As you approach retirement, ensuring that your hard-earned savings and Social Security benefits are optimized is crucial for maintaining a comfortable lifestyle, as well as ensuring you also don’t run out of money in retirement (most people’s worst nightmare).

Today, let’s take a look at a common scenario in America of someone who is 65, was able to stash away $1.8 million in retirement accounts, and is now about to embark on the journey of retirement.

With $1.8 million in savings and the additional support of Social Security, this person is in a strong position to enjoy their retirement years (as long as their spending is reasonable). However, the key to financial security lies in making informed decisions about how to draw down your assets and integrate your benefits effectively.

A key question now is, how can you maximize your monthly income to make the most of your retirement?

One Approach

Maximizing your monthly income in retirement involves a strategic approach to withdrawing from your $1.8 million in savings while integrating your Social Security benefits.

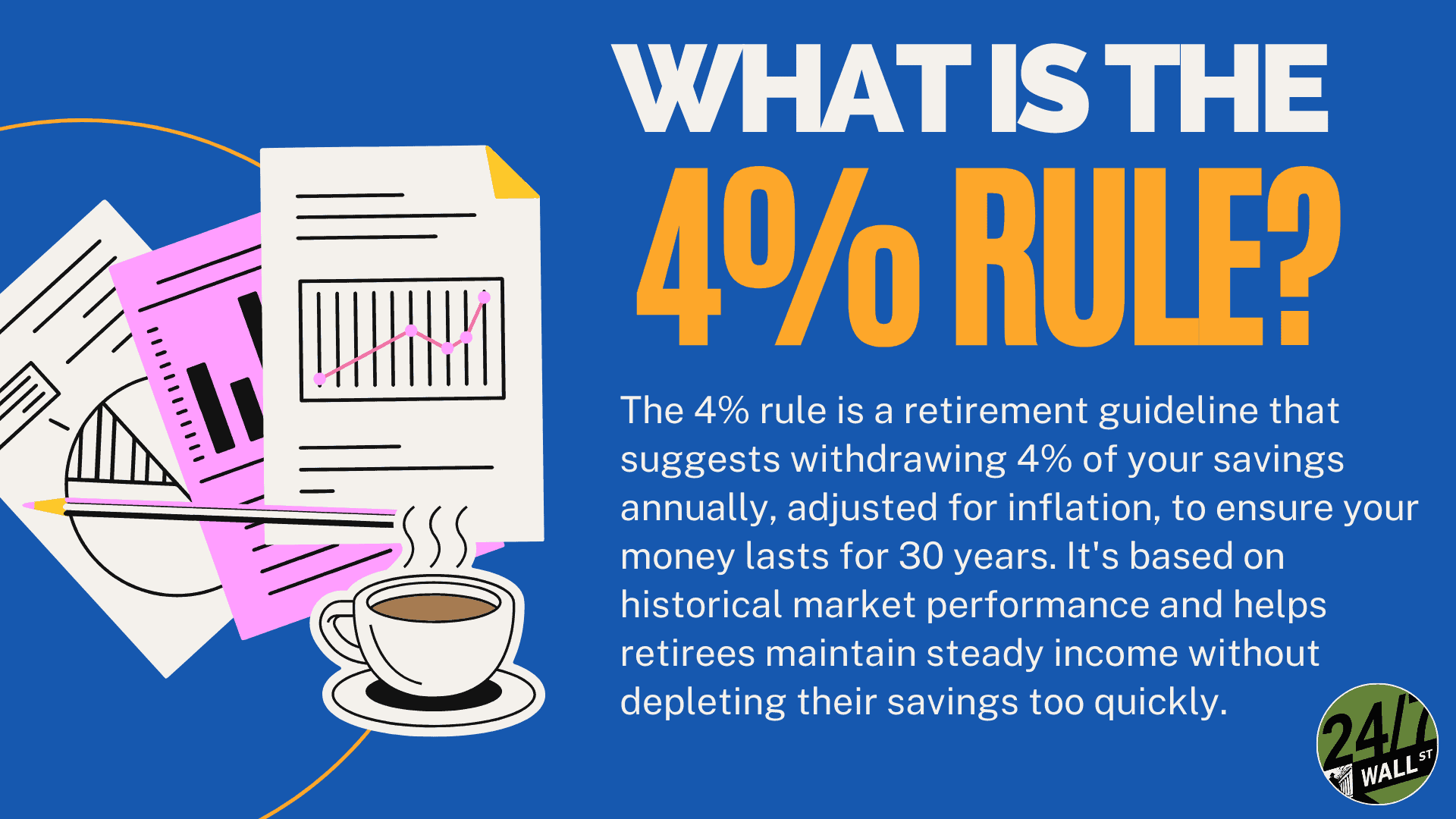

One popular strategy is to consider the “4% rule,” a commonly used guideline that suggests withdrawing 4% of your portfolio (assuming it’s diversified across stocks and bonds) annually to ensure your funds last for 30 years. With $1.8 million, this would allow for an annual withdrawal of $72,000, or $6,000 per month. However, depending on one’s risk tolerance and expected longevity, you may adjust this percentage slightly higher or lower.

It’s worth noting again that the 4% rule applies to a hypothetical portfolio invested 50% in stocks and 50% in bonds. Many people incorrectly assume that once they retire, they can move all of their portfolio to bonds/ fixed income. While this would reduce risk, it would also likely reduce one’s portfolio to continue growing at or above the rate of inflation – particularly if one lives another 20 to 30 years, which in the case of a 65 year old is quite possible.

