ARM Live: Complete Coverage Of ARM’s Q2 Earnings

Quick Read

-

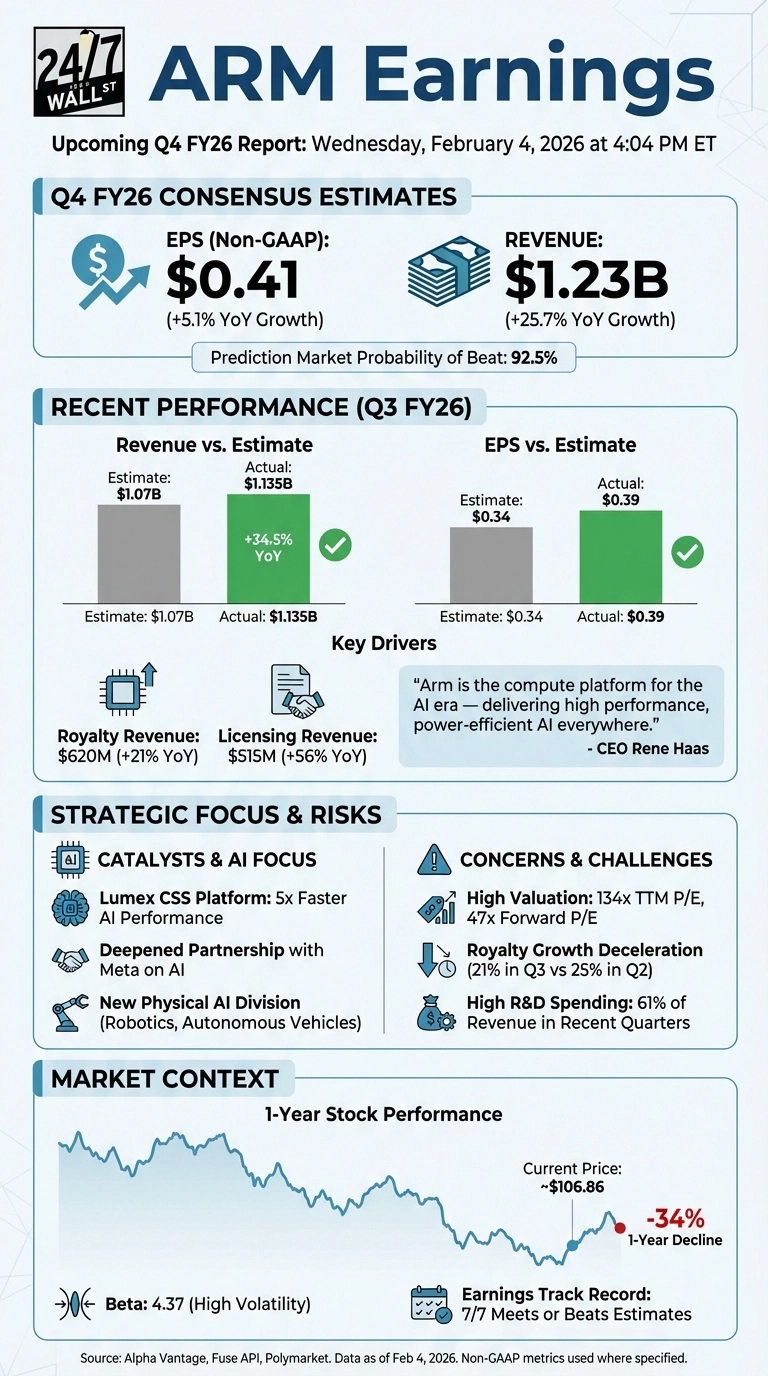

Arm Holdings (ARM) trades at 134x trailing earnings after dropping 34% over the past year.

-

Arm’s royalty revenue growth slowed to 21% from 25% the prior quarter.

-

UBS and BofA downgraded Arm over concerns about smartphone shipments and 2027-2028 royalty forecasts.

