Plug Power (NASDAQ:PLUG) shares are up 5% in today’s session, trading around $2.26 as of midday Monday. The move extends a broader recovery that has the stock up 36% over the past year.

The catalyst is a combination of genuine operational milestones, a fresh leadership voice, and continued momentum from the company’s strongest earnings print in recent memory. The bulls are cheering while the courts are still watching, and that tension is exactly what defines PLUG right now.

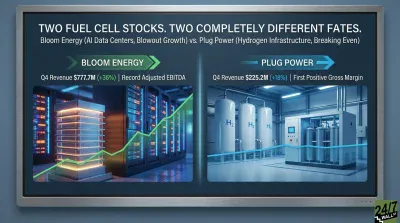

First Positive Gross Profit Drives the Bull Case

The story starts with a number that seemed impossible not long ago. Plug Power reported Q4 2025 gross profit of $5.5 million on $225.2 million in revenue, marking the first positive gross margin in recent memory at 2.4%. For context, the company’s gross margin in Q4 2024 was -122.5%. That’s not a typo: Plug Power was spending more than twice its revenue just to deliver its product.

The Q4 beat extended across the board. Plug Power’s revenue came in 3.63% above the consensus estimate of $217.3 million, and adjusted EPS of -$0.06 beat the consensus of -$0.11 by nearly 43%.

Furthermore, Plug Power’s full-year 2025 revenue reached $709.92 million, up 12.9% year over year, a record for the company. Annual cash burn was cut by 26.5%, and Plug Power ended the year with $368.5 million in unrestricted cash.

The margin improvement came from three places: volume leverage, pricing increases, and manufacturing efficiency gains under Project Quantum Leap. These are structural improvements, not one-time accounting items, though Jefferies pushed back on that point (more on that below).

New CEO, New Tone

New Plug Power CEO Jose Luis Crespo, who took the helm on March 2, wasted no time setting expectations.

“In 2025, we achieved $710 million in revenues and Q4 margin positive as we projected at the start of the year. In 2026, we will continue executing with discipline, driving margin improvement, and delivering exceptional outcomes for our customers. By leveraging our strong commercial foundation, advancing cost-efficiency initiatives, and capitalizing on our more than $8 billion global sales funnel, we are converting operational momentum into sustainable financial performance. Our targets remain consistent in achieving positive EBITDAS in Q4 of 2026, positive operating income by the end of 2027, and full profitability by the end of 2028, while still growing the Company substantially.”

That roadmap gives Plug Power’s investors specific milestones to track rather than vague turnaround promises. The company is also participating in investor conferences across London, Stockholm, Paris, and Washington, D.C. this month, keeping the narrative active.

Asset Sales and Strategic Pivots Add Fuel

Beyond the earnings beat, Plug Power has been executing on its balance sheet. The company sold its New York Project Gateway site to Stream Data Centers for $132.5 million, the first phase of a $275 million strategic infrastructure optimization program expected to close in H1 2026.

Perhaps the most forward-looking development is Plug Power’s plan to offer up to 250 MW of hydrogen electricity in a potential PJM Interconnection power grid auction. PJM is the largest power grid in the U.S., and positioning hydrogen as a dispatchable power source for AI-driven data center demand is exactly the kind of narrative shift that attracts new investor attention.

For a deeper look at how Plug Power stacks up against its closest fuel cell rival, this comparison of Bloom Energy and Plug Power from earlier this month lays out the diverging paths clearly.

The Courts Are Still Watching

The legal overhang is real and cannot be dismissed. Multiple securities class action lawsuits have been filed by firms including Pomerantz, the Rosen Law Firm, and Bronstein Gewirtz and Grossman, alleging that Plug Power made false and misleading statements about the likelihood of receiving a $1.66 billion U.S. Department of Energy loan guarantee and its ability to construct hydrogen production facilities.

Additionally, Plug Power carries an accumulated deficit of $8.2 billion and recorded approximately $763 million in Q4 non-cash asset impairment charges. Operating cash flow for the full year was negative $535.84 million. The path to profitability runs through the end of 2028 — a long runway with a lot of execution risk.

Analysts Split on Whether the Margin Gains Are Real

The analyst community is not rushing to upgrade Plug Power shares. The consensus sits at Hold across 17 analysts, with 5 sell ratings, 8 holds, and 4 buy or strong buy ratings. The average PLUG stock price target is $2.89, implying modest upside from current levels.

Wells Fargo raised its price target to $2 from $1.50 following the Q4 results, acknowledging the beat and the margin milestone. Jefferies, on the other hand, cut its target to $1.80 from $2, calling the margin improvement a “show me” story and flagging that some Q4 gross margin benefit came from one-off items. TD Cowen downgraded Plug Power shares from Buy to Hold and cut its target to $2 from $4, citing execution challenges and a slower electrolyzer ramp-up.

Insiders, for what it is worth, are net buyers. Nine recent insider transactions have skewed toward buying, which at least suggests those closest to the business believe in Plug Power’s growth prospects.

What to Look for Now

Today’s move reflects a market that wants to believe the inflection point is real. The first positive gross profit in recent memory, a new CEO with a concrete timeline, $275 million in incoming asset sale proceeds, and a PJM power grid opportunity all give the Plug Power stock bulls something tangible to hold on to.

Still, the lawsuits, the $8.2 billion accumulated deficit, and the skeptical analyst community remind everyone that belief in Plug Power still needs to be earned quarter by quarter. For the time being, investors should monitor the legal proceedings as well as the $2 level for PLUG stock.