Microsoft (NASDAQ:MSFT | MSFT Price Prediction) has declined 22% year-to-date from its highs, and our model prices the stock at $491.47 over the next 12 months. The price target for Microsoft is $491.47, implying 33.2% upside from the current price of $368.94. The 24/7 Wall St. model rates the stock BUY, with a confidence level of 90%.

| Metric | Value |

|---|---|

| Current Price | $368.94 |

| 24/7 Wall St. Price Target (12-Month) | $491.47 |

| Upside | 33.2% |

| Recommendation | BUY |

| Confidence Level | 90% |

A Rough Start to 2026 for Shareholders

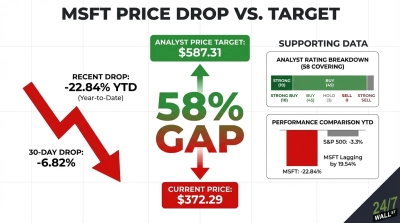

Microsoft shares are down 22% year-to-date, falling from $482.52 at the start of the year to $368.94 as of writing. The stock sits roughly 32% below its 52-week high of $552.24 and trades closer to its 52-week low of $350.25. The one-month decline stands at 9.88%, though shares posted a 1.08% gain over the most recent week.

Fundamentals remain strong. In Q2 FY2026, Microsoft delivered non-GAAP EPS of $4.14 against a consensus estimate of $3.85, a 7.57% beat. Revenue reached $81.27 billion, up 16.72% year-over-year, with Azure growing 39% and the commercial remaining performance obligation surging 110% to $625 billion.

The Case for $600 and Beyond

The bull case rests on Azure’s compounding growth and Microsoft’s AI backlog. The commercial remaining performance obligation (RPO) of $625 billion provides multi-year revenue visibility few companies can match.

OpenAI’s commitment to purchase $250 billion of incremental Azure services represents a structural demand floor. Bulls see the analyst consensus target of $587.31 as achievable, with 55 buy-or-better ratings and zero sells. Our bull case projects $601.46 over the next 12 months if Azure sustains 39-40% growth and AI monetization accelerates.

What Could Go Wrong

The bear case centers on capital discipline and competitive pressure. CapEx nearly doubled year-over-year in Q2 FY2026 to $29.8 billion, compressing free cash flow. FY2025 free cash flow declined 3.32% year-over-year to $71.61 billion.

OpenAI investment losses reached $3.1 billion in Q1 FY2026 versus $523 million a year earlier. The More Personal Computing segment contracted 3% in Q2 FY2026.

Our bear case target sits at $436.41 if macro headwinds slow enterprise cloud spending. The heavy CapEx reflects deliberate AI infrastructure investment, and the $625 billion RPO backlog suggests this spending is backed by committed customer demand.

Valuation and Forward Outlook

The 24/7 Wall St. price target of $491.47 reflects a stock oversold relative to its fundamental trajectory. Azure growth of 39%, a $625 billion backlog, and a forward P/E of 19x support the 24/7 Wall St. price target of $491.47.

Our model rates the stock BUY with 90% confidence. Key downside risks include Azure growth decelerating meaningfully below 35% next quarter or CapEx continuing to expand without corresponding backlog growth.

| Year | 24/7 Wall St. Price Target |

|---|---|

| 2026 | $491.47 |

| 2027 | $570.00 |

| 2028 | $650.00 |

| 2029 | $761.92 |

| 2030 | $818.04 |

These projections assume Microsoft continues executing on Azure AI expansion and commercial cloud adoption. Significant upside toward $1,116.92 is possible in the bull case if AI monetization accelerates beyond current projections, while a bear case implies $571.48 by the end of the five-year period.