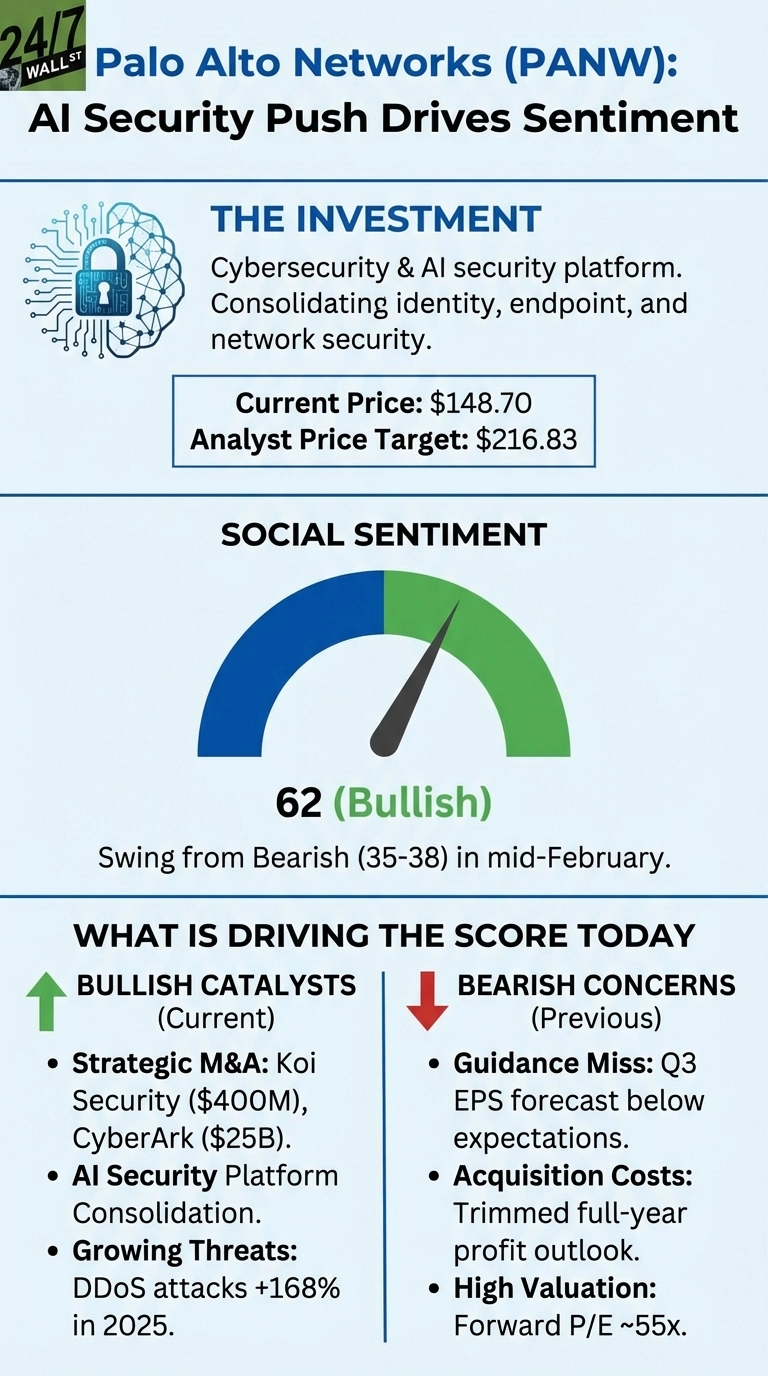

One of the world’s foremost cybersecurity names, Palo Alto Networks (NASDAQ:PANW | PANW Price Prediction) is down 21% year-to-date and 24% over the past year, sitting at $144 against a 52-week high of $223.61. Reddit sentiment swung from a bearish 35-38 during a nine-day stretch in mid-February to a bullish 62 by February 22, coinciding with a flurry of strategic announcements that changed the narrative.

What Pushed Sentiment to 35

The bearish stretch tracked Palo Alto Networks’ Q2 FY2026 earnings on February 17, 2026. Headline numbers were solid: revenue grew 15% year-over-year to $2.59 billion, adjusted EPS of $1.03 beat expectations, and next-generation security ARR jumped 33% to $6.33 billion. But management trimmed its full-year profit outlook due to acquisition costs, and Q3 EPS guidance missed expectations, sending shares down 5-7% in after-hours trading.

A thread on r/stocks titled “Does the SaaS-pocalypse scare have any legs?” gained 78 upvotes and 88 comments. The original poster wrote: “Seeing Palo Alto Network’s prints today (lowering EPS guidance), it kinda of hit me SaaS business may also need to increase spend…”

Does the SaaS-pocalypse scare have any legs?

by u/[OP] in stocks

The bear case rests on three points: the $25 billion CyberArk deal added near-term EPS dilution; integrating CyberArk, Chronosphere, and Koi simultaneously creates real execution risk; and a forward P/E around 55x leaves little room for guidance misses.

Why r/investing Turned Bullish

Sentiment flipped as investors digested what the acquisition spree actually builds. Palo Alto closed the $25 billion CyberArk deal on February 11, 2026, adding identity security to its platform. On February 17, it announced a $400 million acquisition of Koi Security, a one-year-old Israeli startup targeting agentic AI endpoint protection: autonomous AI agents that can download malicious files or compromise software supply chains without human involvement. Discussion on r/investing reflected this shift, with users in threads such as “Which cybersecurity company stands to benefit most in the age of AI and Quantum?” noting that platform consolidation plays like Palo Alto stand to capture disproportionate AI security spend, with one commenter writing: “The companies that can bundle identity, endpoint, and network into one pane of glass are going to win the next decade of enterprise security.”

Which cybersecurity company stands to benefit most in the age of AI and Quantum?

by u/[OP] in investing

Analyst consensus fair value sits at $240.06, with 39 analysts rating the stock a Buy and a 12-month price target of $216.83. CEO Nikesh Arora has called AI “more of an opportunity than a threat for cybersecurity vendors”, and network-layer DDoS attacks rose 168% in 2025, expanding the market for exactly what Palo Alto sells.

The near-term question is whether integration execution and margin recovery can keep pace with a valuation that still demands significant growth. The ultimate test, at least for now, will be Q3 FY2026 results. If free cash flow holds and NGS ARR growth stays above 25%, the gap between the current $148.70 price and the $216.83 analyst consensus target becomes harder to ignore.