Retiring at 62 with $1 million sounds comfortable, but the financial landscape has shifted dramatically over the past decade. What worked in 2016 faces different challenges today, from inflation to interest rate swings to healthcare costs before Medicare.

The Scenario at a Glance

- Age: 62 (earliest Social Security claiming age)

- Portfolio: $1 million in retirement savings

- Gap years: 3 years until Medicare eligibility at 65

- Social Security penalty: 30% permanent reduction for claiming at 62 vs. full retirement age of 67

- Key concern: Making savings last 25-30 years amid higher costs

On Reddit’s financial independence forum, one user noted the difference between retiring at 42 with $1.26 million versus 62 with the same amount, highlighting concerns about bridging the gap to Social Security and Medicare while preserving capital.

The Purchasing Power Problem

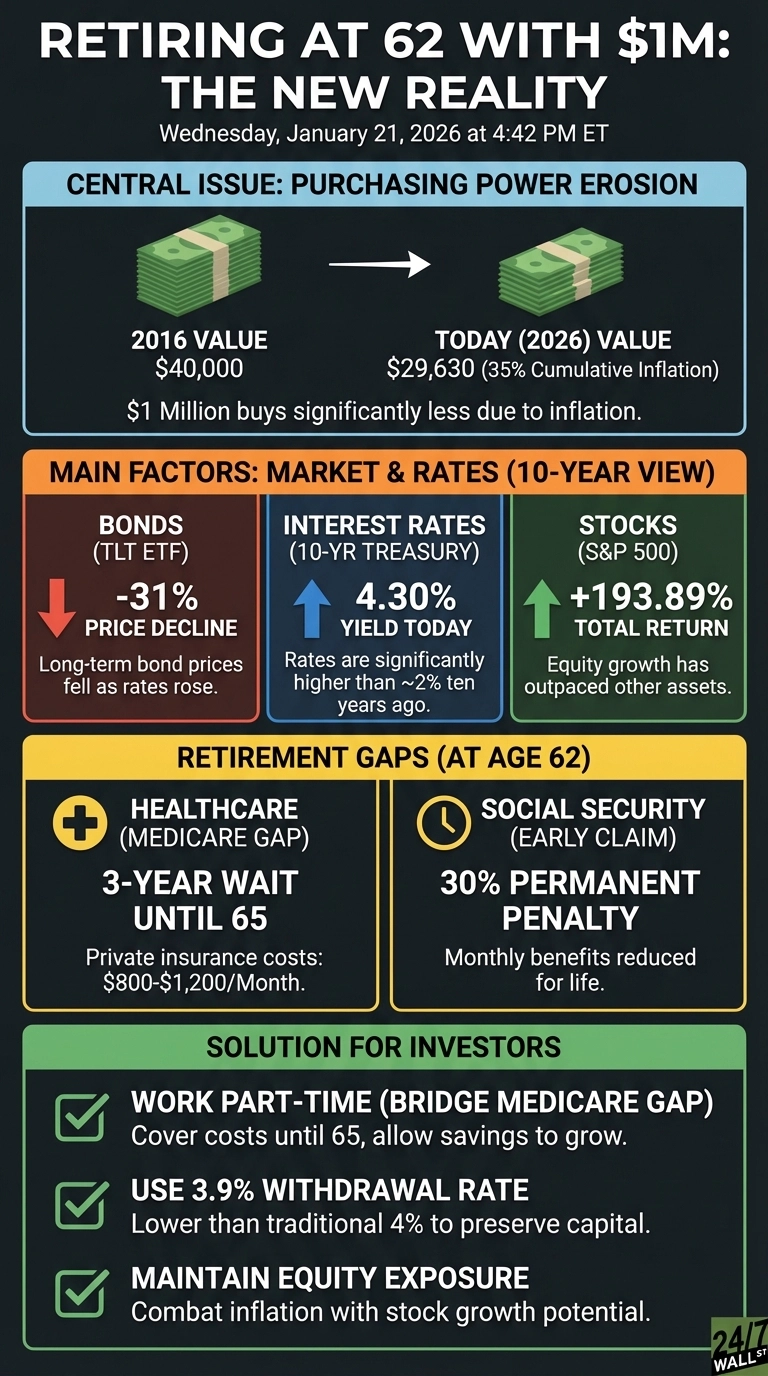

According to Bureau of Labor Statistics data, $1 in 2016 now requires $1.35 to buy the same goods in 2026—35% cumulative inflation over a decade.

For a retiree following the traditional 4% withdrawal rule, a $40,000 annual withdrawal from $1 million today has the purchasing power of just $29,630 in 2016 dollars.

Morningstar analysts now recommend a 3.9% starting withdrawal rate for today’s retirees, translating to $39,000 annually from a $1 million portfolio rather than $40,000.

The Interest Rate Reversal

Ten years ago, the 10-year Treasury yielded around 2%. Today it sits at 4.30%. While higher yields benefit income-focused retirees, the transition hurt existing bondholders.

The iShares 20+ Year Treasury Bond ETF (TLT) dropped 31% over the past decade as rates climbed. The S&P 500 gained 193.89% during the same period, highlighting the cost of being too conservative too early.

What Actually Matters Now

At 62, you’re potentially funding 30 years of retirement without Medicare or full Social Security benefits.

Healthcare represents the most immediate concern. Medicare Part B costs $202.90 monthly in 2026, but private insurance for a 62-year-old can easily run $800-$1,200 monthly depending on location and health status. That’s $9,600-$14,400 annually before deductibles or out-of-pocket costs.

Claiming Social Security at 62 triggers a permanent 30% reduction. For someone entitled to $1,000 monthly at full retirement age, early claiming means accepting $700 instead – $90,000 in forgone benefits over 25 years.

Strategic Paths Forward

Working part-time until 65 eliminates the healthcare coverage gap and allows Social Security benefits to grow 8% annually until age 67. Even modest earnings of $20,000-$30,000 yearly can substantially reduce portfolio withdrawals during critical early retirement years.

For those stopping work at 62, prioritize tax-efficient withdrawal sequencing. Tap taxable accounts first while allowing tax-deferred accounts to grow, keeping taxable income lower and potentially qualifying for Affordable Care Act subsidies.

Maintain equity exposure despite volatility concerns. A 60/40 stock/bond allocation historically supports longer retirement horizons better than conservative portfolios that can’t outpace inflation.

What to Do First

Calculate your true annual spending need, including healthcare. If it exceeds $39,000-$40,000 from your portfolio alone, consider delaying retirement or building additional income sources. Run projections assuming 3% annual inflation rather than the historical 2% average.

Avoid going too conservative with investments at 62. You likely have three decades ahead, and a portfolio that can’t grow above inflation will steadily lose purchasing power.