At 68 with strong savings, the question isn’t whether you can retire but whether you should. This crossroads involves balancing financial security, personal fulfillment, and the reality that working years are finite.

Understanding the Situation

- Age: 68 years old

- Financial Position: Strong savings accumulated

- Key Question: When to stop working

- Core Tension: Desire for retirement vs. financial certainty and purpose

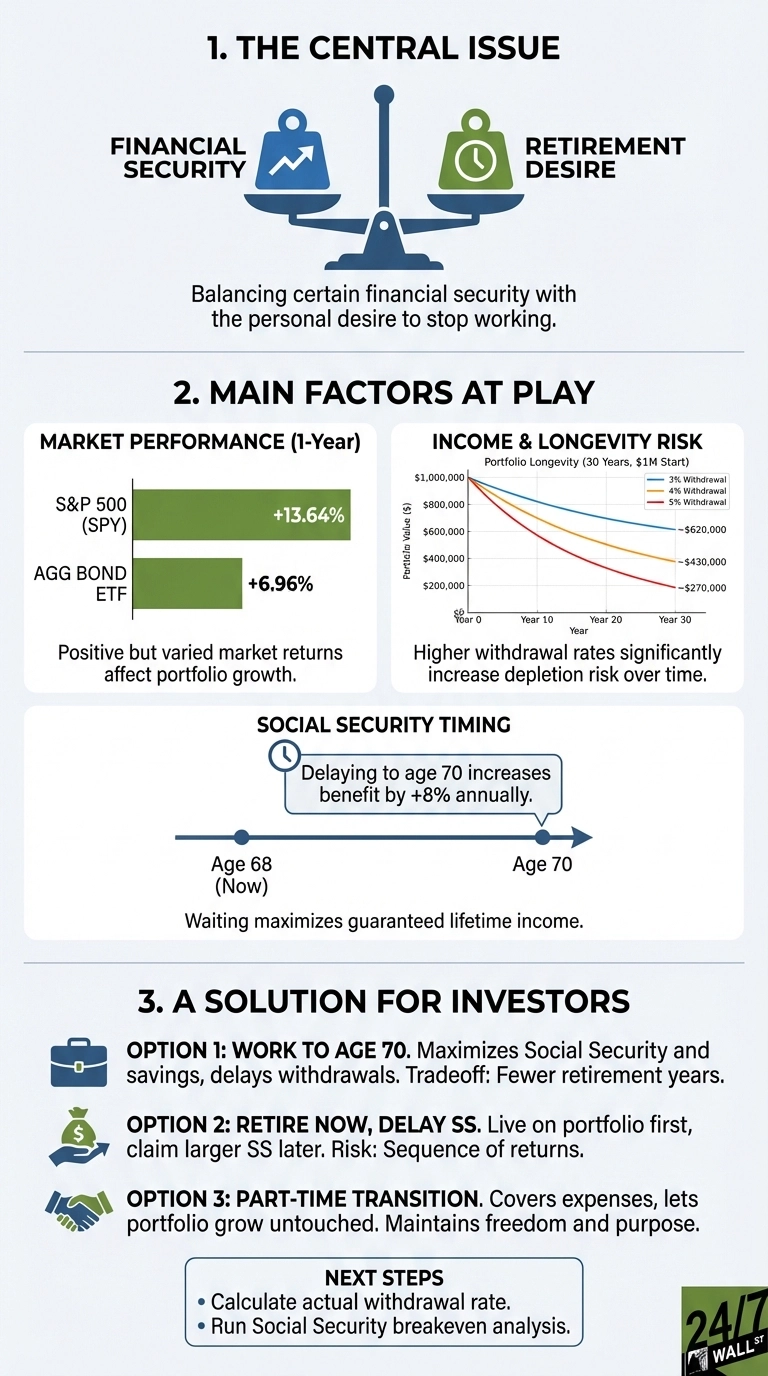

At 68, you’re past full retirement age for Social Security (67 for those born in 1960 or later). Each additional year of work increases delayed retirement credits by 8% annually until age 70, potentially adding thousands to your annual benefit. Meanwhile, your portfolio grows and you delay withdrawals that could last 20 to 30 years.

The Critical Financial Calculation

The key tension is sustainable income versus longevity risk. With strong savings, you likely have enough, but can your portfolio generate reliable income without depleting principal over a retirement spanning three decades?

A diversified portfolio following the traditional 4% withdrawal rule generates $40,000 annually from a $1 million nest egg. However, recent research suggests 3.9% may be safer for 2026 retirees given current market conditions. The S&P 500 has returned 13.64% over the past year, but bonds have struggled, with the aggregate bond market (AGG) down 2.5% over the same period due to rising rates.

Working one or two more years creates substantial buffer. If you earn $75,000 annually and save half while covering expenses with the other half, that’s $37,500 less withdrawn from savings plus continued portfolio growth. Over two years, this could add $150,000 to $200,000 in financial cushion when accounting for investment returns and avoided withdrawals.

Social Security timing matters significantly. If you haven’t claimed yet, waiting until 70 maximizes your benefit. For someone with a $2,500 monthly benefit at 67, delaying to 70 increases it to roughly $3,100, which is an extra $7,200 annually for life.

Strategic Paths Forward

Option 1: Work Two More Years to Age 70

Maximizes Social Security, adds to savings, and delays portfolio withdrawals. Best if you enjoy your work and health permits. The tradeoff is two fewer retirement years.

Option 2: Retire Now, Delay Social Security

Stop working immediately but live on portfolio withdrawals until 70, then claim maximum Social Security. This works if your savings can sustain a higher initial withdrawal rate (potentially 5% to 6%) for two years. The risk is sequence-of-returns: a market downturn in early retirement could permanently damage your plan.

Option 3: Transition to Part-Time Work

Reduce to part-time or consulting work that covers basic expenses while letting your portfolio grow untouched. This maintains income and delays full portfolio dependence while providing more freedom and maintaining purpose.

What to Do Next

Calculate your actual withdrawal rate. Divide your expected annual expenses by your total portfolio value. If it’s above 4%, you need either more savings, lower expenses, or continued income.

Run a Social Security breakeven analysis. Visit ssa.gov to see your estimated benefits at different claiming ages. If you’re in good health with longevity in your family, delaying to 70 usually wins financially.

Avoid working purely out of fear. If your numbers work and you’re staying employed only because you’re afraid to stop, you’re trading guaranteed time for theoretical security. Strong savings exist to be used.

The best choice depends on your health, your relationship with work, and whether your savings can realistically support your lifestyle for 25 to 30 years.