Social Security faces a financial crossroads that’s closer than many Americans realize. The retirement program won’t actually “run out of money” since current workers will always pay into the system. But unless something changes, there won’t be enough funds to cover benefits at their current rates.

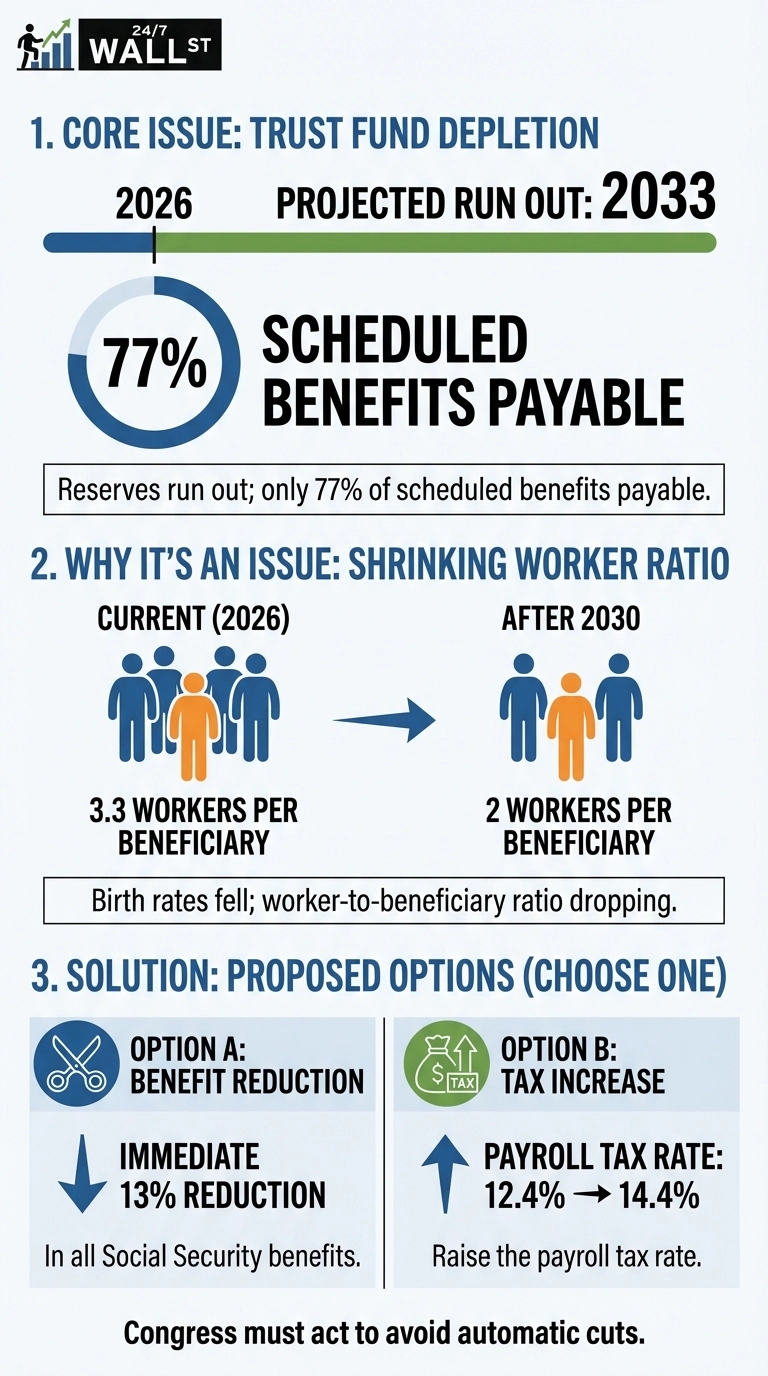

The program’s Old-Age and Survivors Insurance Trust Fund is projected to run out of reserves by 2033, at which point the system will only be able to pay 77% of scheduled benefits from incoming payroll tax revenue. Recent legislation has only accelerated Social Security’s path to insolvency. Two major bills—the Social Security Fairness Act and the One Big Beautiful Bill Act—added billions in costs over the next decade, draining reserves faster than anticipated. The approximately 70 million Americans currently receiving benefits face automatic cuts within the next decade unless Congress acts.

Why Social Security Is Running Short

The fundamental challenge isn’t longevity—it’s demographics. Birth rates collapsed after the baby boom, falling from over three children per woman to approximately two. This shift is squeezing the system: today’s 3.3 workers supporting each beneficiary will drop to just 2 workers after 2030, fundamentally changing the math that made Social Security sustainable.

The trust fund’s depletion reflects a widening gap between what the program collects and what it pays out. Wages and salaries reached $12,972.4 billion in the third quarter of 2025, up from the prior year, generating the payroll tax revenue that funds Social Security. But benefit payments are growing faster because more Americans are retiring and claiming benefits while the worker base supporting them shrinks. This structural imbalance is why the trust fund reserves are being drawn down each year.

What Happens When the Trust Fund Runs Dry

Many people misunderstand what insolvency means. Social Security won’t disappear—it will continue collecting payroll taxes from current workers. But without reserves to draw from, benefits must match incoming revenue. This creates an immediate shortfall that translates into real financial pain for retirees. For a typical couple retiring shortly after the trust fund depletion, this means an $18,400 annual benefit cut, though the exact impact varies depending on income level and work history.

Potential Solutions on the Table

Congress faces difficult choices to restore solvency, each with significant trade-offs. The most straightforward approaches would require either immediate sacrifice from current beneficiaries or higher taxes on current workers. A 13% immediate reduction in all benefits or an increase in the payroll tax rate from 12.4% to 14.4% would maintain full payments for 75 years, according to some estimates. Or a reform package might meet in the middle, asking both current beneficiaries and current workers to sacrifice. Other proposals include raising the income cap on payroll taxes, gradually increasing the retirement age from 67, or means-testing benefits for higher earners.

The advantage the United States has is time—though that window is closing. 2033 will be here before you know it. Unlike many countries facing similar challenges, annual trustee projections provide early warnings, allowing Congress to implement gradual changes that give affected generations time to adjust their retirement planning. The question is whether lawmakers have the political courage to act before automatic cuts become unavoidable.