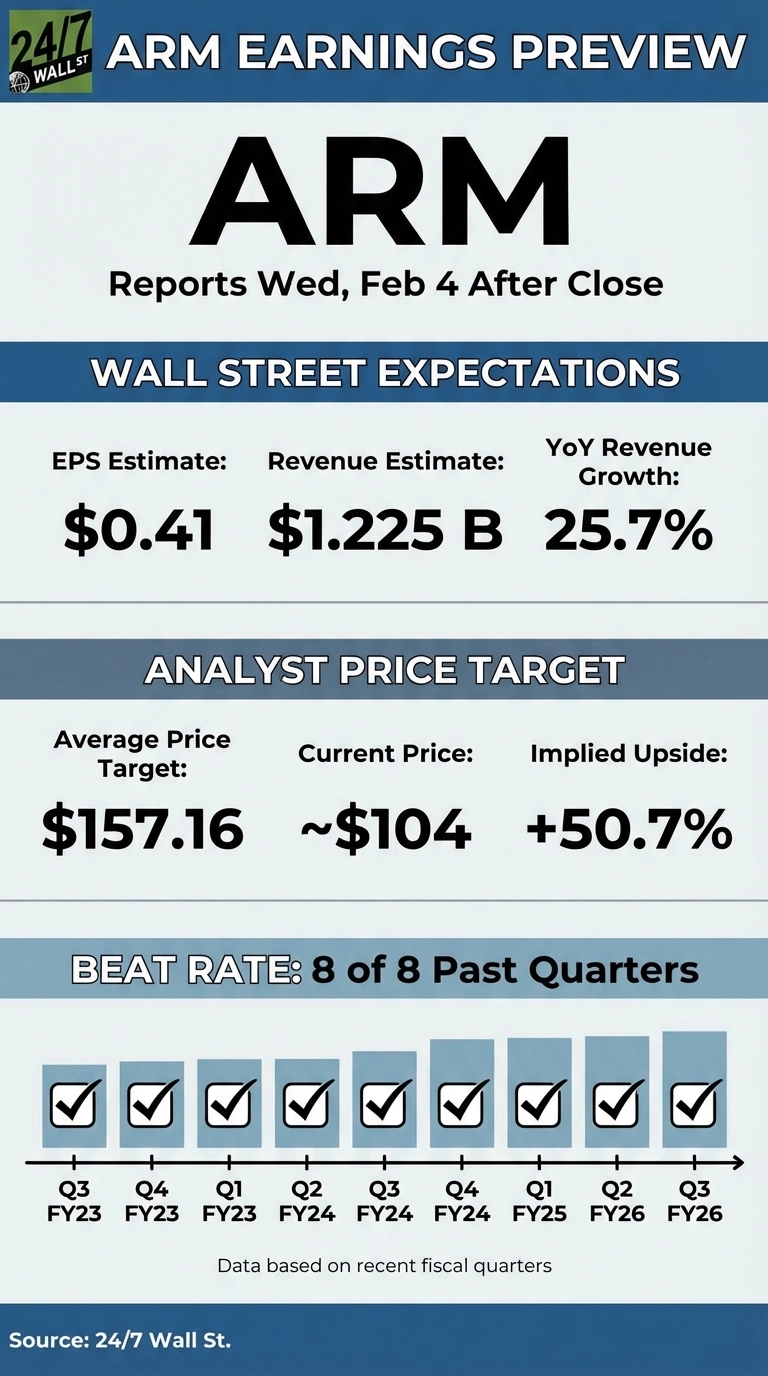

Arm Holdings reports FY2026 Q3 earnings today, Feb. 4, after market close. Wall Street expects earnings of 41 cents per share, representing a 5.1% year-over-year (YOY) increase, on revenue of $1.23 billion, representing 25.7% YOY growth. Shares have fallen more than 36% over the past year, significantly underperforming the semiconductor sector. But with an earnings beat today, the company will continue its streak of what’s currently eight consecutive quarterly beats since its IPO in 2023.

Here’s what investors should watch.

The Numbers That Matter

Wall Street expects EPS of 41 cents, up from 39 cents last quarter. Revenue consensus sits at $1.225 billion, with a guidance range of $1.175 billion to $1.275 billion provided by management last quarter.

The prediction market on Polymarket shows 89.5% probability that ARM will beat the 41 cents estimate, reflecting strong retail confidence heading into the report. Options traders are pricing in a 9.71% move in either direction following the announcement.

What Happened Last Quarter

3 key takeaways from Q3 fiscal 2026:

- Revenue hit $1.135 billion, beating estimates by 5.9% and growing 34.5% YOY. Royalty revenue climbed 21% to $620 million while licensing revenue surged 56% to $515 million.

- CEO Rene Haas highlighted “record royalties reflecting new high in demand for Arm compute platform” and positioned the company as the “compute platform for the AI era.”

- Despite beating estimates, shares fell 6.8% post-announcement, signaling investor concerns about valuation rather than operational performance.

Management’s Promise:

Last quarter, management guided to $1.225 billion in revenue, plus or minus $50 million. This report will show whether they delivered on that target.

Recent Analyst Activity Creates Conflicting Signals

Analyst activity over the past month presents a mixed picture. UBS lowered its price target from $195 to $175 and Wells Fargo cut from $195 to $160, both citing overly optimistic royalty projections. However, Susquehanna upgraded to Positive with a $150 target, calling ARM’s AI initiatives with OpenAI and Meta “company-changing” and projecting more than $1 billion in annual royalty revenue from the AI XPU program alone.

The average price target of $157.16 implies 50.7% upside from current levels near $104. ARM trades at a forward P/E of 47.17x, down significantly from a trailing P/E of 134x, suggesting the market expects significant earnings growth ahead.

What Could Move the Stock

Bull Case Triggers:

- EPS above 43 cents with raised full-year guidance would demonstrate accelerating AI monetization

- Royalty revenue exceeding $650 million would signal sustained momentum in smartphone and data center adoption

- Management commentary confirming the Meta partnership and OpenAI custom silicon projects are progressing on schedule

Bear Case Triggers:

- Revenue miss below $1.2 billion, especially weakness in licensing revenue which surged 56% last quarter

- Cautious commentary on 2026 royalty headwinds in mobile and PC markets due to memory-driven weakness

- Margin compression below 95% gross margin, which reached 97.4% in Q3

The Wild Cards:

Strategic partnerships with Apple extending beyond 2040, plus Amazon and Google custom silicon deals create long-term revenue visibility but execution risk remains. Any updates on the timing of AI XPU production could significantly impact investor sentiment.

1 Metric That Really Matters

Analysts are laser-focused on licensing revenue this quarter. Last quarter’s 56% surge to $515 million was exceptional. Sustaining licensing revenue above $500 million would validate that hyperscaler demand for custom ARM-based chips is real and durable, not a one-time spike. Anything below $475 million would raise questions about whether the AI infrastructure buildout is slowing.

With eight consecutive earnings beats dating back to FY2023 Q3, ARM has established credibility. Today’s report will test whether the company can maintain that streak while addressing valuation concerns and proving its AI partnerships translate to meaningful near-term revenue growth.