Live Updates

Arm Discusses 2027 Demand on Tonight's Conference Call

Wells Fargo tried poking at demand beyond 2026 today on Arm’s call and here’s what the company’s CFO had to say:

Joseph Quatrochi Wells Fargo Securities, LLC, Research Division

And just as a follow-up, maybe one for Jason. I know you’re not giving fiscal ’27 commentary today, but just — how do we think about the puts and takes of just royalty revenue growth and the risks that are associated with the potential like demand destruction that we’re seeing in consumer electronics potentially from memory?

Jason Child Chief Financial Officer

Yes. Yes, that’s — it’s a great question and something we spend a lot of time looking at. So in particular, I think MediaTek last night talked about something like around a 15% reduction in unit volume for next year.

And that’s pretty consistent with what we’ve heard from other smartphone and handset providers around what they think the memory supply chain constraints could provide. And so we’ve done our own kind of analysis of it. And what’s interesting is we’re hearing from [ abrades partners ] that they’re really trying to make sure that they protect the high end of the market, so the premium and flagship portion of the market, which is great for us because that’s for all of our CSS and V9 royalties are, so the highest by a significant margin.

And then on the very bottom end of the segment, that’s where most of the supply chain constraints will probably be felt. For us, that’s v8 and even older generations that are dramatically smaller royalties. So I think if you were to say, what if there’s a 20% reduction in volumes next year, for us, that would translate to probably somewhere around a 2% or 4% at worst impact on smartphone royalties. If you then project that across the whole business, it’d be a 1%, maybe 2% negative impact on total royalties. The good news is, because, as Rene mentioned, the cloud AI or infrastructure business has been continuing to grow ahead of our expectations.

It’s actually growing at a level that’s more than compensating for those kind of risks on the memory and mobile side. So I think we have a very good setup for next year, and not too concerned about at least the royalty revenue impacts that we might see from these unit volume and supply chain constraints.

Arm Provides Details on Data Center Demand During Conference Call

Here’s what Arm’s CEO had to say about data center demand on the company’s conference call:

“In cloud AI, the shift towards inference is reshaping data center design. And increasingly, that inference is agent-based. These workloads are persistent, always-on and power constrained. This is a fundamental change in how AI systems operate.

This is because agent-based AI requires coordination across many agents running continuously, and that the CPU can only do coordination. As this model scales, customers need CPU chips with higher core counts and better power efficiency to operate continuously within tight power and cost constraints. This trend directly benefits Arm. Arm-based CPU chips deliver industry-leading performance per watt, enabling customers to scale core counts and run always-on AI workloads.

We’re now seeing this trend play out in the market where Neoverse CPUs have surpassed 1 billion cores deployed, and Arm’s share amongst the top hyperscalers is expected to reach 50%. “

Arm Not a Lot of Movement on Their Call

Arm Holdings shares are still down around 8% and have seen little movement during their earnings call. We’re reviewing it and will post highlights shortly.

Earnings Call is Now Live!

Arm’s conference call is now live, we’ll post updates if anything material is said.

Simply leave this live blog open and new updates will post automatically.

ARM Conference Call Begins in 26 Minutes

Arm’s conference call is starting at 5 p.m. ET.

If you’d like to listen in you can at this link.

A Correction To Our Last Post

Arm’s guidance is for $.58, which is a slight beat versus expectations.

Wall Street is warming up to the company’s earnings, shares are now down 6.4%, which is an iimprovement from where shares originally traded after the report.

Guidance is Likely An Issue

Arm’s guidance calls EPS of $.56, which is largely inline. Revenue guidance is above consensus.

Yet, if there’s one number Wall Street is likely disappointed in its that EPS guidance. That’s driving the after-hours disappointment in shares.

Investors Not Pleased Despite Strong Earnings

Arm’s earnings look fairly strong, but investors initially sold the stock off. Arm is currently down about 8%.

