The 2.8% cost-of-living adjustment for Social Security in 2026 brings relief to retirees facing inflation. But for many recipients, federal income taxes claim a significant portion of that increase, reducing real purchasing power gains. Understanding Social Security taxation helps retirees plan effectively and avoid surprises at tax time.

The Provisional Income Calculation

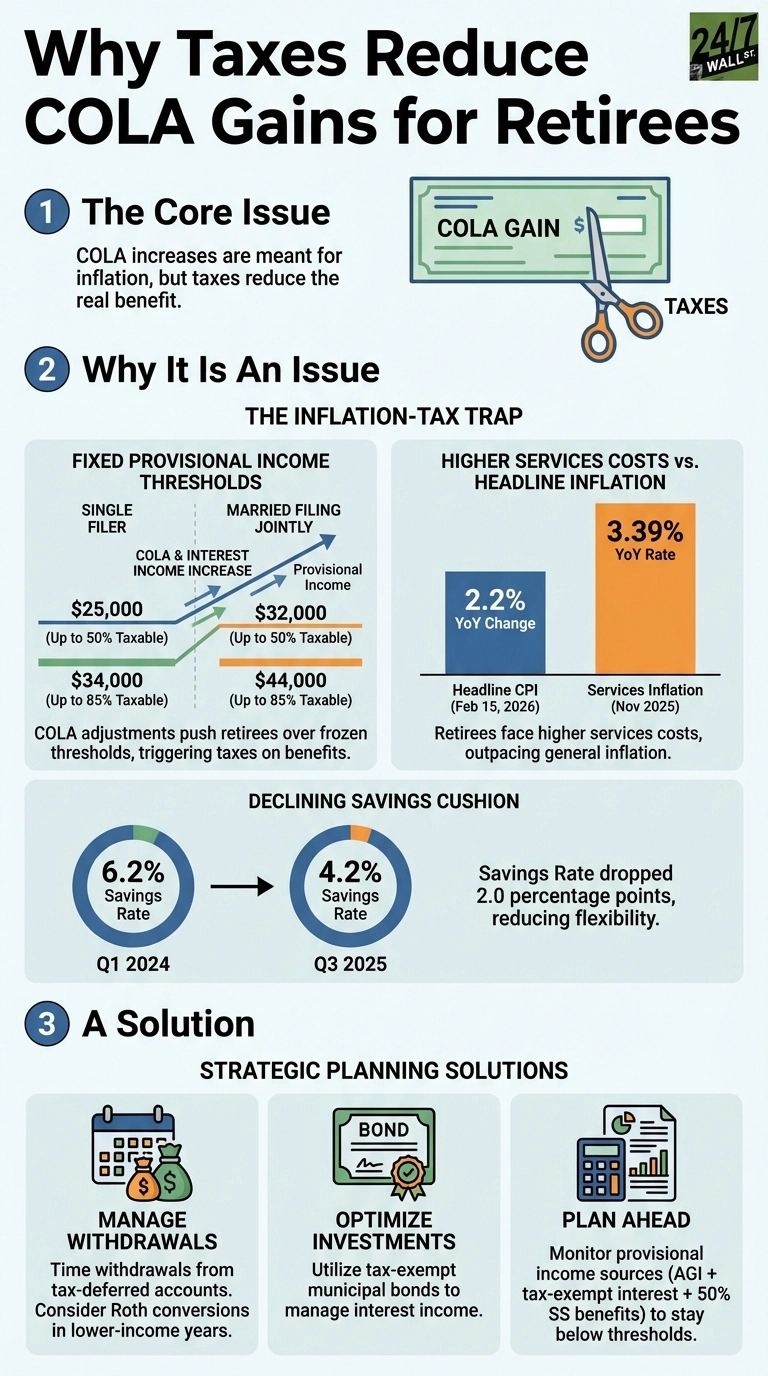

Whether your Social Security benefits become taxable depends on provisional income. This equals your adjusted gross income, plus tax-exempt interest income, plus half of your Social Security benefits. If you’re collecting $2,071 monthly in Social Security and earning interest from bonds, both sources factor into this calculation.

The thresholds triggering taxation have remained frozen since the early 1990s, creating an inflation trap for retirees. Single filers face taxation on up to 50% of benefits once provisional income exceeds $25,000, rising to 85% above $34,000. This bracket creep means more retirees fall into taxation each year as COLA adjustments push them over these outdated thresholds, even though their real purchasing power hasn’t increased.

Why COLA Increases Can Trigger Higher Taxes

The January 2026 COLA increase brought the average monthly benefit to $2,071, adding roughly $672 annually. However, this creates a taxation trap because half of every COLA dollar counts toward provisional income. Retirees who were previously just below taxation thresholds now find themselves paying federal taxes on benefits they once received tax-free, with each year’s adjustment making the next year’s situation more precarious.

Investment income compounds the challenge for retirees holding bonds in their portfolios. With Treasury yields around 4.09%, the interest generated counts fully toward provisional income calculations. Even a modest bond allocation can push retirees across taxation thresholds, creating pressure from multiple income sources simultaneously.

How This Affects Real Purchasing Power

The COLA adjustment slightly exceeded overall consumer price inflation in early 2026, but this masks a critical problem. Retirees spend disproportionately on services like healthcare and housing, where inflation has run significantly hotter than the general rate. When federal taxes claim a portion of the COLA increase, the gap between the adjustment and actual cost increases facing retirees widens considerably.

When taxes claim a portion of the COLA increase, the gap between the adjustment and actual cost increases widens. A retiree in the 85% taxation bracket effectively receives only 15% of their COLA increase as true purchasing power on that portion of benefits.

Planning Around the Thresholds

The most effective strategy involves managing other income sources before claiming Social Security. Drawing down tax-deferred retirement accounts earlier, or converting traditional IRA funds to Roth accounts in lower-income years, reduces required minimum distributions later. This keeps provisional income below thresholds when Social Security begins.

For retirees already collecting benefits, timing withdrawals from savings and managing investment income becomes critical. Spreading large withdrawals across multiple years or choosing tax-exempt municipal bonds over taxable bonds helps control provisional income. These decisions carry lasting consequences because once benefits become taxable, they typically remain so as COLA adjustments compound over time.