Dollar Tree (NASDAQ: DLTR | DLTR Price Prediction) and Dollar General (NYSE: DG) are both sitting in the discount bin right now, and retirement-focused investors may want to research which name aligns with their goals.

Valuation: Edge to Dollar Tree

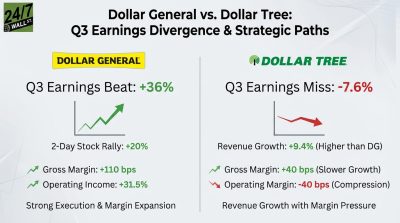

Dollar Tree just reported Q4 FY2025 EPS of $2.56, capping a full year in which adjusted diluted EPS came in at $5.75. Management guided FY2026 adjusted EPS to $6.50 to $6.90, putting the midpoint at $6.70. At a current price of $107.46, that implies a forward P/E of roughly 16x. Dollar General’s forward P/E sits at 18x, based on FY2026 guided EPS of $7.10 to $7.35. Dollar Tree’s lower multiple, combined with stronger near-term earnings momentum, gives it the valuation edge. Analyst consensus targets Dollar Tree at $126.30 versus Dollar General at $148.86, reflecting meaningful upside from current levels for both.

Yield and Income: Dollar General Wins Clearly

For retirement portfolios that depend on income, this dimension is not close. Dollar General pays $0.59 per quarter, or $2.36 annualized, with the next ex-dividend date on April 7, 2026. At current prices, that works out to a yield of approximately 1.74%. Dollar Tree pays no dividend at all. Instead, it returned $1.548 billion through share repurchases in FY2025, with $1.8 billion remaining under its buyback authorization. Buybacks benefit long-term shareholders through earnings-per-share accretion, but they do not put cash in a retiree’s account each quarter. Dollar General wins this dimension outright.

Growth Trajectory: Dollar Tree Has the Momentum

Dollar Tree’s transformation into a pure-play retailer following the Family Dollar divestiture completed July 7, 2025, is producing measurable results. Full-year FY2025 revenue grew 10.43% to $19.41 billion, and net income surged 140.44%. The Dollar Tree 3.0 multi-price format now spans approximately 5,300 converted stores, and the chain has attracted 3 million new households, with 60% coming from the $100,000-plus income bracket, a meaningful trade-down signal given that University of Michigan consumer sentiment averaged just 55.5 over the past 12 months, well below the 80 neutral threshold. Dollar General’s recovery is real but slower. FY2024 net income fell 32.27%, and while three consecutive EPS beats through Q3 FY2025 signal a genuine turnaround, comp sales growth of 2.5% in Q3 trails Dollar Tree’s 5.0% in Q4. Dollar Tree has the stronger near-term growth story.

The Verdict

Both stocks have pulled back sharply. Dollar Tree is down 14.75% over the past month and 12.64% year to date. Dollar General has dropped 14.30% over the same one-month window while holding roughly flat year to date, down just 0.3%. That divergence matters. Dollar Tree’s sharper dip came immediately after a strong earnings report. Institutional buyers including AllianceBernstein, EdgePoint, Schroder, and Korea Investment have been accumulating Dollar Tree shares, a signal worth noting.

Investors focused on income may find Dollar General worth researching further given its consistent dividend and its beta of 0.22, which makes it one of the least volatile large-cap retailers in the market. Its turnaround is progressing, and its dividend remains consistent.

Those researching growth-oriented discount retailers may find Dollar Tree’s earnings inflection and format transformation worth examining. The format transformation is gaining traction with higher-income shoppers, and the stock is trading below its 200-day moving average of $110.32 for the first time in months.