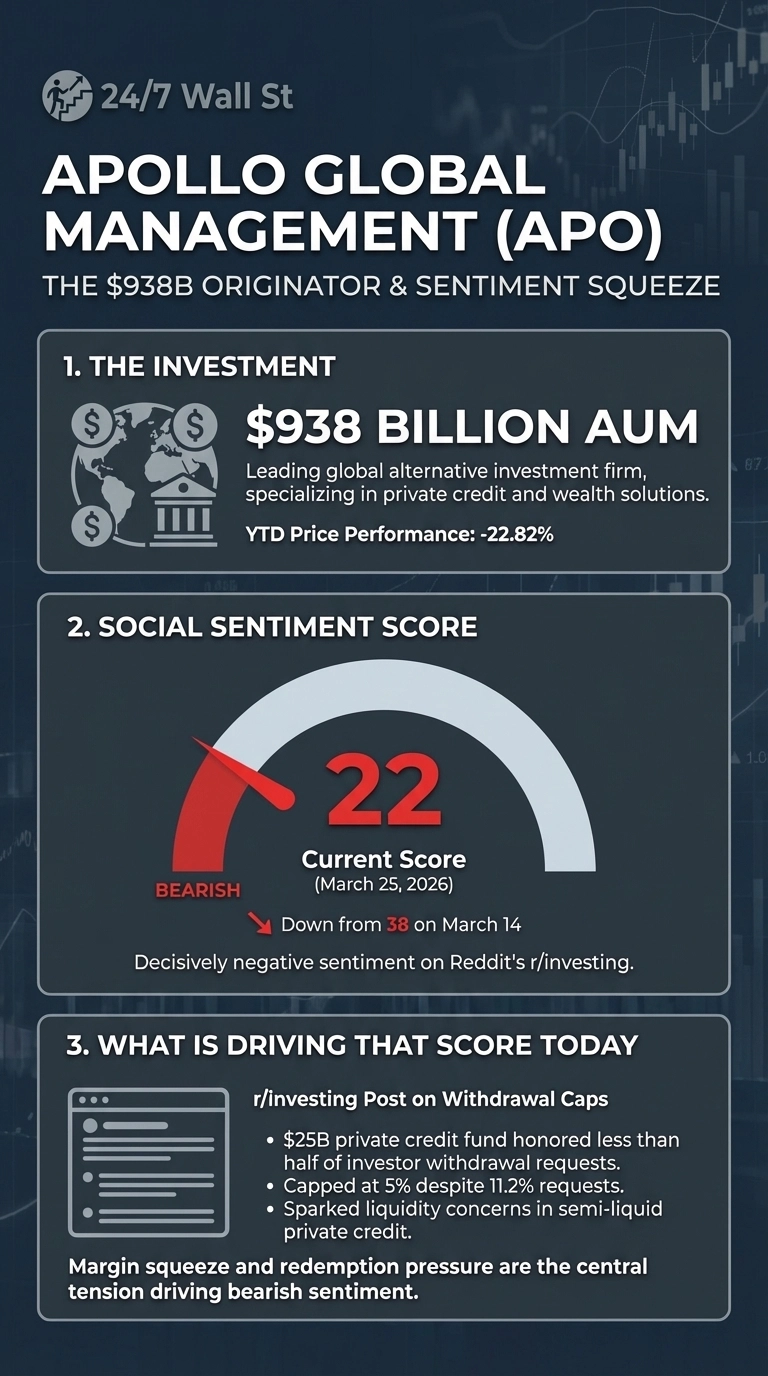

Apollo Global Management (NYSE:APO | APO Price Prediction) is sitting on $938 billion in assets under management after a record year, yet shares have fallen 22.06% year to date, and Reddit’s r/investing community has turned decisively negative. The sentiment score has dropped from 38 on March 14 to 22 by March 25, indicating a firm bearish tone, driven by one alarming story: Apollo’s private credit fund honored fewer than half of investor withdrawal requests.

The trigger was a post by r/investing user DustInside6861, which accumulated 710 upvotes and 128 comments within days. The post described how Apollo’s $25 billion private credit fund received withdrawal requests totaling 11.2% this quarter and honored only 5%, capped at 5%. The framing was blunt: “This is now happening simultaneously across the entire $1.8 trillion private credit industry. The structural problem is simple: these funds hold illiquid corporate loans that can’t be quickly sold, so when everyone wants out at once, the math doesn’t work.”

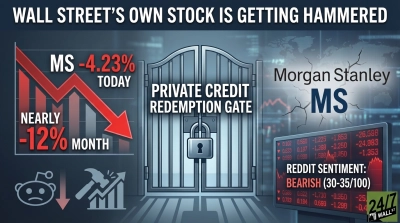

Apollo Just Gave Investors Only 45% of Requested Withdrawals. BlackRock, Morgan Stanley, and Blue Owl Are Doing the Same Thing.

by u/DustInside6861 in r/investing

Withdrawal Restrictions Hit Apollo’s Retail Strategy at the Worst Time

Apollo’s bull case has rested on bringing private credit to retail and wealth-channel investors. A second r/investing post summarizing a Wall Street Journal investigation captured the damage: “Retail capital is going to be a lot more cautious. In the short-term, there is not going to be one financial adviser allocating money to them,” according to newsletter author Leyla Kunimoto. Apollo’s Global Wealth channel had just posted a record $18 billion in annual inflows, making that warning sting harder.

Three compounding pressures define the bearish case:

- Net spread compression has reached 17 basis points year over year, pushing Apollo’s net spread to 1.20%, while the cost of funds surged 30.9% in Q4 alone, squeezing the yield engine powering Athene’s retirement business.

- With 86.7% revenue growth in Q4 2025, net income rose 11.3% to $1.54 billion year over year in the same quarter, signaling real profitability

- The withdrawal cap has exposed the structural liquidity mismatch inside semi-liquid private credit funds, with Rubric Capital’s David Rosen warning investors to exit the asset class entirely, calling Cliffwater’s fund “the canary in the coal mine.”

Strong Results With a Catch

The business delivered genuinely strong results, as full-year 2025 revenue reached $32 billion, up 22.73%, and CEO Marc Rowan declared “record origination activity exceeding $300 billion and inflows of more than $225 billion.” Q4 adjusted EPS came in at $2.47, well above the $2.04 consensus. Apollo raised its 2026 dividend by 10% to $2.25 per share and authorized a new $4 billion share repurchase program.

Wall Street analyst views remain constructive as 15 analysts rate APO a Buy or Strong Buy against just 5 Holds and zero Sells, with a consensus price target near $154. As of March 25, 2026, shares are trading around $109.92, well below the 52-week high of $157.

Private Credit’s Liquidity Stress Test Is Just Beginning

Blue Owl is down more than 41% this year, and Blackstone’s credit fund saw net withdrawals for the first time. Apollo’s scale makes it the most visible name in this industry-wide liquidity test. Whether withdrawal pressure accelerates into Q2 2026 or stabilizes will determine whether the retail wealth channel Apollo spent years building becomes an asset or a liability.