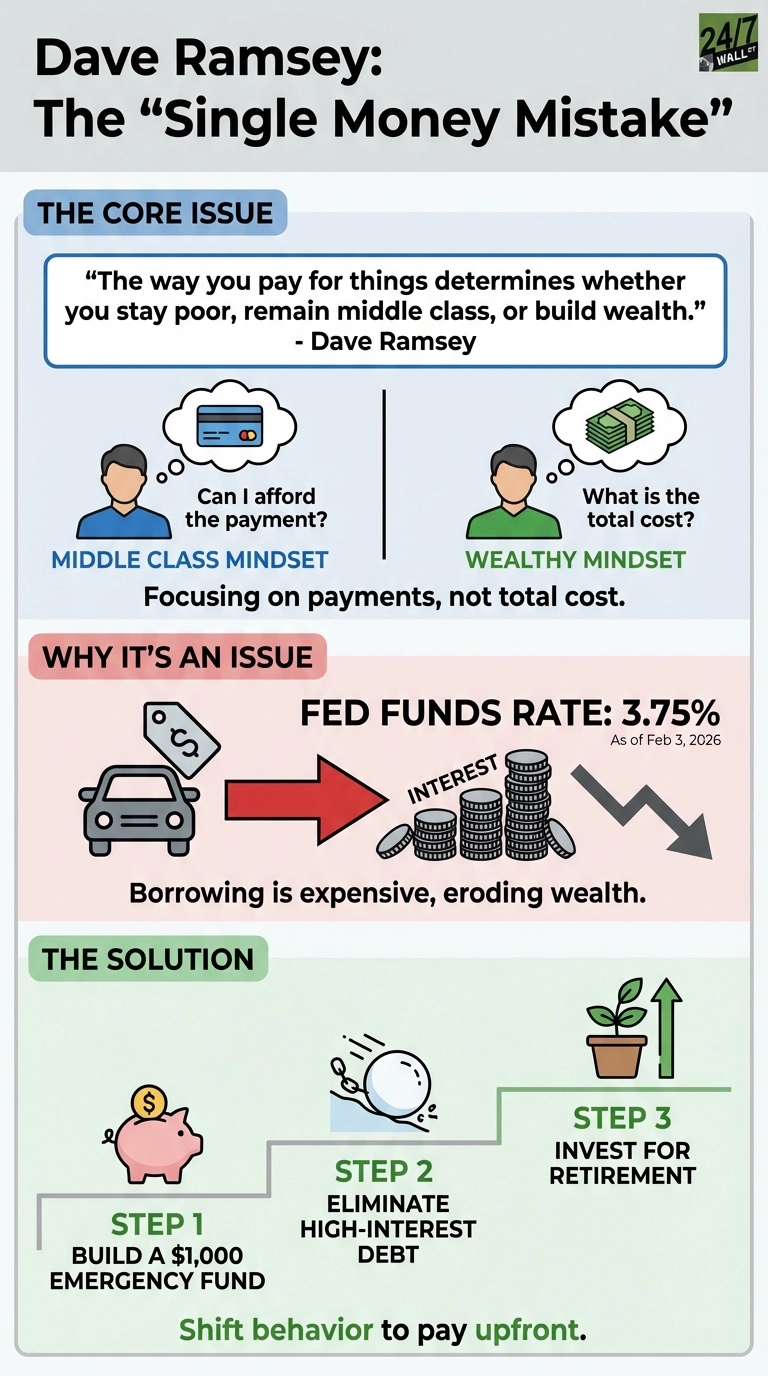

Financial expert, radio personality and author Dave Ramsey has built an empire on bold, uncompromising advice. In recent commentary, he distilled decades of teaching into a single principle: The way you pay for things determines whether you stay poor, remain middle class or build wealth. Wealthy people ask “How much?” and pay upfront to avoid interest. The middle class fixates on monthly payments and credit card rewards. The poor turn to payday lenders, pawn shops and lottery tickets.

The statement simplifies a complex problem of observable behavior. Look at how you approach a purchase, and you’ll see your financial trajectory. For readers drowning in car payments or carrying balances, the message feels uncomfortably accurate.

Where Ramsey Gets It Right

The core insight holds up. Financing everything through monthly payments locks you into a cycle of interest charges that compound over time. Borrowing costs have risen sharply since the pandemic, with the Fed’s effective federal funds rate now in the range of 3.50% to 3.75%. Credit card debt has become particularly destructive; cards typically charge APRs of 18% to 25%, which can turn small purchases into long-term drains on wealth. This makes Ramsey’s advice about avoiding interest charges more relevant than ever.

A typical car purchase illustrates the cost. Finance a $30,000 vehicle at 7% over five years, and you’ll pay roughly $4,500 in interest — money that could have built wealth instead. When this pattern repeats across major purchases throughout life, it creates the compounding effect that determines financial outcomes.

Federal Reserve data reveals the stark result of these accumulated payment decisions. The top 10% of households control 67% of total wealth, while the bottom half holds just 2.5%. This massive disparity often comes down to decades of choosing between asking “How much per month?” versus “How much does this actually cost?”

Ramsey’s advice works best for those earning stable incomes who can redirect money from interest payments into savings and investments. The behavioral shift from “Can I afford the payment?” to “Can I afford the total cost?” forces discipline that builds wealth.

Where the Advice Is Oversimplified

The framework assumes everyone has the cash flow to pay upfront. Many households face a much more difficult reality. Consumer sentiment sits at 52.9 — its lowest level since 2014 and firmly in recessionary territory — reflecting Americans’ collective, deep financial stress. Inflation ran at 2.7% year-over-year through December 2025, eroding purchasing power even as wages struggle to keep pace.

A household earning $45,000 annually faces real constraints when a reliable car costs $25,000. Paying cash means depleting emergency savings entirely, forcing families to choose between financial advice and financial security. For these households, financing becomes necessity rather than choice. The advice also overlooks strategic uses of debt, such as low-rate mortgages that preserve capital for higher-return investments, though Ramsey intentionally rejects this nuance in favor of behavioral simplicity.

The “monthly payment” framing also ignores that some middle-class families use credit responsibly, paying balances in full and capturing rewards without paying interest. The issue isn’t the payment structure itself but the habit of carrying balances and financing depreciating assets.

How to Apply Ramsey’s Advice Without Oversimplifying It

Before acting on Ramsey’s principle, ask yourself this: Do I have the cash flow to avoid financing? Or am I stretching to make payments on things I can’t afford outright? If the latter is your answer, prioritize building a $1,000 emergency fund, then eliminating high-interest debt using the debt snowball method.

If you must finance, minimize the term and interest rate. A three-year car loan at 4% is vastly different from a seven-year loan at 9%. The goal isn’t perfection but directional progress toward paying cash for more purchases over time.

Ramsey’s broader framework remains sound: Increase your income, create a budget, eliminate debt, live below your means and invest in retirement accounts. The “How much?” versus “How much per month?” distinction is a useful behavioral test, but it works best when paired with the income and savings to support it.