In addition to your savings, optimizing your Social Security benefits is crucial. If you haven’t yet started receiving Social Security, delaying benefits until age 70 can significantly boost your monthly payments by up to 32%.

This delay can provide you with a larger, inflation-adjusted income stream for life, which reduces the pressure on your savings. Moreover, consider diversifying your withdrawals by using tax-advantaged accounts, such as Roth IRAs, to minimize taxes on your income.

Balancing withdrawals with Social Security, maintaining an investment strategy that preserves and grows your savings, and managing taxes effectively will help maximize your monthly income and provide financial security throughout retirement.

How an Advisor Might Be Able to Help

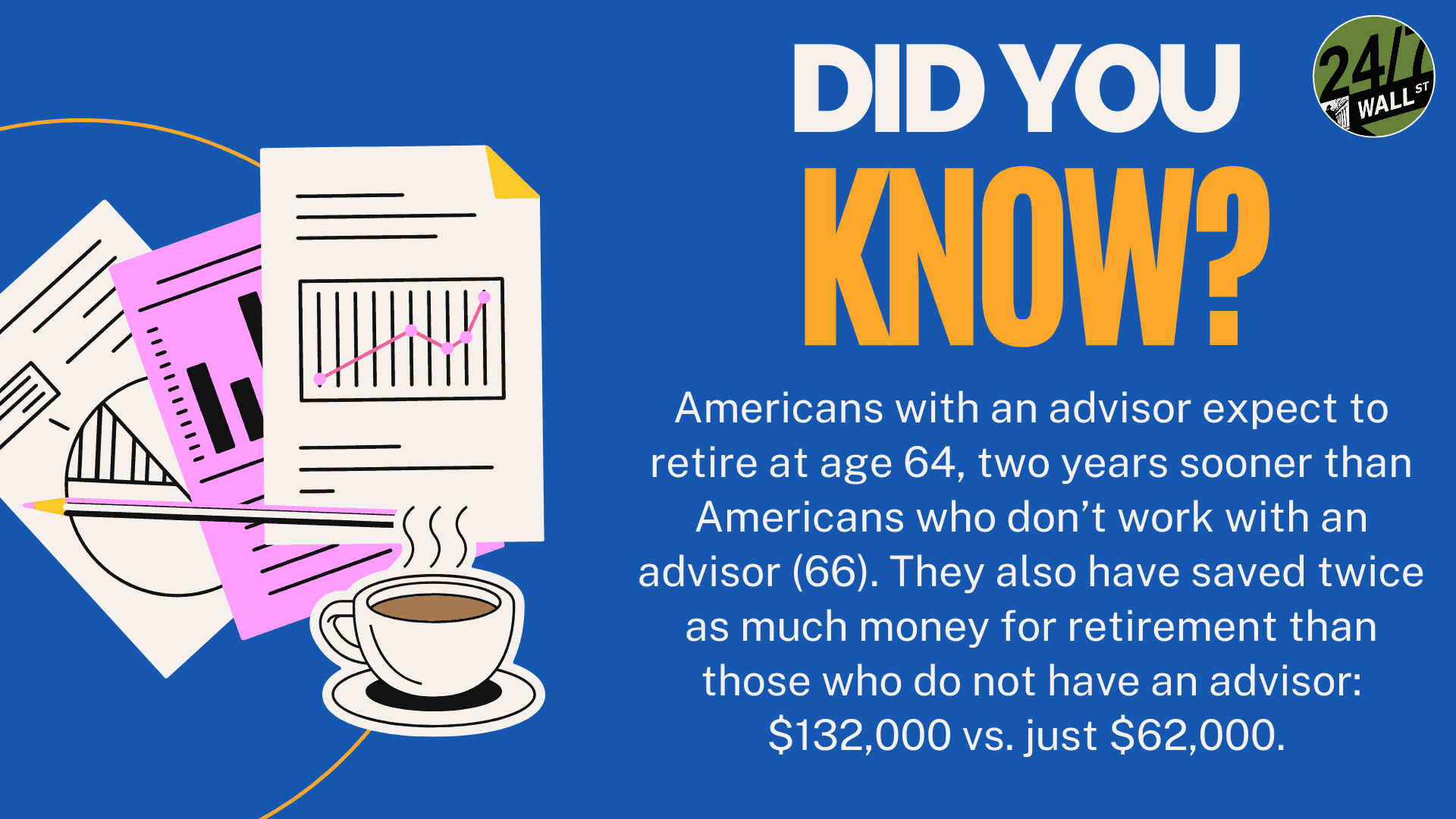

Working with a financial advisor can be invaluable when navigating the complexities of retirement planning.

A financial advisor can provide personalized guidance tailored to your unique situation, helping you create a sustainable withdrawal strategy that considers your risk tolerance, life expectancy, and tax implications.

They can also assist in optimizing your Social Security benefits, ensuring you’re making the most of this crucial income stream. Additionally, a financial advisor can help you manage and adjust your investment portfolio to align with your income needs and market conditions, providing peace of mind that your financial future is secure. By partnering with an expert, you can confidently approach retirement, knowing that your plan is designed to maximize your monthly income while protecting your long-term financial health.