Europe’s defense spending surge has turned a quiet corner of the ETF market into one of the most-watched trades of the past 18 months. The Select STOXX Europe Aerospace & Defense ETF (NYSEARCA:EUAD) gives U.S. investors a single-ticket way to own the continent’s leading defense and aerospace companies as NATO allies race to rebuild military capacity. But the fund’s dividend yield of roughly 0.36% raises an immediate question: is this a dividend investment at all?

How EUAD Generates Income

EUAD is a plain-vanilla equity ETF. It holds shares of European aerospace and defense companies, collects whatever dividends those companies pay, and passes the cash through to shareholders after covering its 0.50% annual expense ratio. No options strategies, no leverage, no synthetic structures. Income depends entirely on what the underlying companies choose to distribute.

The fund launched in October 2024 and tracks the STOXX Europe Total Market Aerospace & Defense Index. Its net assets stand near $1.5 billion, reflecting the surge of investor interest in European rearmament. With portfolio turnover of just 16%, the holdings are relatively stable.

Who Is Driving the Yield

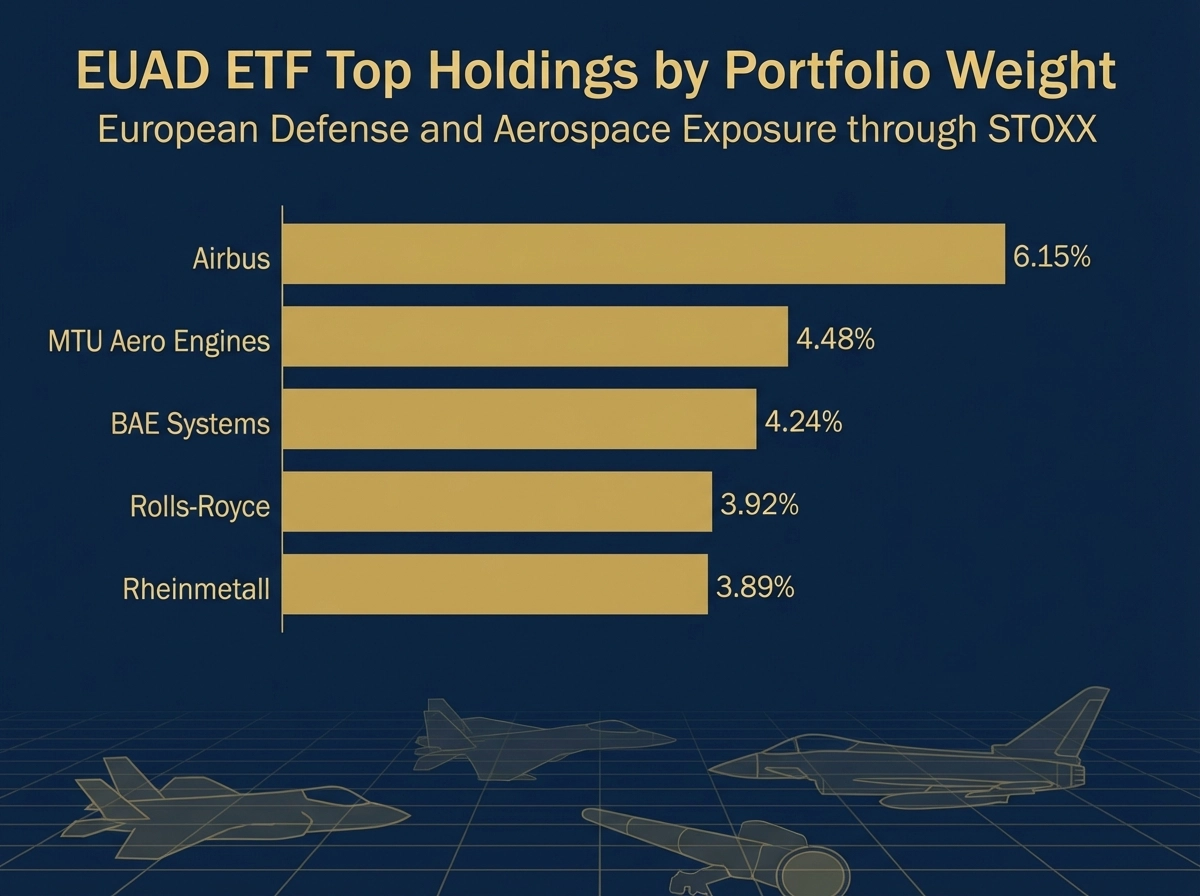

The top five positions account for roughly 22% of the portfolio, and their dividend policies shape the fund’s income profile almost entirely.

