Centuri Holdings (NYSE:CTRI), a Phoenix-based publicly traded utility infrastructure services company, opened 2026 with a statement: more than $870 million in new commercial awards spanning MSA renewals with East Coast utilities, a new gas distribution MSA in the Southwest, and a natural gas storage and compression facility.

The announcement crystallizes the central tension surrounding this infrastructure services company: its backlog is surging, its debt is falling, and its stock has already priced in a lot of good news.

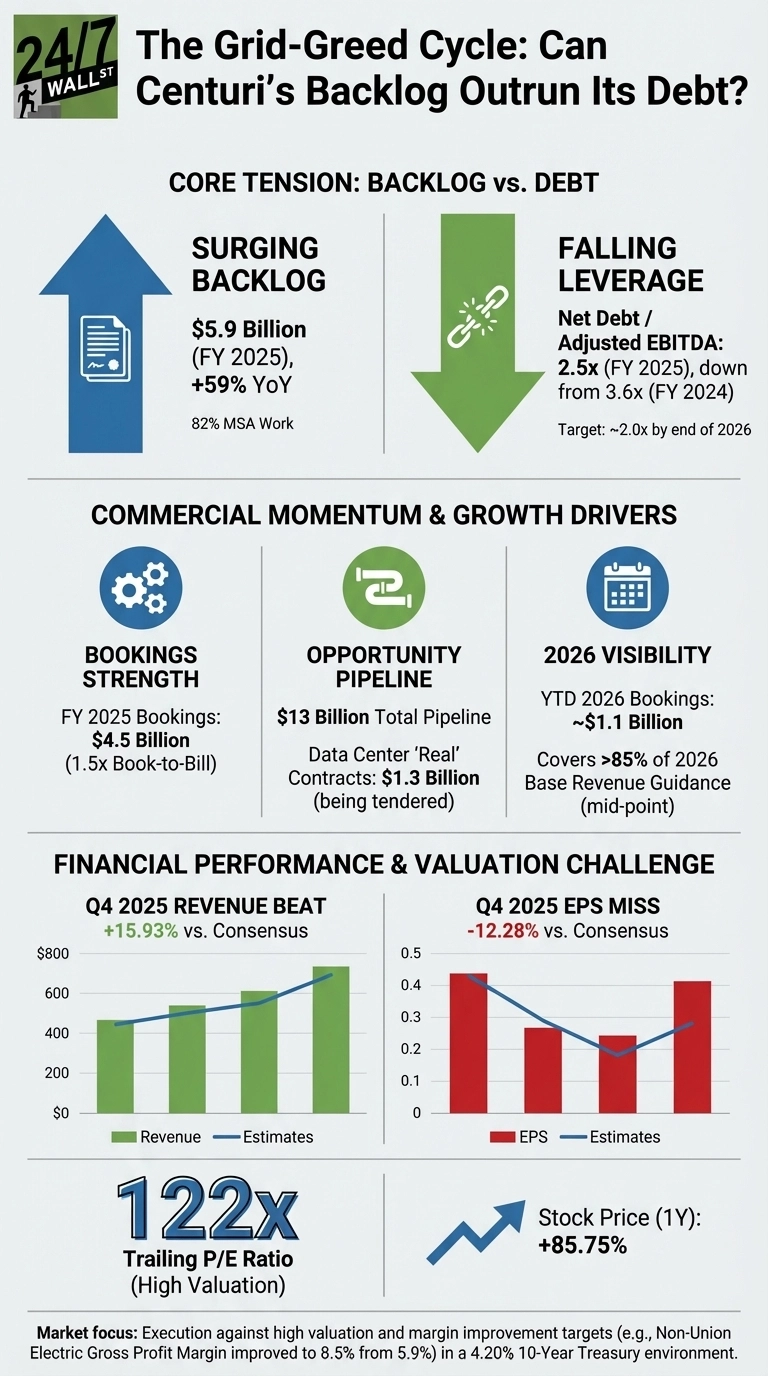

A Backlog Built for Growth

Centuri ended 2025 with a $5.9 billion backlog, up 59% from the prior year, 82% of which was MSA work. For 2026, the company already has approximately $1.1 billion in year-to-date bookings, covering over 85% of the midpoint of its 2026 base revenue guidance. CEO Christian Brown was nothing but direct on the earnings call: “Coming into 2025, we set a goal to achieve a 1.1x book-to-bill ratio. We did not just exceed our goal; we shifted it, delivering a 1.5x book-to-bill for the year. In total, our bookings surpassed $4.5 billion.”

The $13 billion opportunity pipeline includes a data center segment that Brown described with notable specificity: “Of the $2.0 billion, $1.3 billion is real today, where we have got comfort that the client has funding, all the permits are in place, and it is a real contract. We are tendering that $1.3 billion as we speak.”

The Debt Picture Is Improving, But Demands Respect

The leverage story shifted meaningfully in the second half of 2025, and, after a net debt-to-adjusted EBITDA of 3.8x in Q3 2025, the company executed a November 2025 equity offering that raised approximately $251 million in net proceeds, using the bulk of the proceeds to pay down debt.

Centuri CFO Greg Izenstark confirmed the result: “We ended the year with a net debt to adjusted EBITDA ratio of 2.5x, down from 3.6x at year-end 2024. In 2026, we plan to further delever and forecast net debt to adjusted EBITDA of around 2.0x by year-end.”

A Term Loan B repricing in March 2026 secured a 25 basis point rate reduction, and the CFO expects 2026 interest expense to run about 30% lower than 2025. With the 10-year Treasury at 4.20%, the rate environment remains a watchful backdrop for a company still carrying meaningful leverage.

Revenue Beats, Earnings Misses: The Margin Problem

Centuri’s 2025 story was consistent: revenue beat estimates every quarter while adjusted EPS missed every quarter. In Q4, revenue of $858.60 million beat the consensus by 15.93%, yet adjusted EPS of $0.17 missed the ~$0.20 estimate.

Full-year adjusted net income came in at $39 million, a 49% year-over-year increase, but the trailing P/E sits at 122, with a forward P/E of roughly 35x based on 2026 guidance, a multiple that would require a significant earnings ramp to materialize.

Management outlined four margin levers: addressing Q1 gas-seasonality, improving fleet efficiency by at least 20%, driving crew productivity in the fast-growing Non-Union Electric segment, and expanding bid-work margins. Non-Union Electric base gross profit margin already improved to 8.5% from 5.9% in 2024, suggesting the operational work is real, if still early.

A Stock That Has Run Hard

As of March 19, 2026, shares are up 80% over the past year and 20.24% year-to-date, trading near the 52-week high of $32.38. The analyst consensus target of $31.32 implies limited upside from current levels, with ratings split between 4 buys and 2 strong sells. The backlog is real, the deleveraging is real, and end-market tailwinds from grid modernization and data center power demand are real. Whether the current valuation leaves enough margin for inevitable execution bumps is the question the market is still working through.