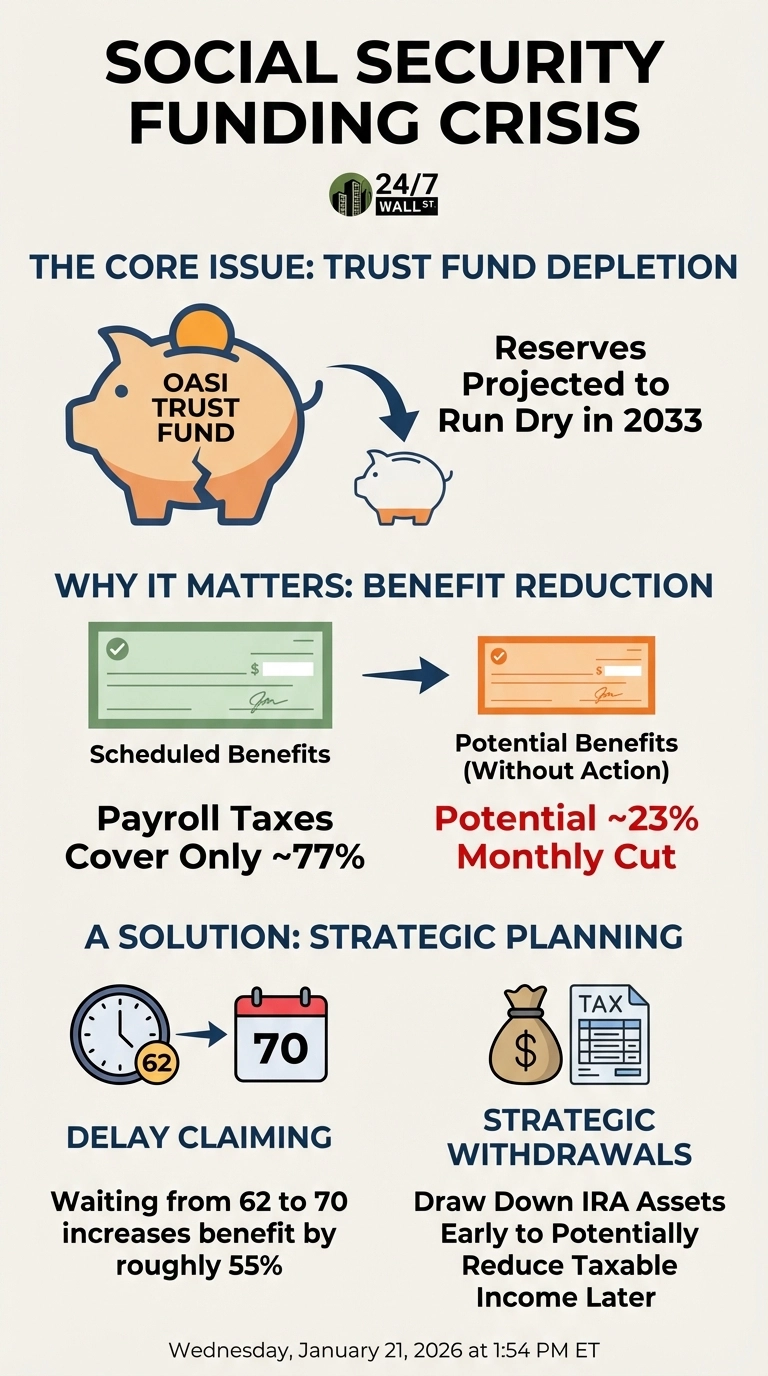

The Old-Age and Survivors Insurance Trust Fund faces a critical milestone in 2033 when its reserves are projected to run dry. This doesn’t mean Social Security disappears—payroll taxes from current workers will continue flowing in, but those taxes alone won’t cover full benefits. The gap between incoming revenue and promised payments creates the funding crisis.

Without congressional action, the program could only pay about 77% of scheduled benefits. For someone expecting $2,000 monthly, that means receiving closer to $1,540 instead. This isn’t just a number on paper—it forces real tradeoffs between housing costs, medical bills, and basic necessities that retirees depend on.

Couples face even harder choices as their combined income shrinks by hundreds of dollars each month.

Why This Matters for Your Claiming Decision

The timing of when you start benefits carries lasting consequences, and the looming shortfall makes this decision even more critical. Claiming early means locking in a permanently lower monthly amount, and that reduction compounds if Congress implements benefit cuts.

Many retirees weigh whether to claim early and secure guaranteed benefits now, or delay for higher monthly payments that might face cuts later. There’s no universal answer, but the math favors waiting if you have other savings to draw from in your early 60s. Even with a potential 23% cut in 2033, delaying from 62 to 70 still increases your monthly benefit by roughly 55% before any cuts are applied.

How Other Income Changes the Equation

Social Security doesn’t exist in isolation—it interacts with your other retirement income in ways that affect your tax bill. When your combined income crosses certain thresholds, up to 85% of your benefits become taxable. This creates an opportunity: drawing down IRA assets strategically before claiming Social Security can reduce your taxable income later, potentially keeping more of your benefits out of the tax net and preserving thousands over a 20-year retirement.

What to Think Through Now

Focus on what you can control. Review your savings and estimate how long they could sustain you if you delay claiming. Consider your health and family longevity patterns, since Social Security provides income for life. Recognize that Congress will likely act before allowing a 23% across-the-board cut, though the solution might involve some combination of benefit adjustments, tax increases, or raising the retirement age.

The goal isn’t to predict exactly what lawmakers will do. It’s to build a claiming strategy that works under multiple scenarios, understanding that Social Security remains a critical foundation even if it becomes a slightly smaller one.