Wall Street can’t seem to stop selling Netflix (NASDAQ:NFLX | NFLX Price Prediction) after a 631% trough-to-peak rally from mid-2022 to mid-2025. NFLX stock has fallen by over 33% as many believe the stock was overvalued, especially after its proposed acquisition of Warner Bros. Discovery’s (NASDAQ:WBD) studio and HBO assets for $72 billion in cash.

First things first, Netflix’s total market capitalization now is $350 billion. A purchase like that would hammer Netflix’s enterprise value. The company would have to take on substantial debt, and it could dent Netflix’s operating cash flow as it would take decades to service and pay off such a large sum of money.

Second, Warner Bros isn’t doing well. It has posted losses every year since 2022, and itself carries meaningful debt. Paying that much for a struggling business is thus a big no-no for Wall Street. Netflix is also in a bidding war with Paramount Skydance for this WBD purchase.

But despite all of that, some analysts are warming up to the stock after the steep selloff and now believe it’s a buy.

Two firms recently upgraded Netflix stock: Freedom Capital Markets upgraded Netflix from Hold to Buy on January 27, 2026, with a price target of $104, and Phillip Securities upgraded Netflix from Sell to Accumulate (essentially a Buy rating) on January 26, 2026, with a price target of $100. Here’s why.

Strong Q4 results show Netflix isn’t slowing down

The company has been making a strong comeback ever since management started cracking down on password sharing and focused heavily on profitability.

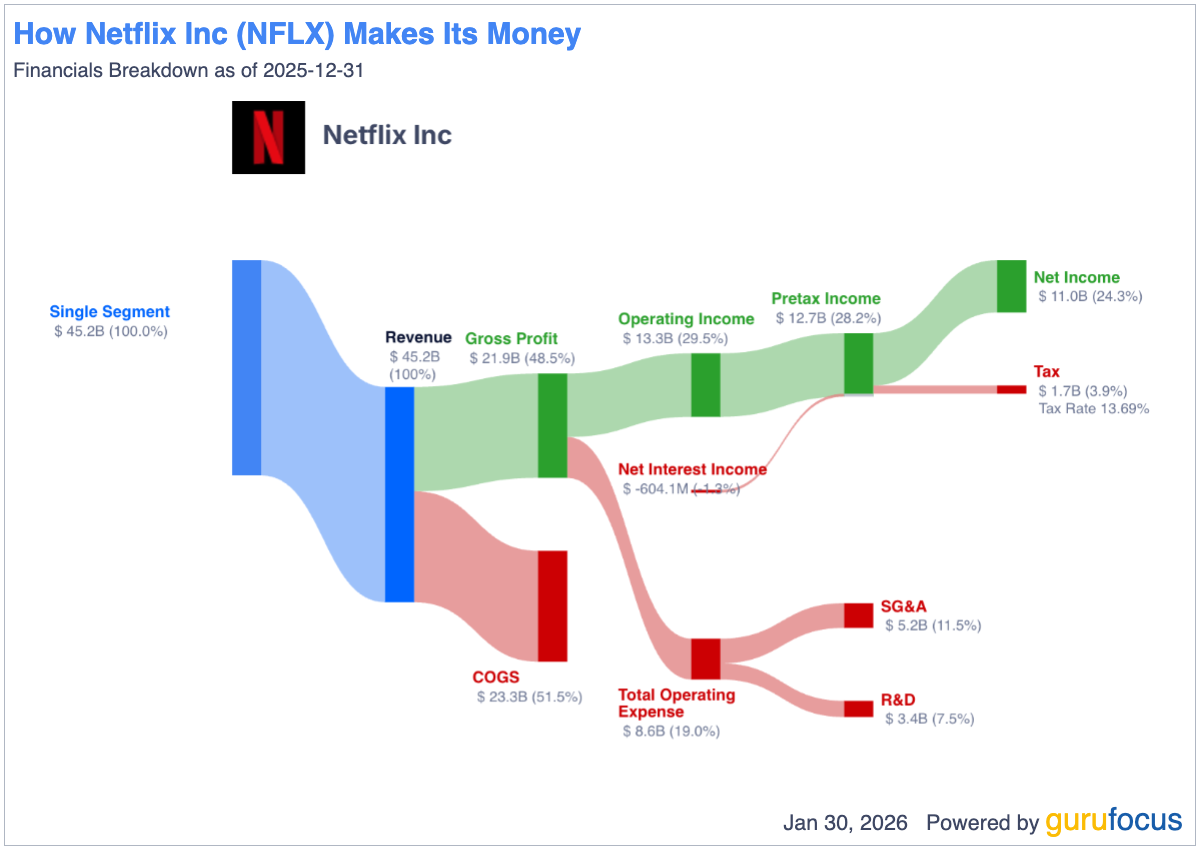

Netflix reported $12.05 billion in Q4 2025 revenue and beat analyst expectations of $11.97 billion. Sales growth was 17.6%, with 29% net income profit growth. It forecasted a doubling of its ad sales this year to $3 billion and is aggressively expanding.

The catch was that the Q1 outlook disappointed analysts. It expects 15% growth in both earnings and revenue next quarter and 13% in sales growth for the full year, 3% less than in 2025. I still think that’s very solid growth for a business so mature, and one that has shown it can outperform its own guidance consistently.

It has beaten sales expectations in 2023, 2024, and 2025. Analysts expect EPS to be $3.1 for the full year, up 23.5%. 2027 EPS is expected to be $3.8, up 22.2%, with revenue growth holding at double digits for both of those years, thanks to people keeping their subscriptions and advertising revenue remaining strong.

Is NFLX stock finally cheap?

You’re paying ~26 times forward earnings for this year, which is a very good deal for NFLX stock. It hasn’t been this cheap since late 2023. Investors were paying 52 times forward earnings last summer, so you’re paying almost half that today with only a small reduction in the company’s growth prospects.

Sure, you can argue the stock was overvalued back then, but the stock has historically traded at a premium compared to others in the business. Margins are top-notch, with an operating margin of nearly 30%. This is better than many AI software companies today.

The stock shaving a third of its value before the WBD deal even materializes is unwarranted.

Free cash flow is enough to handle much more debt

While I do believe a WBD acquisition would pressure the business, Netflix will still remain highly profitable. This company has made tremendous progress in the past 5 years. Free cash flow was -$3.14 billion in 2019 but was $9.46 billion in 2025. Similarly, operating cash flow improved from -$2.9 billion in 2019 to over $10.15 billion in 2025.

Netflix’s current $14.46 billion debt load has led to $604.1 million in net interest losses last year, so there’s plenty of room to take on more debt.

Thus, if this deal does go through, it’s not over for Netflix. The stock will recover eventually, and it’s all the merrier if Paramount Skydance wins the bidding war and is the one picking up the slack instead.

Should you buy the dip on NFLX stock?

With most analysts in the bull camp, I’d be inclined to buy the dip here. The growth is solid, and the margins can keep Netflix rising in the coming years, no matter what happens with WBD. You’re paying historically cheap premiums, and there’s little room for more disappointments as the forward earnings premium is already low.

Even if Wall Street pays 20 times forward earnings, I see 40-50% upside potential in the next two years based on the EPS growth alone. Most analysts expect that much upside in just one year, and that is more than enough to outperform the broader market.