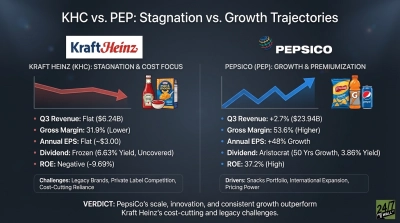

PepsiCo (NASDAQ:PEP | PEP Price Prediction) has had a turbulent March. After gaining 19.34% year-to-date through late February, shares pulled back 6.35% over the past month, settling around $156.66 and sitting well below the 52-week high of $171.48. Over one year, shares are up just 4.48%.

Most analysts have settled into a cautious posture, with the Street consensus sitting at a “Hold” rating across 20 analysts. Deutsche Bank analyst Steve Powers is holding firm with a Buy rating and a bold $169 price target, representing roughly 10% upside from current levels. That target sits just below the Street consensus of $171.38, with Powers cutting it from $176 after flagging mounting macro headwinds. Can PEP realistically reach $169 by the end of 2026?

Steve Powers’s $169 PEP Prediction

Powers sees “legitimate and widespread pressures building” across consumer packaged goods, driven by Middle East conflict creating cost inflation, potential demand destruction from consumer trade-down, and adverse currency moves. Yet he maintains his Buy, pointing to PepsiCo’s Q4 momentum: core EPS grew 11% in constant currency and EMEA operating profit surged 72%, demonstrating the portfolio’s ability to generate earnings power even through turbulence. Management’s commitment to a record year of productivity savings in fiscal 2026 adds further support to the thesis.

Key Drivers of PEP Stock Performance

- Dividend compounding: PepsiCo just raised its annualized dividend to $5.92 per share, marking its 54th consecutive annual dividend increase. For retirement accounts, that consistency is a compounding engine. Total shareholder returns for 2026 are projected at ~$8.9 billion.

- International growth offsetting North American pressure: With LatAm Foods up 11% and EMEA up 12% in Q4, global diversification is actively cushioning domestic weakness. CEO Ramon Laguarta noted “the situation in the Middle East looks good, with consumers there performing well.”

- Productivity and brand reinvestment: Major relaunches across Lay’s, Gatorade, and Quaker, combined with double-digit shelf space gains expected from spring resets, position PepsiCo to rebuild North American volume. CFO Steve Schmitt confirmed productivity gains will “fund some of our investments” in growth.

What Will It Take for PEP to Reach $169?

With 1.37 billion shares outstanding and a current market cap of approximately $209.3 billion, reaching $169 would push PepsiCo’s market cap toward roughly $231 billion. The conditions required: organic revenue growth at the high end of the guided 2-4% range, core constant currency EPS growth of 4-6%, and stabilization of North American volumes as affordability investments gain traction.

The primary risk is that consumer trade-down accelerates further, with University of Michigan sentiment still at a pessimistic 56.6 and tariff-driven commodity costs delivering an 11-percentage-point headwind in PBNA last quarter. Still, for retirement investors, PepsiCo’s 54-year dividend growth streak, $8.9 billion in projected shareholder returns, and Deutsche Bank’s maintained Buy conviction make $169 a credible destination for patient, long-term holders.