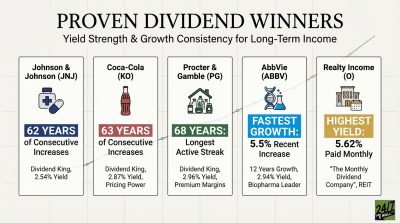

Realty Income (NYSE: O | O Price Prediction) reports its Q4 2025 and full-year results today after the market closes. The central question is straightforward: did the company close out 2025 within its own raised guidance range?

A Strong Setup Heading Into the Final Quarter

Last quarter, Realty Income delivered revenue of $1.39 billion while AFFO came in at $1.08 per share. GAAP EPS missed expectations, but that metric is largely irrelevant for net lease REITs. AFFO (adjusted funds from operations) is what drives dividend sustainability and valuation here.

Management raised full-year guidance mid-cycle, lifting the AFFO per share range to $4.25 to $4.27 and increasing investment volume guidance from $5.0 billion to approximately $5.5 billion. Through Q3, year-to-date investment volume had already surpassed $3.9 billion, meaning Q4 needed to contribute roughly $1.6 billion to hit the target.

The rate backdrop has also improved. The Fed cut rates twice since December 2025, bringing the federal funds rate to 3.75%, down 75 basis points over the past year. The 10-year Treasury yield sits at 4.08%, down 50 basis points from its May 2025 peak of 4.58%. That shift has been a meaningful tailwind for REIT valuations and borrowing costs.

Consensus Estimates

| Metric | Q4 2025 | FY 2025 |

|---|---|---|

| AFFO per Share | ~$1.05-$1.08 (implied) | $4.25-$4.27 (company guidance) |

| Revenue | $1.392 B | $5.43B |

AFFO Delivery and 2026 Guidance Will Drive the Reaction

The print itself matters less than what comes after it. I’ll be watching three things closely tonight.

First, whether full-year AFFO lands within the $4.25 to $4.27 guidance range. Management raised that range after Q3, and missing it now would raise questions about forecasting credibility. Hitting the high end would signal operational discipline.

Second, 2026 AFFO guidance. This is the number that will move the stock. Investors have bid shares up 16.1% year-to-date, far outpacing the broader market. That re-rating reflects optimism about a lower-rate environment supporting growth. Management needs to validate that optimism with a credible forward AFFO range.

Third, the investment pipeline. Europe represented 72% of Q3 investment volume at an 8.0% yield, compared to 7.0% in the U.S., where competition from firms like Blackstone, BlackRock, and Starwood has intensified. You should watch whether Q4 investment volume confirms the $5.5 billion annual target and whether European deal flow remained the primary driver.

Occupancy and rent recapture rates are secondary but worth noting. Q3 occupancy held at 98.7% with a rent recapture rate of 103.5%, above the historical average of roughly 101%. Any deterioration there would be a yellow flag for portfolio health. Also worth monitoring: progress on the recently launched perpetual life fund, which CEO Sumit Roy described as expected to provide additional capital to support growth objectives and enhance liquidity.

A Chance to Lock In the Re-Rating

Realty Income has spent much of the past year rebuilding investor confidence as rates peaked and then retreated. The stock’s strong run into tonight’s report reflects that progress. Now management has to confirm it with numbers. If AFFO lands at or above guidance and 2026 targets look credible, the narrative shifts from recovery to sustained growth. That would be a meaningful moment for a company that calls itself the Monthly Dividend Company.