Plug Power (NASDAQ:PLUG) stock is up 6% in Thursday morning trading, with shares climbing toward $2.40 from an opening price of $2.25. The move comes on the last trading session before Good Friday, when the U.S. stock market closes for the long weekend.

The rally builds on a month that had already seen PLUG shares gain 24.31%, and the stock is now up 20% year-to-date. That momentum is drawing fresh attention to whether Plug Power’s long-awaited operational turnaround is finally gaining traction.

The renewed investor interest stems from a positive gross margin turn, an asset monetization plan, and falling Treasury yields. Still, the bear case remains formidable, and anyone considering a position should weigh both sides carefully.

Reason 1: Gross Margin Turned Positive and Revenue Is Growing

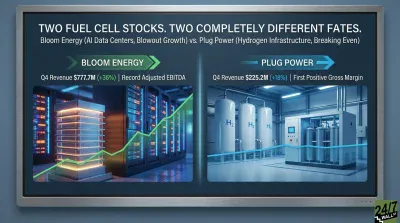

Plug Power reported Q4 FY2025 revenue of $225.22 million, a 17.63% increase year-over-year, beating the $217.3 million consensus estimate by 3.63%. More importantly, the company achieved a positive gross margin of 2.4% for the quarter, the first positive gross margin in recent memory after posting -122.5% in Q4 2024.

New CEO Jose Luis Crespo has laid out a structured profitability road map for Plug Power: positive EBITDAS by Q4 2026, positive operating income by end of 2027, and full profitability by end of 2028. The gains were driven by volume leverage, pricing increases, and manufacturing efficiency improvements under Project Quantum Leap.

The PLUG stock bulls have heard ambitious timelines before, but a positive gross margin is concrete evidence that the unit economics are shifting. That’s a meaningful difference from prior quarters in which Plug Power was losing money on every unit it sold.

Reason 2: Asset Monetization and Data Center Opportunity

Plug Power is executing a capital-release plan targeting over $275 million through asset sales, restricted cash release, and expense trimming, with those transactions targeted to close in the first half of 2026. This directly addresses the chronic cash burn that has been PLUG stock’s most persistent headwind.

The company is also positioning its hydrogen-fueled electricity assets to serve AI data centers through the PJM Interconnection grid. Plug Power CFO Paul Middleton presented this strategy at the Roth Annual Growth Conference in March, and the institutional reception was positive enough to drive PLUG shares up 3.6% that day. Indeed, placing hydrogen infrastructure at the intersection of green energy and AI demand is a compelling repositioning story.

Plug Power CEO Crespo expressed confidence in the company’s Q4 FY2025 earnings release:

“By leveraging our strong commercial foundation, advancing cost-efficiency initiatives, and capitalizing on our more than $8 billion global sales funnel, we are converting operational momentum into sustainable financial performance.”

The $8 billion funnel includes electrolyzer projects across Europe, Australia, and North America.

Reason 3: Falling Yields and Sector Momentum

Notably, Plug Power caught a macro-driven tailwind on Tuesday when shares rose 5.61% to $2.26 as falling U.S. Treasury yields boosted risk appetite for long-duration growth stocks. Lower yields reduce the discount rate on future cash flows, making speculative growth names more attractive on a relative basis.

Additionally, the hydrogen sector broadly is seeing renewed investor interest driven by global energy demand. A March 27 sector analysis noted that hydrogen stocks are poised for attention as energy demand overwhelms legacy infrastructure, with Plug Power’s positive gross margin cited as an operational improvement signal. Plug Power’s one-year gain of 71.76% reflects how much sentiment has shifted from the stock’s lows.

PLUG Stock: Acknowledging the Bear Case

All of that being said, risks remain for PLUG stock. Multiple securities fraud class action lawsuits allege that Plug Power misled investors about the likelihood of receiving a $1.66 billion DOE loan guarantee and its capacity to build hydrogen production facilities. The lead plaintiff deadline is tomorrow, April 3.

Over five years, PLUG shares have declined 93%, one of the steepest long-term drawdowns among clean energy names. The analyst consensus remains “Hold” with a target price of $2.74, and the path to profitability demands strong execution across multiple years. Moreover, Plug Power carries an accumulated deficit of $8.2 billion and full-year 2025 operating cash flow of -$535.84 million.

If you’re watching Plug Power now, the company’s gross margin turn is the most credible data point the bulls have had in years. Going forward, watch for whether the $275 million asset monetization transactions close on schedule in H1 2026. That’s the next concrete test of whether Plug Power’s comeback story has real legs or is simply riding a yield-driven wave.