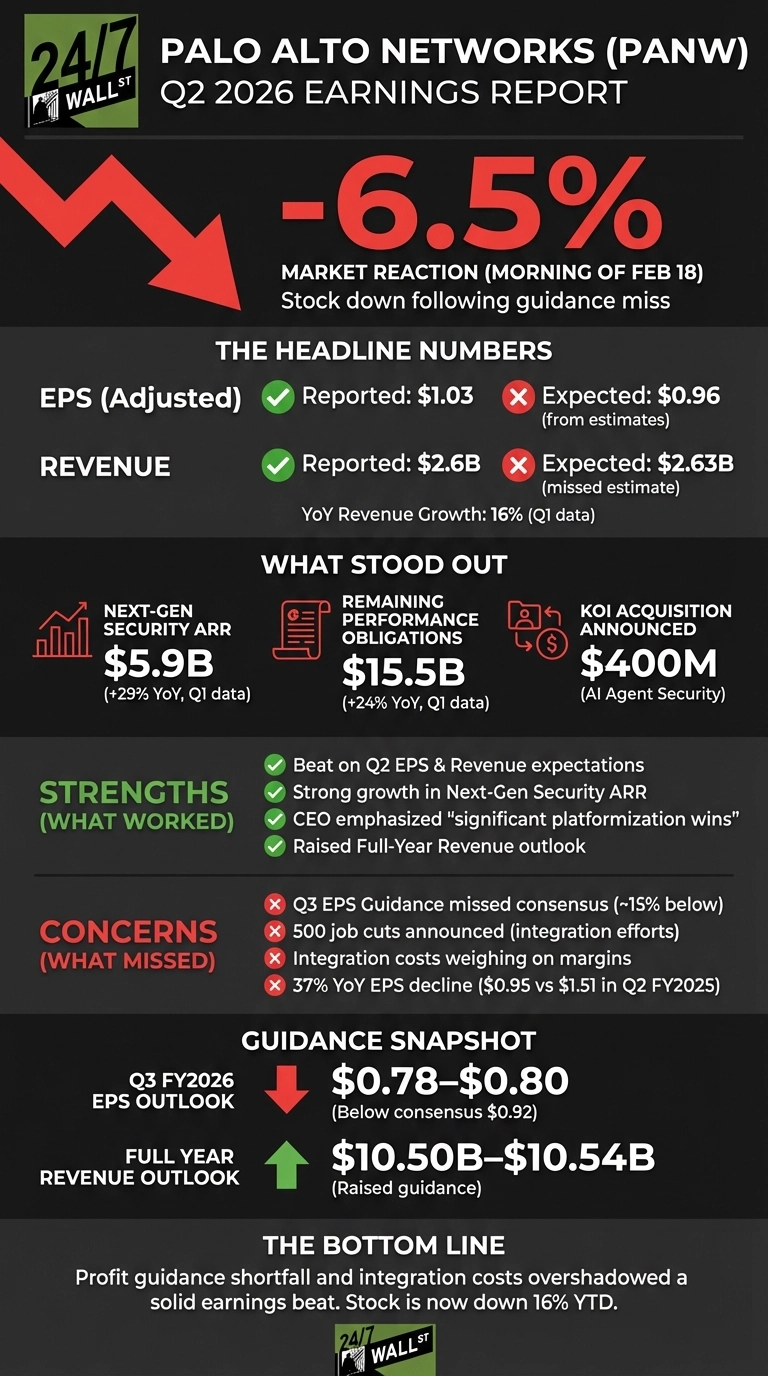

Yesterday we were watching whether Palo Alto Networks could extend its earnings beat streak and deliver the forward guidance investors expected. The company delivered a solid quarter after the bell Tuesday, but this morning shares are down 6.5% as weak profit guidance overshadowed otherwise strong results.

The Guidance Gap That Drove the Selloff

Palo Alto Networks reported Q2 fiscal 2026 results after the close on February 17. The Q2 FY2026 analyst EPS estimate stood at $0.96 per share on revenue of approximately $2.63 billion, per the most recent available estimates. In Q1 FY2026, the company had guided Q2 revenue to $2.57–$2.59 billion and EPS of $0.93–$0.95. Next-Generation Security ARR reached $5.9 billion in Q1, up 29% year over year, with remaining performance obligations of $15.5 billion.

The selloff this morning appears driven by the Q3 profit outlook, which came in below analyst expectations. Revenue guidance for the full year had previously been set at $10.50–$10.54 billion as of the Q1 report. Investors focused squarely on the profit shortfall signaled in management’s forward commentary.

Integration Costs and Strategic Bets Weigh on Margins

The earnings pressure appears tied to integration costs from recent acquisitions. 500 job cuts were announced as part of ongoing integration efforts. On Tuesday, the company also revealed it is acquiring Israeli cybersecurity startup Koi for $400 million to bolster AI agent security capabilities.

CEO Nikesh Arora emphasized that “customers are keen to both modernize and normalize their cybersecurity stack, aligning them to our approach,” pointing to continued strength in platformization deals. Yet the market appears skeptical that near-term execution can keep pace with the company’s aggressive M&A strategy.

What’s Next for PANW

The stock has now fallen 16% year to date and 26% over the past year, reflecting growing investor concern about margin pressure in a highly competitive cybersecurity landscape. We’ll be watching whether management can demonstrate integration progress and margin improvement when the company reports Q3 results.