That has trimmed some early losses, but is still a fairly harsh reaction.

Arm Holdings Earnings Are Out- Here Are the Key Figures

Here’s what Arm Holdings reported in Q4:

- Revenues: $1.24 billion

- EPS: $.43

As a reminder, here’s what Wall Street was expecting from Arm Holdings’ earnings:

| Metric | Q4 FY26 Estimate | Full Year FY26 Estimate |

|---|---|---|

| EPS (Non-GAAP) | $0.41 | $1.72 |

| Revenue | $1.23B | $4.85B |

Arm Shares Up 1.85% in Late Trading

It’s been a brutal day for chip stocks and stocks in the AI trade, but Arm shares are outperforming strongly. They’re up about 1.85% in late trading.

Elsewhere in the semiconductor space, NVIDIA is down 2.7%, Broadcom is down 3.8%, and AMD has dropped 16.5% after issuing guidance that disappointed Wall Street.

Snapshot of Q2 Estimates

Arm Holdings (NASDAQ: ARM | ARM Price Prediction) reports fourth-quarter fiscal 2026 earnings today after the bell at 4:04 PM ET. After a volatile year that saw shares drop 34% over the past 12 months, this report will test whether the semiconductor designer can sustain momentum from its strong third-quarter beat.

Rebuilding After a Rough Stretch

Last quarter delivered what investors needed to see. Revenue hit $1.135 billion, up 34.5% year over year, beating the $1.07 billion consensus. EPS of $0.39 topped estimates of $0.34. More importantly, it marked a sharp turnaround from the prior quarter’s miss, when EPS came in at just $0.12 against a $0.36 estimate.

CEO Rene Haas struck a confident tone, stating “Arm is the compute platform for the AI era — delivering high performance, power-efficient AI everywhere.” The company launched its Lumex CSS platform with 5x faster AI performance and deepened ties with Meta on AI infrastructure. Royalty revenue climbed 21% to $620 million, while licensing surged 56% to $515 million.

Consensus Estimates

| Metric | Q4 FY26 Estimate | Full Year FY26 Estimate |

|---|---|---|

| EPS (Non-GAAP) | $0.41 | $1.72 |

| Revenue | $1.23B | $4.85B |

Watching Valuation Against Execution

I’ll be focused on whether management can justify the premium multiple. At 134x trailing earnings, the stock trades well above the semiconductor sector average. The forward PE of 47x suggests the market expects significant earnings expansion, but recent analyst downgrades from UBS and BofA Securities cite concerns about overly optimistic royalty estimates for 2027-2028 and smartphone unit shipment declines.

The key metric to watch is whether royalty growth holds up. Last quarter’s 21% royalty increase was solid but slower than the prior quarter’s 25% gain. Any deceleration could pressure the narrative, especially with R&D spending at 61% of revenue in recent quarters. The new Physical AI division targeting robotics and autonomous vehicles needs to show traction beyond concept.

A Test of Credibility

After establishing a perfect record of meeting or beating estimates over seven consecutive quarters, ARM has built investor trust. Prediction markets assign a 92.5% probability the company will beat the $0.41 EPS estimate. If guidance disappoints or margins compress, sentiment could shift quickly given the stock’s beta of 4.37. This quarter will show whether the AI positioning translates to sustainable financial performance.

Eric Bleeker has been investing for more than 20 years. He began his career working at Microsoft before joining Motley Fool, one of the largest publishers of financial research. In his 15 years at Motley Fool Eric served as the General Manager for Fool.com and led coverage in the Technology & Telecom sector. In addition, he was a featured columnist and has hosted dozens of investing seminars attended by more than a million total investors. Eric has more than 1,000 financial bylines to his name and has been featured in The Wall Street Journal, CNBC, Fox Business, and many other leading publications. He is currently focused on artificial intelligence investing and is a CFA Charterholoder.

© 24/7 Wall St.