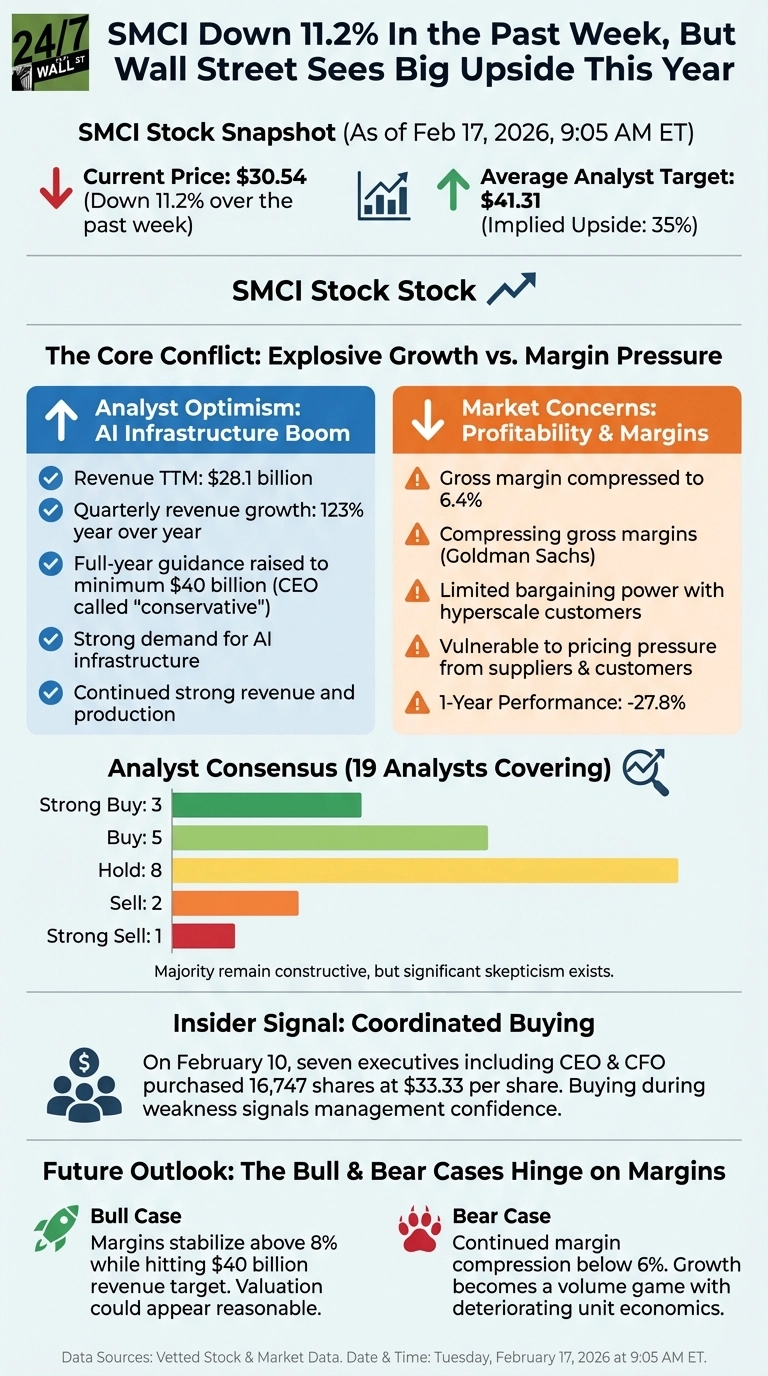

Super Micro Computer (Nasdaq: SMCI | SMCI Price Prediction) is trading at $30.54, down 11.2% over the past week. Yet Wall Street analysts see the stock climbing to an average target of $41.31, implying 35% upside from current levels. That gap widened sharply during the recent selloff, raising the question: is the market pricing in risks analysts are missing, or are analysts seeing a recovery opportunity the market hasn’t recognized yet?

