Many retirees open their benefits statement with cautious optimism, only to find that their 2.8% cost-of-living adjustment doesn’t stretch as far as expected. The reason lies in how Social Security calculates that annual increase—and whose expenses it’s designed to protect.

The Index That Shapes Your Benefits Wasn’t Built for Retirees

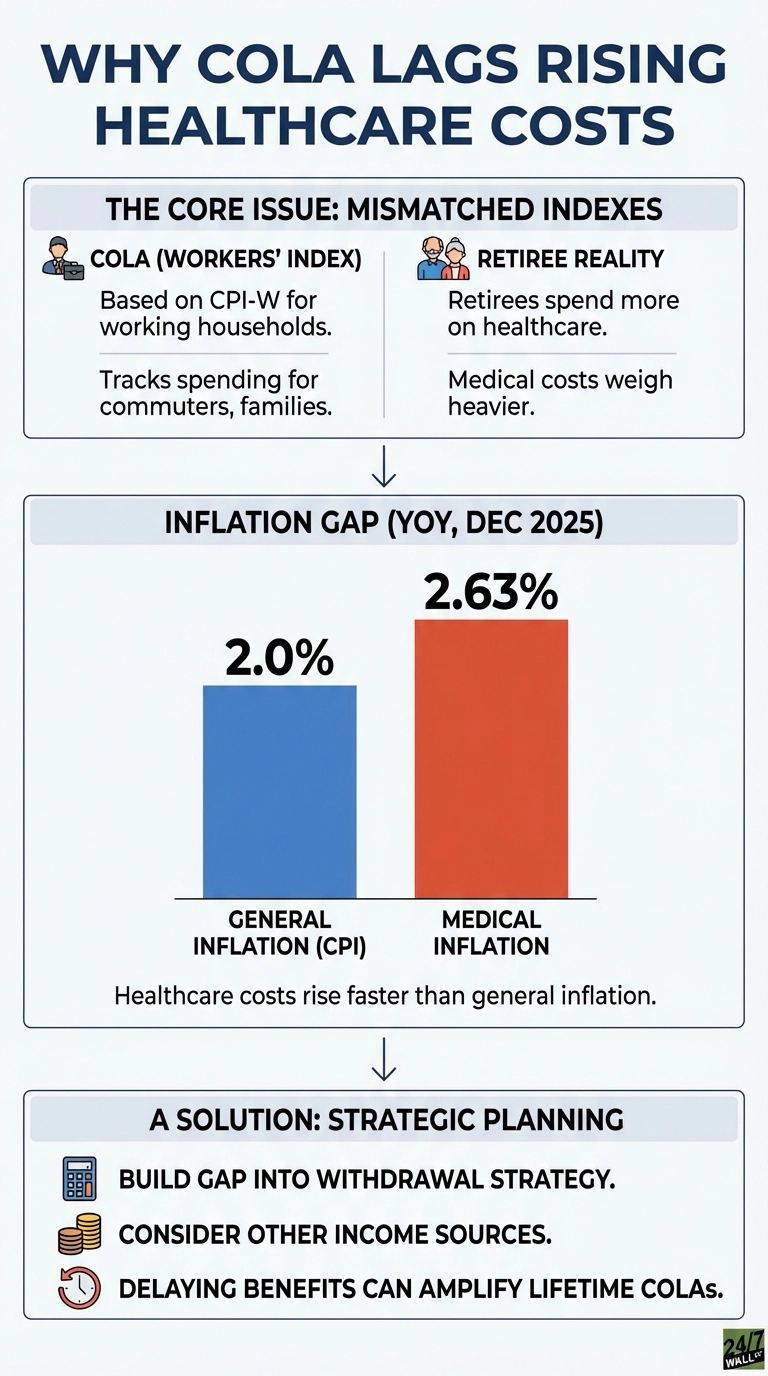

Social Security’s COLA comes from the Consumer Price Index for Urban Wage Earners and Clerical Workers (CPI-W). This index tracks spending patterns for working households—people commuting to jobs, raising families, and managing expenses that look very different from retirement. The CPI-W reflects roughly 30% of the U.S. population, and retirees aren’t the focus.

The most consequential gap shows up in medical care weighting. Working households spend relatively less on healthcare because they’re younger and often covered by employer plans. The CPI-W assigns medical expenses a smaller share than retirees actually experience. When you’re 68 and managing prescriptions, specialist visits, and supplemental insurance premiums, healthcare commands a much larger portion of your budget than the index assumes.

When Medical Inflation Runs Ahead

Medical care inflation tells a troubling story for retirees. Over the past year, healthcare costs rose faster than the general inflation rate that determines COLA adjustments—with medical expenses increasing 2.63% while broader inflation measured just 2.0%. This gap may seem small in any single year, but it compounds relentlessly when healthcare commands a significant portion of your retirement budget, eroding purchasing power in the category you can least afford to cut.

This isn’t a one-year anomaly. Healthcare costs have persistently outpaced general inflation, driven by an expanding economic footprint in the sector. The healthcare industry’s sustained growth over recent years translates directly into higher prices for the medical services, devices, and pharmaceuticals that retirees depend on most.

How This Affects Your Retirement Budget

The mismatch becomes visible when you map your actual spending against your COLA increase. If medical expenses represent 15% to 20% of your budget—common for retirees—and those costs are rising nearly a third faster than your benefit adjustment, the gap erodes purchasing power in the category you can least afford to cut.

Energy services add another layer of pressure. Utility costs have surged well beyond the COLA adjustment, hitting retirees particularly hard since they spend more time at home than working households. The CPI-W weights these expenses based on families who may be away during the day, missing how central heating and electricity costs are to retirement budgets.

What Matters Most When Planning Ahead

The COLA provides essential protection against inflation, but it’s calibrated to a spending pattern that doesn’t match yours. Recognize that your healthcare and utility costs will likely rise faster than your annual adjustment. Build that assumption into your withdrawal strategy and consider how other income sources—pensions, savings, part-time work—can absorb the difference.

If you’re deciding when to claim benefits, remember that higher lifetime COLAs apply to larger base amounts. Delaying can amplify the compounding effect of those adjustments, even if each year’s increase lags your actual cost growth. Understanding how COLA is calculated helps you plan with realistic expectations rather than hoping the adjustment will cover everything.