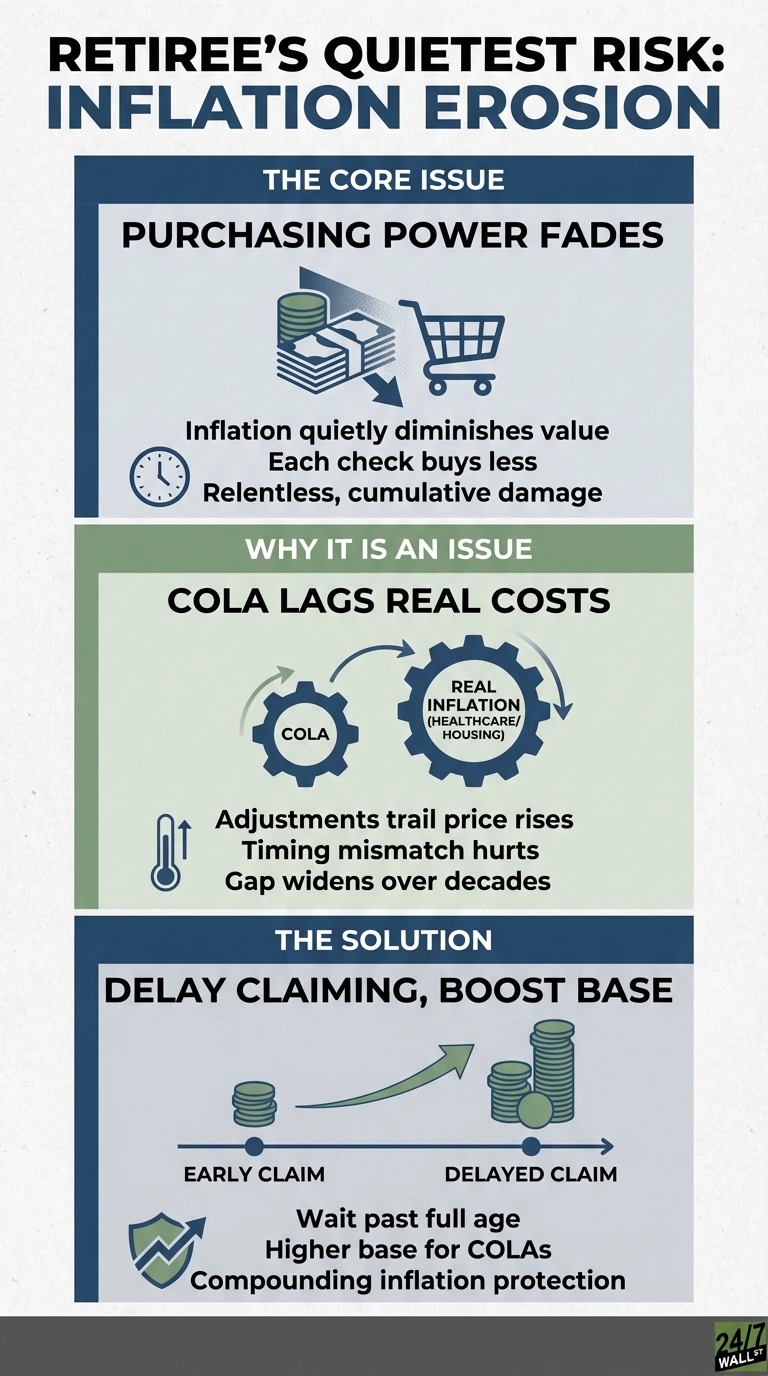

Social Security’s trust fund faces funding challenges in the coming years, triggering headlines about benefit cuts and financial doom. But for most retirees, potential policy changes aren’t the real threat. The bigger risk is quieter and more relentless: inflation steadily eroding what each monthly check can buy.

Understanding this distinction changes how you should think about retirement income and when to claim benefits. Policy debates get attention, but inflation affects every retiree, every year, for decades.

The Inflation Risk That Never Stops

Inflation’s damage accumulates slowly over a typical retirement. Social Security’s cost-of-living adjustments are designed to protect retirees from inflation, but these adjustments consistently lag behind actual price increases. When inflation spiked in recent years, retirees endured months of eroding purchasing power before their benefits caught up.

This timing mismatch hits hardest for healthcare and housing costs, which often rise faster than the general inflation rate used to calculate COLAs. The gap between initial benefits and what’s needed to maintain living standards grows over time, explaining why many retirees feel financially squeezed despite receiving annual adjustments.

How This Changes Your Claiming Decision

The inflation risk makes delaying Social Security more valuable than many retirees realize. Each year you wait past full retirement age increases your benefit, creating a higher base for all future COLA increases to compound from.

Someone who claims early receives a lower starting amount that adjusts for inflation over time. Waiting longer means those same percentage increases apply to a larger base. Over a multi-decade retirement, that difference compounds substantially as each year’s inflation adjustment builds on a larger foundation.

What Actually Deserves Your Attention

Rather than fixating on policy debates, focus on building inflation resistance into your retirement plan. Consider drawing down other retirement accounts first if you can afford to delay Social Security. The guaranteed income stream that grows with inflation becomes more valuable as you age and face higher healthcare costs.

The stock market will have volatile years, with significant gains in some periods and sharp drawdowns in others. Social Security provides something different: inflation-adjusted income you can’t outlive. In a retirement that might span three decades, that protection against rising prices deserves careful consideration in your claiming strategy.