The San Jose-based server and AI infrastructure specialist has delivered explosive growth. Revenue hit $28.1 billion over the trailing twelve months, with quarterly revenue growth of 123% year over year. Management raised full-year guidance to a minimum of $40 billion, which CEO Charles Liang called “conservative”. But the stock has struggled, down 46% over the past year even as demand for AI infrastructure accelerates.

Margin Pressure Triggered the Selloff

The recent decline stems from growing concerns about profitability, not demand. Goldman Sachs maintained its Sell rating, citing “compressing gross margins” and limited bargaining power with hyperscale cloud customers. Gross margin compressed to 6.4%, a sharp contraction that caught investors off guard despite record revenue. The company operates as an intermediary in the AI supply chain, assembling servers using components from NVIDIA and others, which leaves it vulnerable to pricing pressure from both suppliers and customers.

Needham cut its price target while maintaining a Buy rating, acknowledging “lower margin expectations” going forward. The market is also digesting institutional selling. Herald Investment Management reduced its stake by 4.6%, while Cibc World Market cut its position by 9%. These moves suggest some large holders are taking profits or reducing exposure despite the AI tailwinds.

Technical indicators show momentum deteriorating but not collapsing. The stock’s RSI sits at 46.72, below the neutral 50 level but well above oversold territory. That suggests selling pressure without capitulation. The stock would need to drop further to trigger classic reversal signals.

Analysts Still See the AI Infrastructure Story Intact

Wall Street’s bullish stance rests on the belief that margin pressure is temporary and manageable. Rosenblatt maintains a Buy rating with a $50 price target, citing “continued strong revenue and production” and the upcoming ramp of NVIDIA’s GB300 systems. Management is positioning the company to improve profitability through higher-margin enterprise and edge IoT customers, along with its expanded “One-Stop Shop” data center building block solutions offering.

The analyst community is split but leaning constructive. Of the 19 analysts covering the stock, 3 rate it Strong Buy and 5 rate it Buy, while 8 rate it Hold. Only 2 rate it Sell and 1 rates it Strong Sell. That distribution suggests most analysts believe the growth story outweighs margin concerns, even if conviction has weakened.

Insider activity during the recent drop adds an interesting wrinkle. On February 10, seven executives including CEO Charles Liang and CFO David Weigand purchased common stock at $33.33 per share, totaling 16,747 shares. The coordinated buying during weakness signals management confidence, though it was partially offset by routine RSU disposals on the same day.

Where Things Stand

Current Situation:

- Current Price: $30.54

- Average Analyst Target: $41.31

- Implied Upside: 35%

- Number of Analysts Covering: 19

- Recent Performance: Down 11.2% over the past week

Analyst Ratings Breakdown:

- Strong Buy: 3

- Buy: 5

- Hold: 8

- Sell: 2

- Strong Sell: 1

Comparison to S&P 500:

- SMCI YTD: +4.3%

- SMCI 1-Year: -27.8%

The data shows a divided Street. The majority of analysts remain constructive, but the large Hold contingent and handful of Sells indicate meaningful skepticism. The stock is still slightly positive year to date despite the recent drop, suggesting some resilience.

The Bull and Bear Cases Hinge on Margins

The bull case hinges on whether management can stabilize gross margins above 8% while maintaining revenue growth. If margins stabilize and the company hits its $40 billion revenue target, the current valuation at 22x trailing earnings could appear reasonable for a company growing revenue at triple-digit rates. The shift toward higher-margin enterprise customers and the expanded DCBBS offering could offset hyperscaler pricing pressure.

However, if the next quarter shows continued margin compression below 6%, the growth story risks becoming a volume game with deteriorating unit economics. The market is clearly pricing in the risk that Super Micro’s position as a systems integrator leaves it squeezed between powerful suppliers and demanding customers. Goldman Sachs’ Sell rating isn’t based on demand concerns but on structural profitability challenges.

The insider buying provides some positive signal, though the amounts were modest relative to executives’ total holdings. The key catalyst will be whether the next earnings report shows margin improvement or further deterioration. The 35% upside to analyst targets is compelling, but depends entirely on whether the margin story turns around in coming quarters.