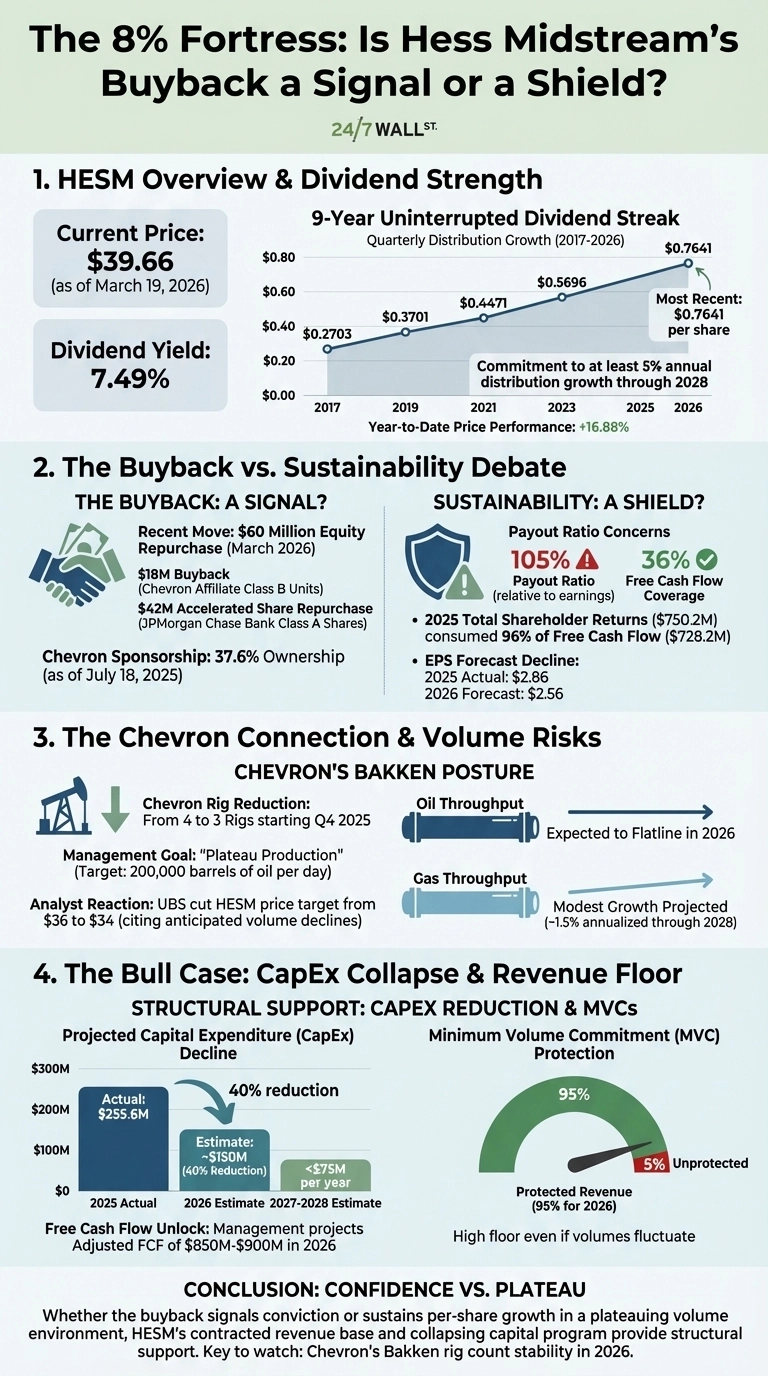

Hess Midstream LP (NYSE:HESM | HESM Price Prediction), the fee-based, growth-oriented midstream energy company, announced a $60 million equity repurchase on March 3, 2026, the latest move in a capital return program that has returned hundreds of millions to shareholders annually. The question is whether these buybacks reflect genuine confidence or are engineered to prop up per-share metrics as upstream growth stalls.

The Yield That Demands Scrutiny

HESM currently trades near $39.66 and carries a 7.49% dividend yield, backed by nine consecutive years of uninterrupted quarterly distributions. The most recent quarterly payout was $0.7641 per Class A share, up from $0.2703 at inception in August 2017. Management has committed to at least 5% annual distribution growth through 2028.

The dividend payout ratio relative to earnings sits at a concerning 105%, and analysts have flagged a 2026 EPS forecast of $2.56, a step down from the $2.86 earned in 2025. Free cash flow coverage tells a more reassuring story at 36%, though that metric tightened in 2025 when total shareholder returns of $750.2 million consumed 96% of the $728.2 million in free cash flow generated.

The Buyback Mechanics

The March repurchase included an $18 million buyback of 455,811 Class B units from a Chevron affiliate and a $42 million accelerated share repurchase with JPMorgan Chase Bank. Chevron became HESM’s sponsor on July 18, 2025, and its ownership now sits at 37.6% following prior repurchases.

CFO Michael Chadwick was direct on the Q4 2025 earnings call: “We’re also funding incremental shareholder returns for free cash flow after distributions, rather than leverage buybacks. And so it’s just a bit more of a conservative approach that we’re following that is in line with our profile and Chevron’s target of 200,000 barrels of oil per day plateau production in the Bakken.”

That phrase, “plateau production,” is the crux of the concern. Chevron reduced its Bakken rig count from 4 to 3 rigs starting Q4 2025, and UBS responded by cutting its HESM price target from $36 to $34, citing anticipated volume declines. Oil throughput is expected to flatline in 2026.

The Bull Case: CapEx Collapse and MVC Protection

CEO Jonathan Stein framed the lower-growth environment as a free cash flow unlock: “In 2026, we expect to spend approximately $150 million, a 40% reduction in capital spending relative to 2025. We expect our capital spend to decrease even further in 2027 and 2028 to less than $75 million per year.”

With approximately 95% of 2026 revenues protected by minimum volume commitments, the floor is high even if Chevron pulls back further. Management projects adjusted free cash flow of $850 to $900 million in 2026.

Whether the buyback signals conviction or sustains per-share growth in a plateauing volume environment, HESM’s contracted revenue base and collapsing capital program provide more structural support than a simple yield-chasing story. Investors will want to track whether Chevron’s Bakken rig count holds or slips further in 2026, with the stock up 16.88% year-to-date.