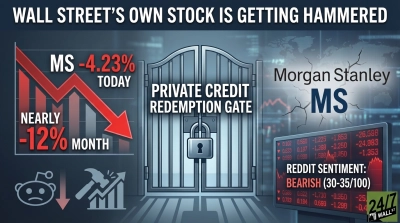

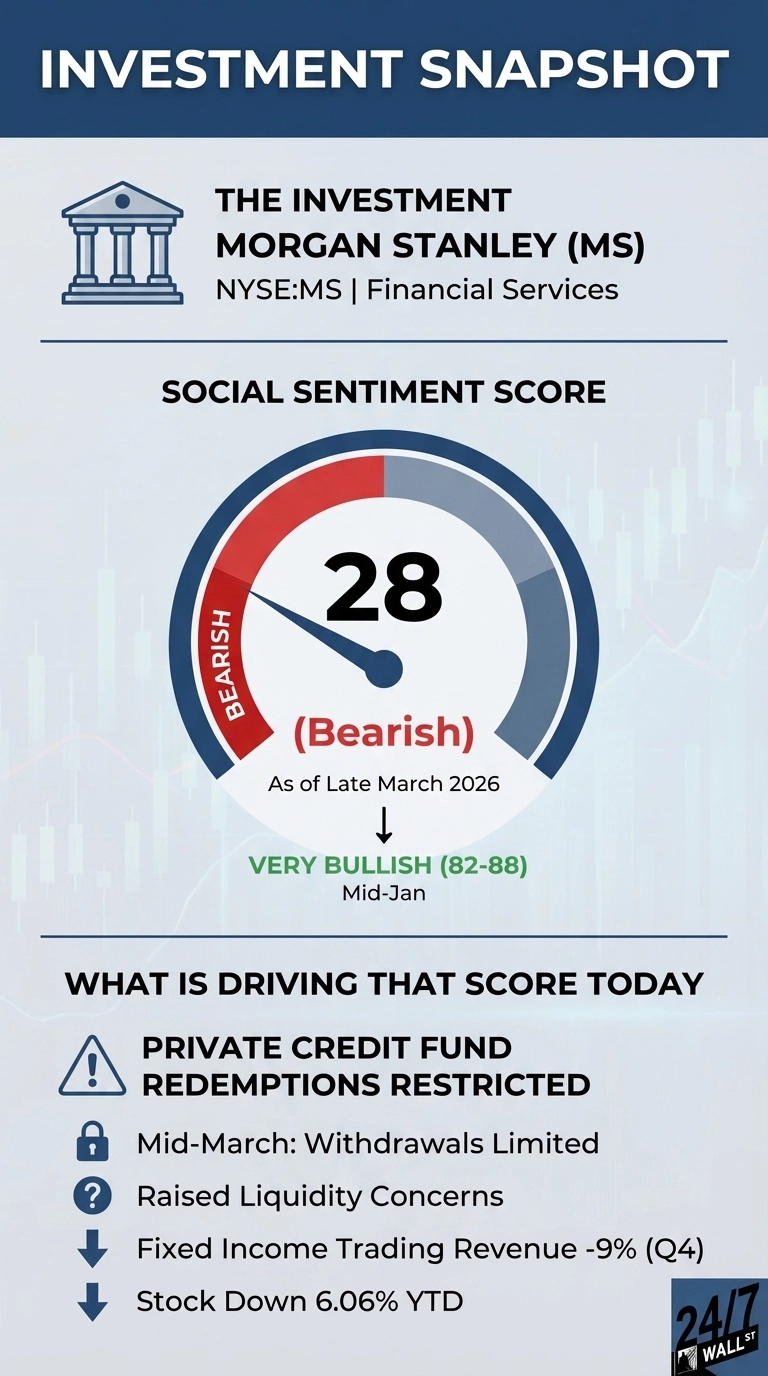

One of the biggest names in financial services and investment banking, Morgan Stanley (NYSE:MS | MS Price Prediction) posted a record $70.6 billion in 2025 revenue and an 11.2% Q4 earnings beat, yet Reddit sentiment has collapsed from very bullish scores of 82 to 88 in mid-January to a bearish 28 by late March. The trigger was not the earnings report. It was what happened two months later.

In mid-March, Morgan Stanley restricted redemptions in its North Haven Private Income Fund after investors sought to withdraw nearly 11% (10.9%, to be exact) of the shares outstanding. The firm fulfilled only about 45.8% of the tender request, returning roughly $169 million, citing the need to avoid asset sales during “periods of market dislocation.” That news landed on Reddit like a flare in a dark room as one would expect on the platform.

Morgan Stanley’s Private Credit Problem Spooks Retail Investors

The two posts driving the most discussion appeared on March 12 to 13, 2026, generating a combined 810 upvotes and 175 comments across r/stockmarket and r/stocks.

Morgan Stanley restricts redemptions at private credit fund after withdrawals surge

by u/unknown in r/stockmarket

The r/stockmarket thread framed the redemption gate as a structural warning for the private credit industry, with one commenter writing: “This is exactly the kind of liquidity mismatch that blows up in a downturn — private credit funds promising semi-liquid access but gating when it matters most.” The second post, titled “When you see one cockroach, there are probably more,” drew on JPMorgan CEO Jamie Dimon’s October warning about credit market risks and applied it directly to Morgan Stanley’s situation.

When you see one cockroach, there are probably more

by u/unknown in r/stocks

Skepticism across r/stockmarket, r/stocks, and r/investing centers on three specific concerns:

- Morgan Stanley restricted redemptions at its North Haven Private Income Fund to 5% of units, honoring less than half of investor requests and raising structural liquidity questions across its $1.9 trillion Investment Management business.

- Fixed Income net revenues fell 9% year-over-year in Q4, and the recent “gating” of private credit capital compounds fears of deteriorating credit quality within the firm’s institutional book.

- Shares have plunged roughly 10% year-to-date, falling from a January high of $192.68 to approximately $165, effectively erasing the optimism from its record $70.6 billion 2025 revenue report.

Record Revenue, But the Stock Tells a Different Story

The underlying 2025 results were strong. Investment banking revenue surged 47% YoY, Wealth Management brought in $122.3 billion in net new assets in Q4 alone, and CEO Ted Pick called it “outstanding performance.” Analysts still see roughly 17% upside to their average price target of $193.22, with EPS expected at $2.92, up 12% from Q1 2025.

Peer Goldman Sachs (NYSE:GS) faces the same year-to-date pressure, down 4.43% versus Morgan Stanley’s 6.06%, pointing to broader sector headwinds. The private credit gate remains the story investors will watch most closely heading into Q1 earnings.