- Airbus (EADSY), 6.15% weight: The fund’s largest position. Airbus pays dividends but is primarily a growth and capital-allocation story. Its yield is modest and the payout has been inconsistent amid aircraft production ramp-ups and supply chain pressure. Airbus ADR shares have fallen nearly 22% year-to-date, weighing on EUAD’s NAV even as the defense narrative remains intact.

- MTU Aero Engines (MTUAY), 4.48% weight: A German engine maintenance and manufacturing specialist. MTU’s dividend is modest and tied closely to civil aviation demand, introducing cyclical risk absent from pure defense contractors.

- BAE Systems (OTC:BAESY), 4.24% weight: The most consistent dividend payer in the top five. BAE has paid semi-annual dividends without interruption since at least 2009. The upcoming spring 2026 payment carries an ex-dividend date in late April 2026, with a per-ADR amount of about $1.22. The trailing payout ratio sits near 34%, well within a safe range. BAE’s revenue is anchored in long-term government defense contracts in the U.K., U.S., and Australia, insulating its cash flow from economic cycles. BAESY shares have risen 21% year-to-date, making it the standout performer among top holdings.

- Rolls-Royce (RYCEY), 3.92% weight: Rolls-Royce reinstated its dividend only recently after suspending it during the pandemic. The recovery has been strong, but its dividend history carries a credibility gap that more established payers do not.

- Rheinmetall (RNMBY), 3.89% weight: The purest defense play in the portfolio. Rheinmetall reported 2025 revenue of roughly 9.9 billion euros, up 29% year-over-year and guided for sales growth of up to 45% in 2026. The backlog is enormous, but RNMBY shares pulled back nearly 18% over the past month as investors took profits after a multi-year run that saw the stock rise more than 1,600% over five years.

A Yield Too Low to Live On

At roughly 0.4%, EUAD’s yield is not a meaningful income source. European defense companies are reinvesting heavily into production capacity, R&D, and contract fulfillment rather than returning cash to shareholders. The fund functions more like a growth ETF than a dividend vehicle.

BAE Systems is the exception. Its semi-annual dividend has never been suspended, even through the 2008 financial crisis. The combined ADR payout for the most recent spring and fall cycle totaled roughly $1.77, up from around $1.11 in the equivalent 2021 cycle. That consistency matters, but BAE represents only about 4% of EUAD’s portfolio.

Total Return Is the Real Story

Since inception in late 2024, EUAD has gained roughly 55% from its starting price near $25. The past month has been rough: shares dropped nearly 17% over the past month, and the fund is down about 8% year-to-date. The fund trades near $41.

The divergence between EUAD and BAE Systems illustrates the portfolio’s internal tension. BAE is up more than 21% year-to-date while Airbus, the largest weight, has lost more than a fifth of its value. The pure defense names are performing; the aerospace-commercial names are dragging.

A Growth Trade with a Nominal Yield

EUAD’s dividend is safe in the narrow sense. The underlying companies hold expanding government backlogs, and none of the major holdings appear at risk of cutting payouts. BAE Systems has one of the most dependable dividend records in global defense, with uninterrupted payments stretching back to at least 2009.

The real risk is price volatility, not a dividend cut. A 17% monthly drawdown in a fund yielding under 0.5% erases years of dividend payments in weeks. EUAD suits investors who want direct exposure to European rearmament and understand they are buying a growth story with a nominal yield attached. Income-focused investors expecting meaningful cash distributions will find 0.4% falls well short.