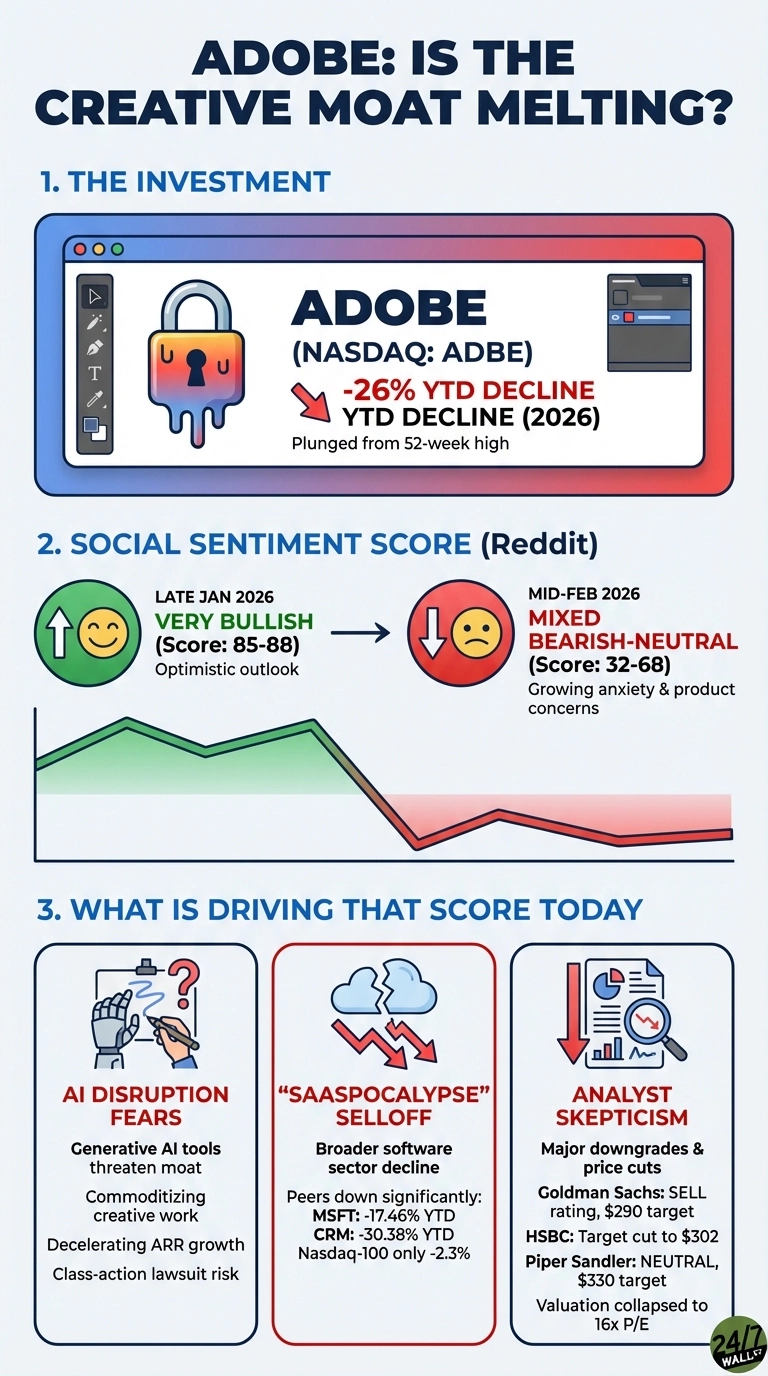

Since the start of 2026, Adobe (NASDAQ:ADBE | ADBE Price Prediction) has plunged 26% as Wall Street questions whether its creative software empire can withstand the generative AI revolution, plunging over 44% from its 52-week high as the market reprices the stock for a world where AI tools commoditize creative work that once required Adobe’s premium software suite. The selloff coincides with Reddit discussion scores sliding from very bullish (85-88) in late January to mixed bearish-neutral (32-68) by mid-February. The catalyst? Wall Street’s growing skepticism about whether Adobe’s creative software moat can survive the AI era.

The Paradox: Strong Execution, Weak Conviction

Adobe’s valuation has collapsed to a P/E of 16x (less than half its historical range) despite maintaining industry-leading operating profit margins above 36%, suggesting the market is pricing in existential risk rather than rewarding current performance. Goldman Sachs slapped a Sell rating with a $290 price target, HSBC cut its target to $302 from $388, and Piper Sandler downgraded to Neutral at $330. Wall Street is deeply divided on Adobe’s future, with Goldman Sachs issuing a rare Sell rating at $290 (implying further downside), while others, such as Piper Sandler, downgraded to Neutral at $330, reflecting uncertainty about whether Adobe can successfully monetize AI quickly enough to offset disruption to its legacy business.

Reddit Turns Skeptical on AI Strategy

Online discussions shifted from bullish optimism in late January to bearish anxiety by mid-February, with users questioning Adobe’s product quality and AI strategy. Recent posts venting product frustrations gained significant traction, with users expressing concerns about product quality and strategic direction. By late January, contrarian bets emerged: a wallstreetbets user posted a $26,000 options YOLO “because the AI narrative is stupid,” arguing Adobe is “printing money” while being unfairly punished.

The core concerns driving bearish sentiment:

- Generative AI tools from OpenAI, Midjourney, and others threaten Adobe’s Creative Cloud dominance

- Decelerating ARR growth as the company faces headwinds from AI disruption

- A class-action lawsuit alleges Adobe used pirated books to train AI models, adding legal and reputational risk

Broader Software Selloff Amplifies Adobe’s Pain

Adobe’s pain reflects a broader software sector reckoning. Enterprise software giants like Microsoft (NASDAQ:MSFT) and Salesforce (NASDAQ:CRM) have suffered even steeper declines as investors reprice the entire category for AI disruption risk, a rotation some analysts call the “SaaSpocalypse.” The Nasdaq-100 is off just 2.3% for the year, suggesting a software-specific rotation.

Investors now face a choice: trust Adobe’s $414 analyst consensus target, a 21% upside that assumes the company successfully transitions its customer base to AI-enhanced subscriptions before standalone AI tools erode its pricing power, or side with the market’s fear that autonomous AI agents will disintermediate traditional software workflows faster than Adobe can adapt.