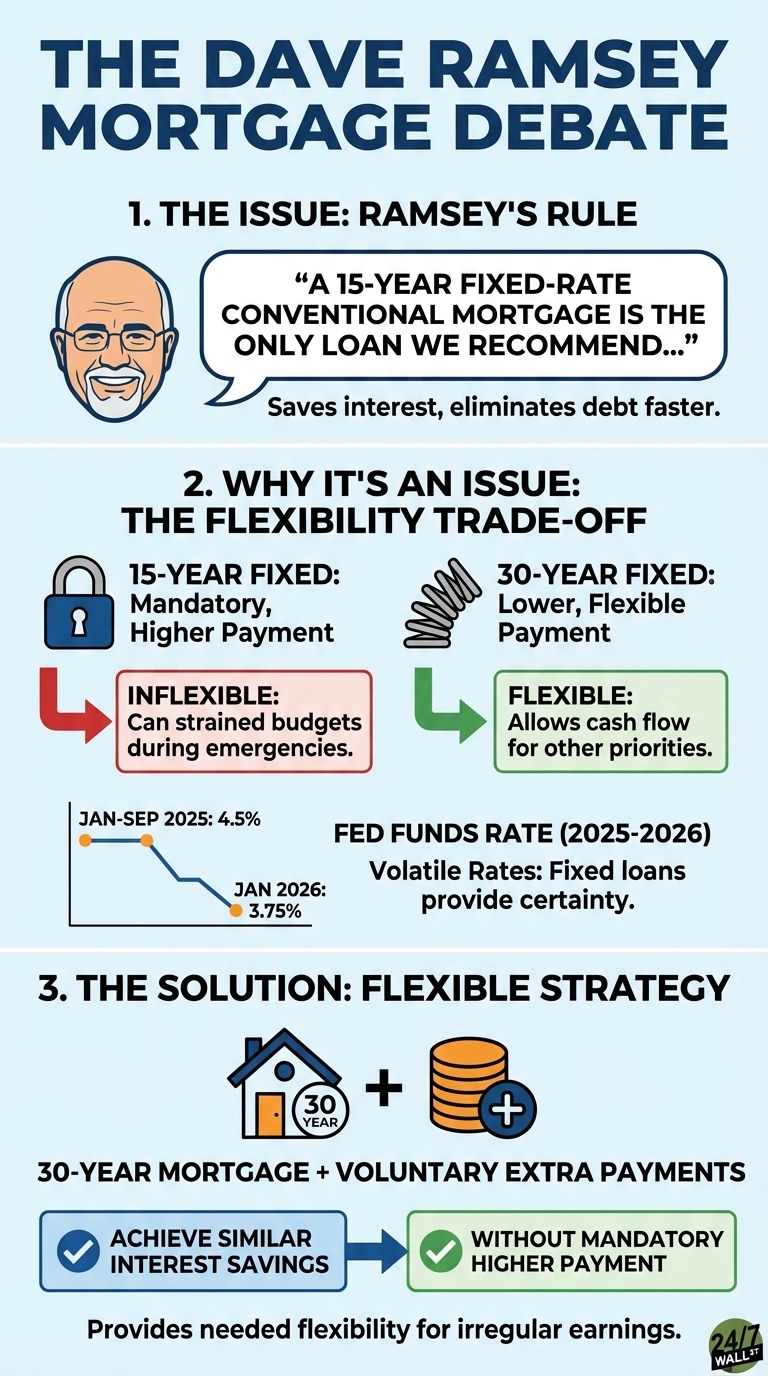

Dave Ramsey has built a personal finance empire on clear, uncompromising rules. Among his most emphatic: “A 15-year fixed-rate conventional mortgage is the only loan we recommend because it saves tens of thousands in interest and eliminates debt faster.” The statement appears across his books, radio show, and website as the singular path to homeownership without regret.

The advice resonates because it’s simple and morally framed. Adjustable-rate mortgages feel risky. Thirty-year loans stretch debt across decades. A 15-year fixed mortgage promises certainty, lower total interest, and freedom before retirement.

Where the Advice Holds Up

The mathematics behind Ramsey’s preference center on compound interest. Consider a $300,000 mortgage: the 15-year option at 5.5% costs $139,000 in total interest, while the 30-year version at 6.5% costs $178,000. That $39,000 difference comes from two factors working together – lenders offer better rates for shorter commitments, and less time means interest compounds against you for fewer years.

Recent market volatility proved the value of payment certainty. When the Federal Reserve began cutting rates in 2025, dropping from 5.50% to 3.75% by early 2026, adjustable-rate borrowers watched their payments fluctuate with each policy shift. Fixed-rate borrowers made the same payment each month regardless of whether Treasury benchmarks rose or fell, eliminating the anxiety of rate resets during uncertain times.

For disciplined savers with stable income who can afford the higher monthly payment, a 15-year mortgage builds equity rapidly and forces debt elimination during peak earning years. It works well for buyers purchasing below their means or refinancing with substantial equity.

Where the Advice Breaks Down

The “only loan” framing ignores legitimate trade-offs. Monthly payments on a 15-year mortgage run nearly double those of a 30-year loan, which can price middle-income buyers out of homeownership or force them into smaller, less suitable properties despite recent Fed cuts.

Ramsey’s rule assumes consistent income and no competing financial priorities. A household with irregular earnings, young children, or aging parents may need payment flexibility more than accelerated equity building. Paying extra principal on a 30-year mortgage when cash flow allows achieves similar interest savings without the mandatory higher payment.

Tax considerations matter too, though less than before 2018 tax law changes. For higher earners itemizing deductions, mortgage interest retains some value. Money locked into home equity earns nothing, while invested funds historically compound at rates exceeding mortgage interest over long periods.

How Retirees Should Think About This Advice

Ramsey’s 15-year rule works best as a forcing mechanism for people who struggle with financial discipline. The mandatory higher payment prevents lifestyle inflation and guarantees debt freedom. But it’s a framework, not a moral imperative.

Before committing to a 15-year mortgage, ask: Can I sustain this payment through job loss, medical emergency, or market downturn without jeopardizing retirement savings? Does my income support maxing out retirement accounts while making this payment? Would a 30-year mortgage with voluntary extra payments provide needed flexibility?

Ramsey’s mortgage rule eliminates payment shock from adjustable rates but replaces it with payment inflexibility that doesn’t fit every household’s reality.