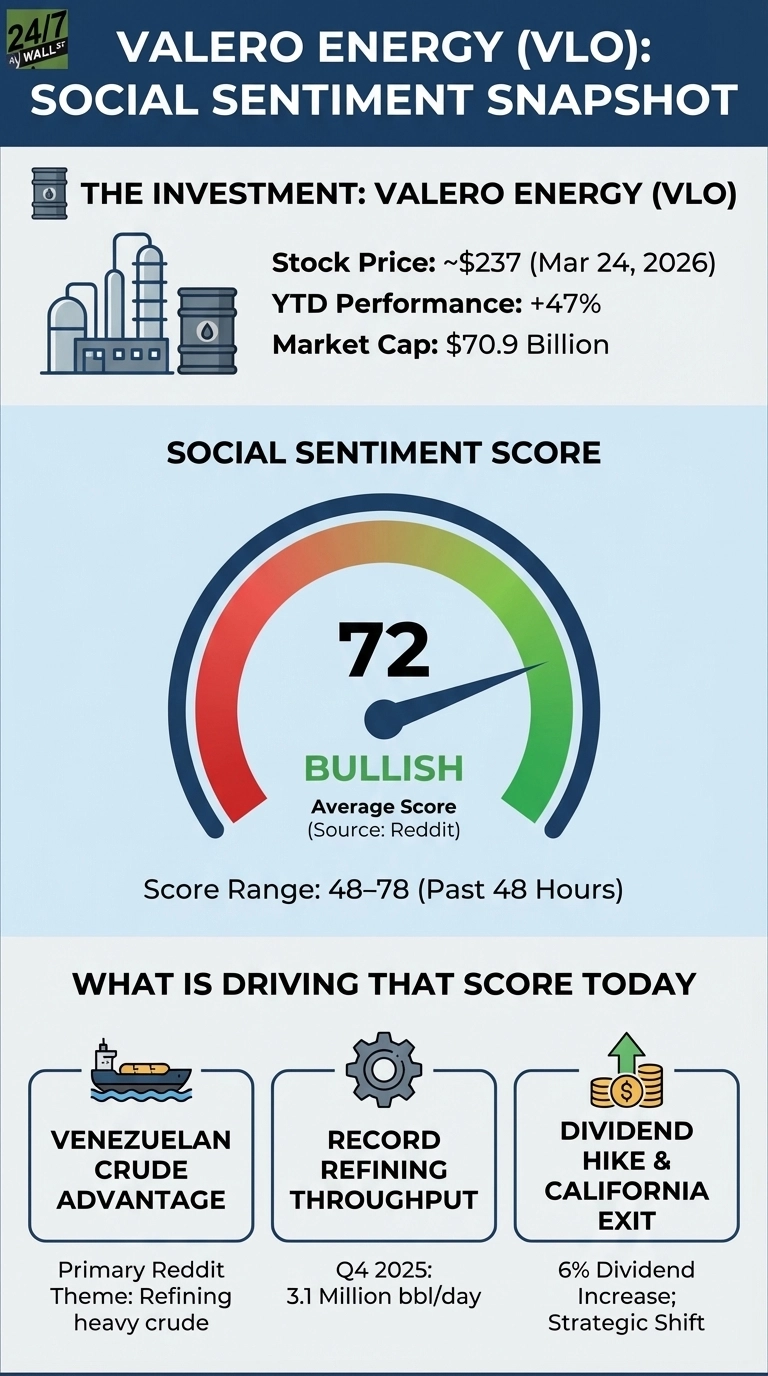

Reddit’s r/wallstreetbets has been building a bull case on Valero Energy (NYSE:VLO | VLO Price Prediction) since the company posted record refining throughput, hiked its dividend, and announced a full exit from California, with shares up about 47% year to date and trading near $239. The catalyst: record refining throughput of 3.1 million barrels per day in Q4 2025, a 6% dividend hike to $1.20 per quarter, and a strategic California exit reshaping how investors think about the business.

The good news is that the Q4 2025 numbers were hard to ignore, as Valero posted adjusted EPS of $3.82 against a $3.27 estimate, with refining segment operating income surging to $1.69 billion from $437 million a year earlier. Behind those numbers: 98% throughput capacity utilization across the full year 2025, a figure CFO Homer Bhullar called out explicitly on the earnings call. For the full year, Valero returned $4 billion to shareholders and reduced its share count by 42% since 2014.

What the Reddit Bulls Are Actually Arguing

Over the past 48 hours, sentiment on Reddit has been predominantly bullish, with scores ranging from 76 to 78 across four of five tracked periods, and an average sentiment score of 72 out of 100. The primary thread, posted by u/StoopSign on r/wallstreetbets, frames the bull case around geopolitical feedstock advantages rather than the earnings beat.

Valero Energy (VLO) is a good oil stock because they refine PDVSA Venezuelan Crude-Benefitted from closure of of the Strait Of Hormuz

by u/StoopSign in wallstreetbets

The author, a former Venezuela journalist, writes: “Valero has performed well during the Maduro regime and after the shift towards the Rodriguez administration and its efforts in liberalizing the oil sector. Equally or potentially more importantly, the tensions involving the closure of the Strait of Hormuz have benefited Valero’s stock price.” The post has accumulated 132 upvotes and 62 comments. The thesis has merit: Valero’s Gulf Coast configuration is purpose-built for heavy crude, and the company has historically been the largest U.S. purchaser of Venezuelan heavy crude, processing as much as 240,000 barrels per day before capacity expansions at Port Arthur raised that ceiling further.

Three reasons Reddit bulls are leaning in:

- Valero’s coker infrastructure gives it a structural cost advantage in processing discounted Venezuelan and Canadian heavy crude, with heavy Canadian grades trading around $11 to $11.50 under Brent heading into 2026

- Valero has taken the $1.1 billion Benicia impairment charge, and the California exit is expected to save roughly $150 million annually in sustaining capital

- Valero’s capital allocation framework targets a minimum 40% to 50% payout ratio with share repurchases filling the gap, a decade-long program generating mid-teens returns on buybacks per management

The Real 2026 Risk Is Margins

On the one hand, the California exit is largely priced in, but the more pressing question is whether refining margins can hold as WTI crude has jumped from around $76 in early 2025 to roughly $92 more recently. Tighter crack spreads pose a structural threat to earnings power, and the forward P/E of 31x sits above the industry average of 16x, implying the market is pricing in continued execution at near-record utilization. COO Gary Simmons offered a constructive read on the call: “demand is outpacing additional supply” heading into 2026, with net capacity additions of roughly 400,000 barrels per day against 500,000 barrels per day of light product demand growth. Crack spread data and Venezuelan crude import volumes will determine whether the 98% machine keeps running.