Palantir Technologies (NASDAQ:PLTR | PLTR Price Prediction) has pulled back sharply from its highs. With shares at $128.06, our price target is $148.91, implying upside of approximately 16.28% over 12 months. Confidence level: 90%.

| Metric | Value |

|---|---|

| Current Price | $128.06 |

| 24/7 Wall St. Price Target | $148.91 |

| Upside | +16.28% |

| Recommendation | Bullish |

| Confidence Level | 90% |

The stock trades well below its 52-week high of $207.52, reflecting a significant discount from the 52-week high for investors tracking the AI platform thesis.

A Rough Start to 2026

Palantir shares are down 27.95% year-to-date, falling from $177.75 at the start of the year to $128.06. The one-week decline is -13.74%, dropping from $148.46 to $128.06 between April 2 and April 10. Despite 2026 losses, the one-year return remains positive at 44.55% from $88.59.

The most recent earnings report was exceptional. Q4 2025 revenue hit $1.40 billion, up 70% year-over-year, beating estimates by 5.74%. Adjusted EPS of $0.25 beat the $0.18 consensus, exceeding expectations by 38.89%. The stock was trading at $158.06 at the time of filing and has since declined, making the valuation more attractive.

The Bull Case

Palantir’s Rule of 40 score reached 127% in Q4 2025, unmatched in large-cap software. U.S. commercial revenue grew 137% year-over-year in Q4, with full-year 2026 guidance calling for U.S. commercial revenue exceeding $3.144 billion, representing at least 115% growth.

The AIP (Artificial Intelligence Platform) drives growth, with remaining deal value of $4.38 billion in U.S. commercial (up 145% year-over-year) providing forward visibility.

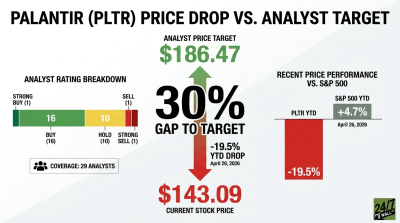

The bull scenario projects a price of $195.43 by April 2027. Wall Street consensus target of $185.25 from 17 buy-rated analysts reflects similar optimism. If 2026 guidance of $7.182 to $7.198 billion in revenue is achieved, the stock could re-rate meaningfully higher.

Downside Risks

At a trailing P/E of 203x and price-to-sales of 68x, the stock prices in flawless execution. Any guidance miss or macro spending slowdown could compress the multiple sharply. The bear scenario puts Palantir at $128.35 by April 2027, essentially flat from today.

| Year | 24/7 Wall St. Price Target |

|---|---|

| 2026 | $148.91 |

| 2027 | $147.97 |

| 2028 | $165.72 |

| 2029 | $177.94 |

| 2030 | $193.85 |

Significant upside could result from AIP adoption acceleration; meaningful downside from valuation compression or macro spending cuts.

The Verdict

Our price target of $148.91 carries 90% confidence. Fundamentals are exceptional: Rule of 40 score of 127%, free cash flow of $2.27 billion in 2025, and 2026 guidance for adjusted free cash flow of $3.92 to $4.12 billion show extraordinary compounding.

The YTD pullback of 27.95% brings the stock to its lowest level in nearly a year. Investors watching the 2026 commercial revenue ramp and macro headwinds on enterprise AI spending will find the key variables to monitor in the quarters ahead. The risk-reward at $128 is the most favorable in months.